On Wall Street, few things create chaos quite like a short squeeze. It happens when traders heavily bet against a stock, only for the shares to suddenly reverse higher. As prices climb, short sellers rush to buy back stock to limit losses, which pushes shares even higher in a self-feeding rally. Sometimes, the bigger the bearish crowd, the sharper the comeback rally can be.

Hence, investor eyes are suddenly back on Wolfspeed, (WOLF), as the silicon carbide pioneer has been through a brutal stretch. Rising manufacturing costs, mounting debt, and a Chapter 11 filing last year nearly crushed investor confidence. But after emerging from bankruptcy with a much cleaner balance sheet, WOLF stock staged a stunning comeback, surging sharply and reminding traders that the company still plays an important role in the growing EV, defense, and industrial semiconductor markets.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Now the story is getting even more interesting. Despite a recent double-digit pullback that appeared driven mostly by profit-taking, bearish traders still remain aggressively positioned against the stock. With 117.38% of the float reportedly sold short, the setup is starting to resemble a “pressure cooker.” So, if momentum turns positive again, WOLF may not plunge further at all. Instead, the stock could become the latest battleground for a giant short squeeze that sends shares sharply higher in a hurry.

Let’s get into more details.

About Wolfspeed Stock

Wolfspeed’s story traces back to its 1987 roots as Cree, a North Carolina-born innovator betting early on SiC before it was cool. As the company expanded into Europe and Asia with a sharper focus on SiC and gallium nitride (GaN) power technologies, it rebranded to Wolfspeed in 2021 – an identity shift that matched its evolution into a pure-play wide-bandgap powerhouse. Wolfspeed’s market cap stands at $3.1 billion.

Wolfspeed’s stock performance has been marked by a dramatic turnaround. Just last year, the chipmaker was fighting for survival. During the first half of 2025, bankruptcy fears crushed investor confidence, the stock price collapsed, and WOLF became one of the market’s most heavily shorted names. Many traders had almost written the company off completely.

Then came the reset. After emerging from Chapter 11 bankruptcy on Sept. 29 and replacing old shares with newly issued ones, sentiment around Wolfspeed suddenly flipped. Investors began viewing the company less as a failed EV supplier and more as a possible hidden AI infrastructure play.

That shift triggered a massive rally.

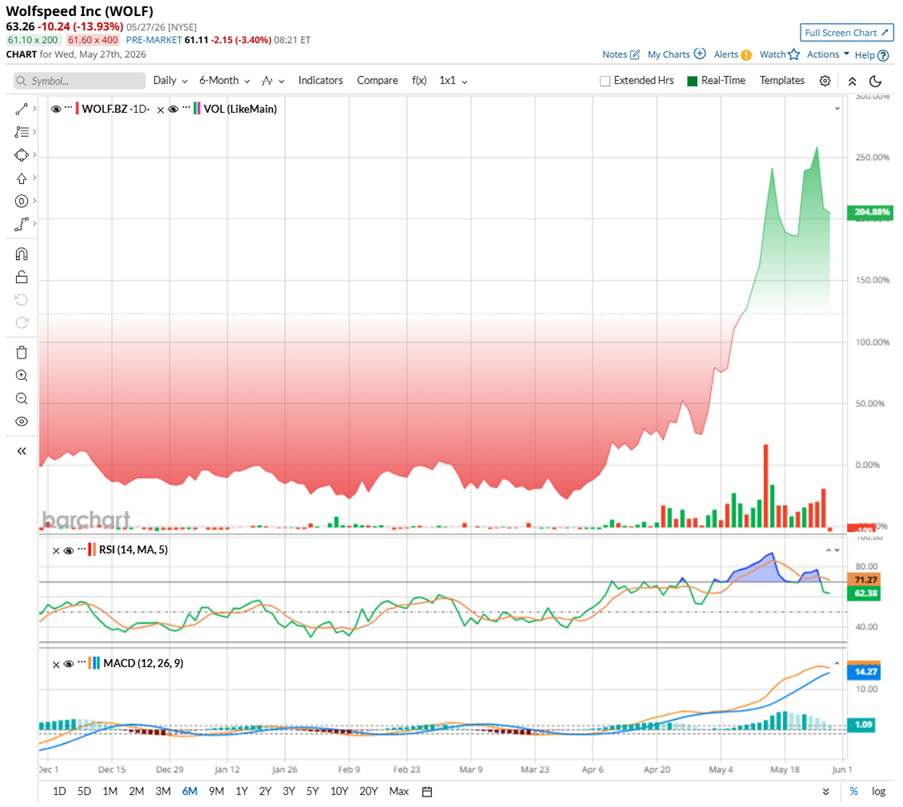

In 2026 alone, WOLF stock has skyrocketed 273.64%, eventually touching a high of $80.82 on May 22. Some of the excitement came after recent bullish commentary from Citrini Research, which described Wolfspeed as a “crouching tiger getting ready to reveal a dragon.” Ironically, the same aggressive factory expansion that once pushed the company toward bankruptcy is now being viewed as a potential advantage in the AI era. The logic is that Wolfspeed already built large silicon carbide manufacturing capacity that could eventually benefit from rising AI power and data center demand.

Still, the rally has not been smooth. After hitting its recent peak, the stock pulled back roughly 21.7% as traders locked in profits following the explosive run. Even with that decline, WOLF remains up 151.64% over the past month alone, showing just how aggressively speculative money has poured back into the stock.

Technically, momentum is starting to cool slightly. Recent trading sessions have shown more red volume bars, signaling increased selling pressure after the huge rally. The 14-day RSI has also started moving lower after previously entering overheated territory, suggesting some of the earlier buying frenzy is fading. Meanwhile, the MACD indicator still remains positive, but momentum appears less aggressive than it was during the stock’s sharp breakout phase.

www.barchart.com

www.barchart.com A Snapshot of Wolfspeed’s Q3 Report

Wolfspeed’s third-quarter fiscal 2026 results, announced on May 5 showed a company that is still going through a tough rebuilding phase rather than enjoying smooth growth. The chipmaker generated $150.2 million in revenue, landing right in the middle of its own forecast range. The numbers did not surprise investors much, but they showed the business may finally be stabilizing after a difficult stretch.

Profitability, however, remains the biggest challenge.

The company’s adjusted gross margin stayed deep in negative territory at -21%, although that was slightly better than the previous quarter. Wolfspeed explained that its factories are still not running at full capacity, which is hurting efficiency and profitability. In fact, underused manufacturing facilities alone reduced gross margin by around $46 million during the quarter. Management made it clear that improving factory utilization will be critical if the company wants margins to recover over time.

Losses also remained heavy. Wolfspeed posted a loss of -$3.26 per share, much wider than last year’s loss, though better than the previous quarter’s massive decline. And, the company burned cash during the quarter, reporting negative operating cash flow of $83.8 million and negative adjusted EBITDA of $61.7 million. That signals Wolfspeed is still spending aggressively to expand and upgrade its business.

At the same time, the company did make progress financially. It reduced some of its expensive debt, cut total borrowings by $97 million, and lowered annual interest costs by an estimated $62 million. With around $1.2 billion in available liquidity, management believes the company still has enough financial flexibility to continue funding its key projects.

Further, Wolfspeed is trying to position itself for future demand. During the quarter, it introduced new silicon carbide power products, expanded development of its advanced 300mm platform, and continued seeing growth in AI data center applications, which rose roughly 30% sequentially.

Looking ahead, the company expects Q4 revenue between $140 million and $160 million, while margins are expected to remain negative. Right now, Wolfspeed’s story is less about short-term profits and more about whether today’s heavy investments can eventually turn into a sustainable business turnaround.

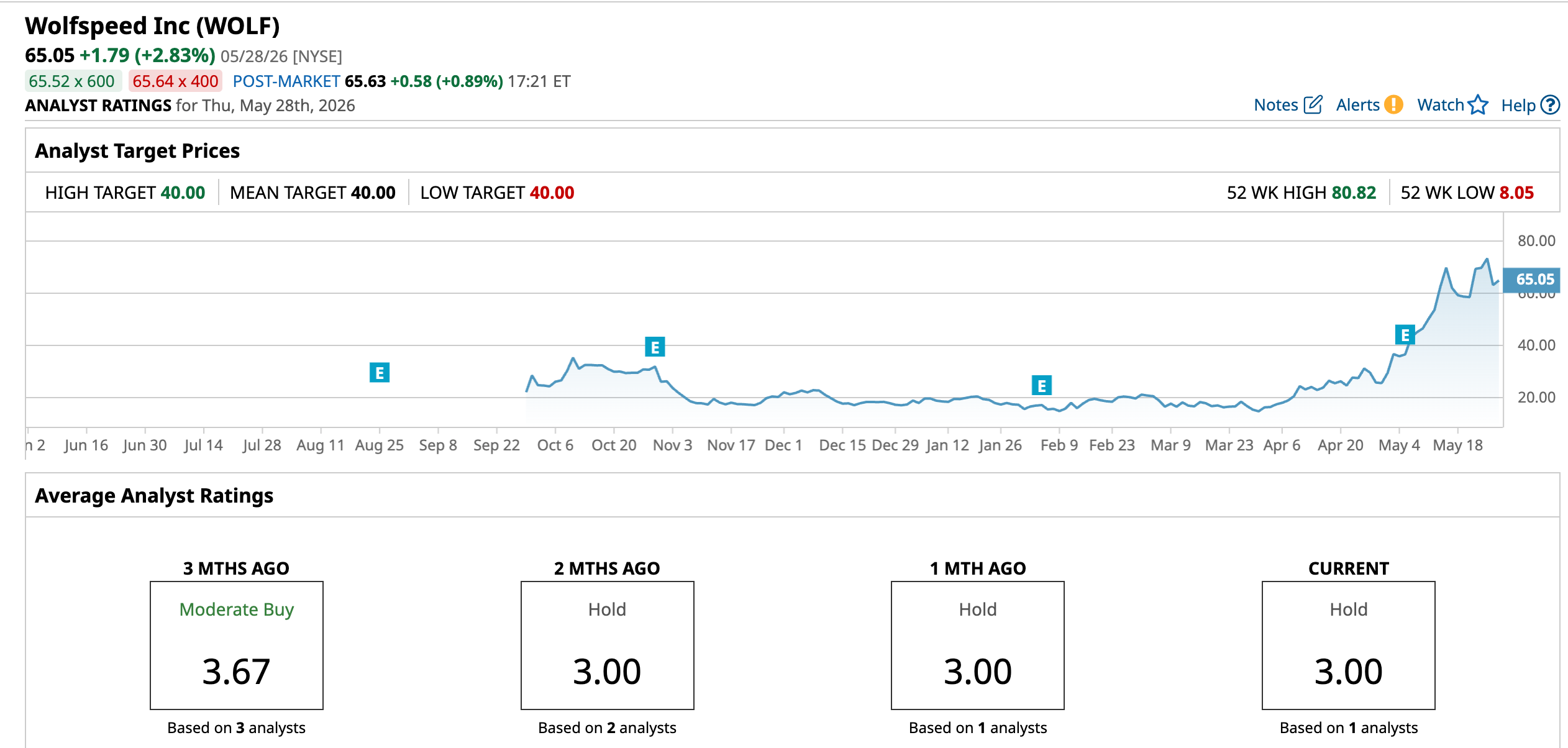

What Do Analysts Expect for Wolfspeed Stock?

Wolfspeed has a consensus “Hold” rating from the one analyst covering the stock. The stock trades well beyond the mean price target of $40.

www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A Giant Short Squeeze Could Be Brewing in Wolfspeed Stock The SpaceX IPO Is a Bet That Retail Investors Love Elon Musk So Much They’ll Fund His Money-Losing Empire You’ve Likely Never Heard of This Stock, But Data Center Demand Just Took Shares to New 52-Week Highs Starbucks’ AI Disaster and Sam Altman’s U-Turn Prove That AI Still Needs Humans