Globus Medical GMED a prominent global player in the musculoskeletal healthcare space, is well positioned to capitalize on the robust expansion of the niche market. According to a report by Market Research Intellect, this market was valued at $15.6 billion in 2025 and is projected to grow at a CAGR of 11.96% from 2026 to 2033, reaching an estimated $38.52 billion by 2033.

The demand backdrop for musculoskeletal care remains supported by an aging population and higher incidence of degenerative conditions and trauma, which should sustain procedure volumes over time. This creates a favorable setup for Globus Medical’s broad implant portfolio across spine and orthopedics. However, the musculoskeletal devices market remains highly competitive. Government cost-containment efforts and tighter hospital budgets can constrain pricing. Large peers across orthopedics and spine continue to invest in technology, which can increase competitive bidding and elongate sales cycles.

Despite these challenges, Globus Medical reaffirmed the full-year 2026 revenue guidance at $3.18-$3.22 billion, supported by its broad product offering and market presence.

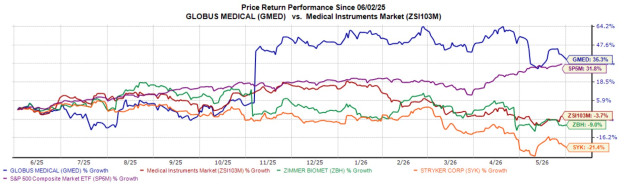

In the past year, Globus Medical’s shares have surged 35.3% outperforming the broader Medical Instrument industry’s decline of 3.7%. The S&P 500 benchmark improved about 31.8% in the same period. During this time, Globus Medical’s key peers, such as Stryker Corporation SYK, known for its orthopaedics, medsurg and neurotechnology products, lost 21.4%, and Zimmer Biomet ZBH recognized for orthopedic reconstructive products, sports medicine and extremities and trauma products, lost 9%.

Image Source: Zacks Investment Research

Major Tailwinds Driving GMED Stock

Musculoskeletal Share Gains Continue: In the first quarter of 2026, worldwide net sales rose 27% year over year, while base business sales, excluding Nevro, increased 13.2%.

U.S. Spine marked its third straight quarter of 10% growth, with double-digit growth cited across standard fixation, minimally invasive surgery pedicle screws, expandable transforaminal lumbar interbody fusion, anterior lumbar interbody fusion, posterior cervical and cervical plating. International Spine grew 16.4% as reported in the first quarter.

Trauma revenues increased 30.4% in the quarter, helped by continued adoption of the core trauma line and the Precice limb lengthening portfolio, with ANTHEM Elbow continuing to exceed expectations, leading the company to ship additional sets to the field in the second quarter.

Steady Pace of Product Development: Globus Medical continues to invest in R&D and product cadence as a core part of its competitive positioning. In the first quarter of 2026, R&D expenses were 4.8% of sales, with management expecting it to be 5-6% of net sales for the full year, with spend ramping methodically through the year as product efforts progress.

The company’s early second-quarter FDA 510(k) clearances for patient-specific lumbar spacers and rods also reinforce its roadmap of linking planning software, enabling technologies and implants into one workflow, which can deepen account relationships and increase procedure-level pull-through over time. This launch activity complements the broader post-merger strategy of compressing development timelines and keeping the portfolio fresh across spine and orthopedics.

Financial Flexibility: The company ended the first quarter of 2026 with $560.9 million of cash and cash equivalents and $68.9 million of short-term marketable securities. The company remains debt-free, which preserves the capacity to fund R&D, sales-force investments and manufacturing expansion without relying on external financing. Liquidity is also being replenished internally, with $202.4 million of operating cash flow generated in the quarter. This supports continued capital spending and buybacks alongside ongoing integration work.

Estimates for GMED Heading South

The Zacks Consensus Estimate for Globus Medical’s 2026 sales and EPS implies a year-over-year improvement of 8.8% and 19.1%, respectively. The bottom-line estimates have moved north by 6.3% in the past 60 days.

Image Source: Zacks Investment Research

GMED’s Downsides

The company operates in an environment of interest-rate uncertainty, inflation and geopolitical complexity that can disrupt supply chains and raise input costs. While adjusted gross margin improved to 69.2% in first-quarter 2026, management’s long-term goal is a mid-70s profile, leaving a limited buffer if costs rise faster than pricing. SG&A was $297.8 million in first-quarter 2026, or 39.2% of sales, up from $242.8 million a year earlier, reflecting higher compensation and benefit costs on higher volume. The company also recorded restructuring costs in the quarter as it continues synergy and integration plans, which could add variability to near-term expense trends.

GMED Stock Valuation

With a forward one-year price-to-sales (P/S) of 3.29X, GMED’s shares are trading at a discount compared with the industry median of 4.52X. It has a Value Score of C at present.

Image Source: Zacks Investment Research

How to Play GMED Stock Now?

Globus Medical continues to benefit from strong execution across its spine, trauma and orthopedic businesses, with robust revenue growth in the first quarter. This growth was driven by market share gains, broad-based procedure growth and continued adoption of newer products. The company’s ongoing R&D investments strengthen its competitive position and supports long-term growth. A debt-free balance sheet, healthy cash generation and ample liquidity provide significant financial flexibility to fund innovation, expansion initiatives and shareholder returns.

However, investors should remain aware of several headwinds. The company operates in a challenging macroeconomic environment which could weigh on profitability.

GMED, currently sporting a Zacks Rank #1 (Strong Buy), has outperformed both the industry and its peers, and its earnings estimates are likely to continue trending upward in the near term. As a result, the stock appears well positioned to deliver attractive long-term returns and investors may view the current level as an attractive entry point.

You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Stryker Corporation (SYK): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Zimmer Biomet Holdings, Inc. (ZBH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).