Global health insurance costs are expected to rise by an average of 10.3% this year, according to WTW’s 2026 Global Medical Trends report. That follows increases of 10% in 2025 and 9.5% in 2024, a run of higher costs that is putting steady pressure on insurers’ margins. Even so, one of the biggest names in the sector is choosing this moment to step up what it returns to investors.

UnitedHealth Group (UNH) is sending a clear message of confidence to its shareholders. On Wednesday, the company announced a 5% dividend increase, lifting its quarterly payout from $2.21 to $2.32 per share. This latest raise marks UnitedHealth’s 16th straight year of growing its dividend.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

With the higher dividend showing management’s belief in cash flow strength and recovery, the key question now is how to read this move. Is it a real turning point that rewards long‑term UNH holders, or mainly a cautious adjustment in a tough environment? Let’s dive in.

UnitedHealth’s Numbers Back Its Dividend

UnitedHealth Group is a diversified health insurance and health services company based in Minnetonka, Minnesota, and runs its business through the UnitedHealthcare and Optum segments in the U.S. and abroad.

The company increased its quarterly dividend to $2.32 per share, with the next payment set for June 23. That puts the forward annualized dividend to $9.28 and translates to a forward yield of about 2.46%.

UNH closed at $398 Thursday, up 20.8% year-to-date and 32.8% over the past 52 weeks.

www.barchart.com

www.barchart.com The company has an equity value of about $343.2 billion and trades at 23.25x trailing 12‑month earnings and 17.87x cash flow, versus sector medians of 15.99x and 13.62x, showing it trades at a premium.

Their most recent quarterly update, released in early April for Q1 of calendar 2026, showed revenue of $111.7 billion. It was 2% higher than the same period a year earlier and about $1.9 billion above analyst estimates. The same report showed adjusted earnings-per-share of $7.23, beating consensus by 9.4%. The company reported adjusted EBITDA of $9.99 billion with an 8.9% margin, which was 5.1% above expectations.

That performance led to a free cash flow margin of 7.3%, up from 4.2% a year earlier, giving management more room to support higher dividends. UNH also generated an operating cash flow of $8.9 billion, down 54.75% year-on-year.

UNH’s Operational Changes

UnitedHealth’s Optum Rx introduced what it calls the industry’s first transparent pharmacy care model, built to give plan sponsors a clearer view of drug costs and pricing structures. This move is meant to link pharmacy benefit spending more directly to actual outcomes, which helps large employers and health plans manage budgets and, over time, can support steadier margins for UnitedHealth.

UnitedHealthcare’s insurance unit is also working to make it easier to get care. It is eliminating most medical prior authorizations and speeding up payments for key rural hospitals and providers nationwide, a shift that should ease some of the reputational and regulatory pressure that large insurers often face.

On top of that, UnitedHealthcare has committed to cutting prior authorization requirements overall by 30%. This step lowers paperwork for clinicians and may lift provider satisfaction, which matters when health systems decide which plans they want to work with.

The company has also expanded its doula offering to employer‑sponsored plans nationwide, with a focus on better maternal health support and more complete benefits for working families. Those targeted benefits may make UnitedHealth’s plans more appealing to large employers that want coverage with clear add‑ons.

All of these actions feed back into the same point as UnitedHealth deepens its role across employers, providers, and members.

Wall Street’s View on UNH’s

Analysts are lining up behind UnitedHealth’s decision, and the numbers they are working with help explain why. Their next earnings update for the current quarter ending June 2026 is scheduled for Aug. 4, with the average earnings estimate at $4.84 per share. That compares with $4.08 a year earlier for the same period and points to an expected year‑over‑year growth rate of 18.63%.

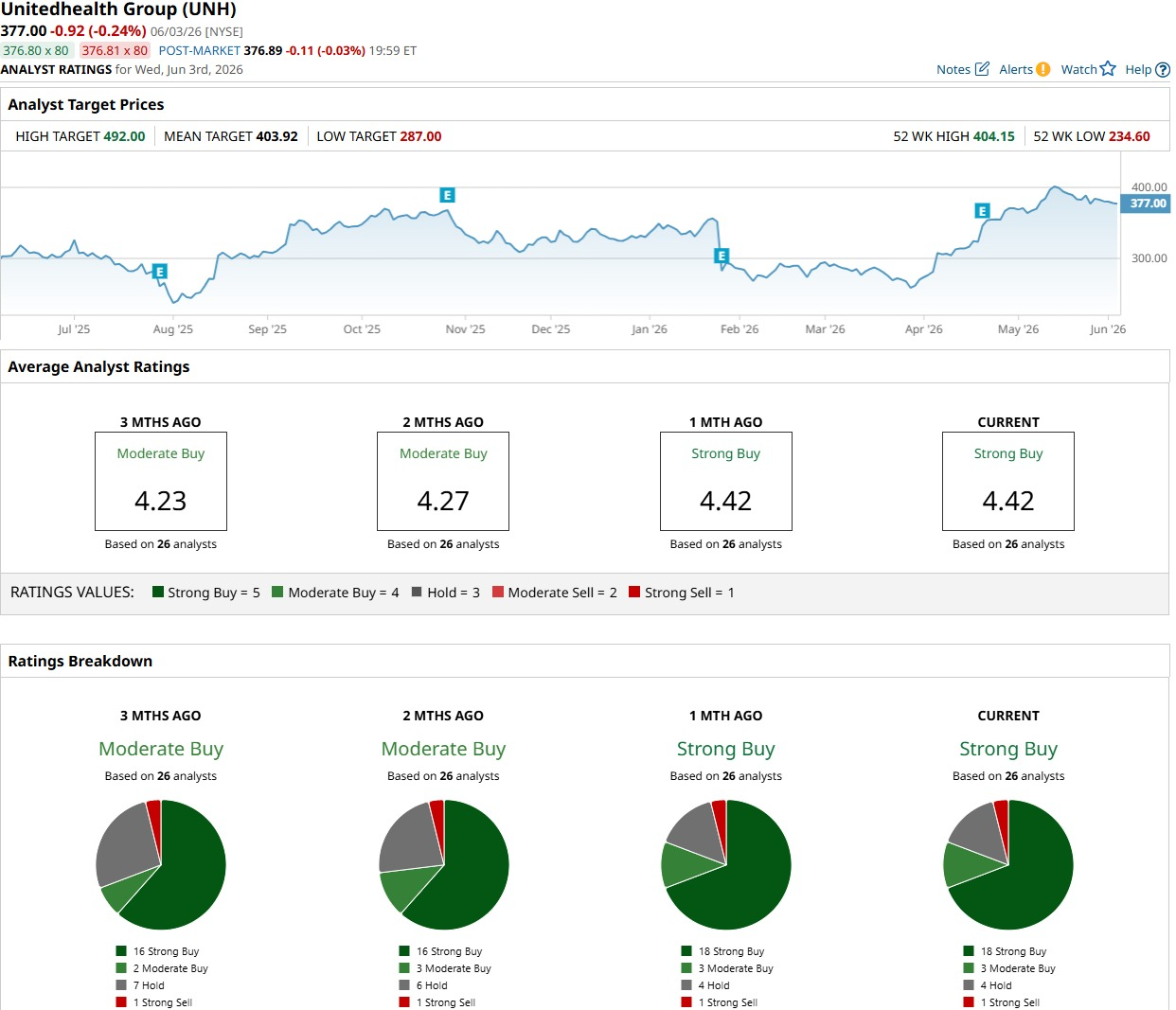

Individual firms are also staying positive. Piper Sandler analyst Jessica Tassan has kept a bullish stance on UnitedHealth and recently raised her price target to $420. Across the analyst community, the latest survey of 26 analysts shows a “Strong Buy” consensus rating. Their average price target is $403.92 per share, implying roughly 2% upside from recent levels.

www.barchart.com

www.barchart.com Conclusion

UnitedHealth’s 5% dividend increase looks well backed by its earnings strength, cash generation, and recent business moves, not like a late‑cycle gesture. Taken together with solid growth forecasts and a broadly positive analyst view, that support makes moderate upside from here a reasonable base case. In that context, total returns are likely to lean on both share price gains and the growing dividend stream.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

UnitedHealth Just Raised Its Dividend 5%. Why You Should Buy UNH Stock Here. Michael Burry Takes Aim at Palantir Stock Again, But He’s Missing the Bigger Picture AVGO Stock Alert: Why Broadcom Is Leading Chip Stocks Lower Today Why 1 Analyst Is Betting DRAM Strength Can Supercharge Sandisk Stock to $3,250