Things may finally be looking up for UnitedHealth (UNH). Shares of the largest health insurer in the United States popped more than 5% in yesterday's trading session after leading broker Bank of America upgraded the company to a “Buy” from “Neutral.” The firm also increased its price target on the stock to $450 from $420, which would entail an upside potential of 12% from current levels.

Even more good news awaited its shareholders when the company recently raised its dividend by 5% to $2.32 per share. Notably, UnitedHealth has been raising dividends consecutively over the past 16 years, and with the latest rise, its stock now offers a dividend yield of 2.34%. Valued at a market cap of $360 billion, UNH stock is up 21.7% on a YTD basis.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com About UnitedHealth

With its founding days going back more than five decades, UnitedHealth is no longer simply an insurance company. Through its Optum division, it has become a healthcare ecosystem spanning insurance, pharmacy benefit management, health care delivery, data analytics, and technology services.

However, the company has been struggling of late. Thus, on the back of its newfound confidence due to its latest quarterly earnings and armed with an upgrade from Bank of America, can UNH stock finally make a comeback? Let's find out.

Greenshoots Visible

Growth may not be one of the defining features of a company like UnitedHealth, especially after substantial pruning of its non-US businesses and realignment of focus towards its domestic operations. However, stability is.

For Q1 ended March 31, 2026, UnitedHealth delivered revenues of $111.7 billion. This marked a growth of just 2% from the previous year. Yet, earnings, which saw three straight quarters of yearly declines, managed to remain flat at $7.23 per share (vs $7.20 per share in the year-ago period). Further, this was above the consensus estimate of $6.58 per share, marking the third consecutive quarter of earnings beat from the company.

The medical care ratio, a key metric that tracks how much of the premium revenue an insurer spends on actual medical claims, dropped to 83.9% from 84.9% in the same period a year ago.

Cash flow from operations rose considerably to $8.9 billion from $5.5 billion in the prior year, as the company closed the quarter with a mammoth cash balance of $31.2 billion. This was much above its short-term debt levels of $6.5 billion.

Meanwhile, UNH is also trading at reasonable levels. While its forward P/E of 20.52x is near the sector median of 16.89x, the forward P/S and P/CF of 0.77x and 15.82x are also within the range of sector medians of 3.48x and 13.67x, respectively.

On the Right Path

A recent headline that grabbed attention was Berkshire Hathaway's exit from UNH stock. However, context is required. When Berkshire built up its stake in the company, its shares were in the doldrums. Now, CEO Greg Abel and his team were sitting on sizeable profits from this position and therefore lightened it to perhaps divert the funds toward tech stocks, as evidenced by the company's latest buy of Alphabet (GOOGL) (GOOG) shares.

Thus, it is certainly not an indictment of the company's capabilities, which are now increasingly being powered by AI and AI-led efficiencies.

The efficiency gain was visible in the fall in the medical cost ratio, reflecting that the $1.5 billion investment in AI is showing positive signs.

Further, Optum Real, the company's AI-first claims adjudication and coverage validation platform, is on track to process 2.5 billion transactions in 2026, having already cleared 500 million year-to-date as of the Q1 call. The platform cuts manual contact costs by 76%, a figure management cited directly during that call.

Notably, it should be taken into account that manual claims handling has historically been one of the most expensive, error-prone, and time-consuming layers in American health care administration. Replacing it at that scale and that level of efficiency improvement is not a marginal gain.

All this is made possible by a seamless AI-led backend. Nearly 95% of prior authorization requests now arrive electronically, roughly half are processed in real time, and more than 90% clear within one business day, according to the earnings call. Authorizations submitted through Digital Authorization, the new prior auth platform, are hitting a 96% approval rate. On the pharmacy side, the PreCheck MyScript tool has cut prescription approval time from over eight hours to under 30 seconds and drives a 68% reduction in denials tied to missing information. Optum Insight, the segment commercializing these AI capabilities externally, saw new product launches in Q1, including AI-powered claims processing tools capable of improving productivity by over 20% for revenue cycle management customers.

Finally, apart from these nimble moves, UnitedHealth will be difficult to dislodge from its apex position when one considers its presence across the overall health care chain. UnitedHealth owns insurance and pharmacy benefits management through Optum Rx, with 1.67 billion adjusted scripts annually, and a value-based care delivery network through Optum Health serving 5 million patients. Moreover, the company's 2026 Medicare Advantage plans are still available to 94% of Medicare-eligible beneficiaries, preserving its position as the nation's largest Medicare Advantage carrier by total plan enrollment.

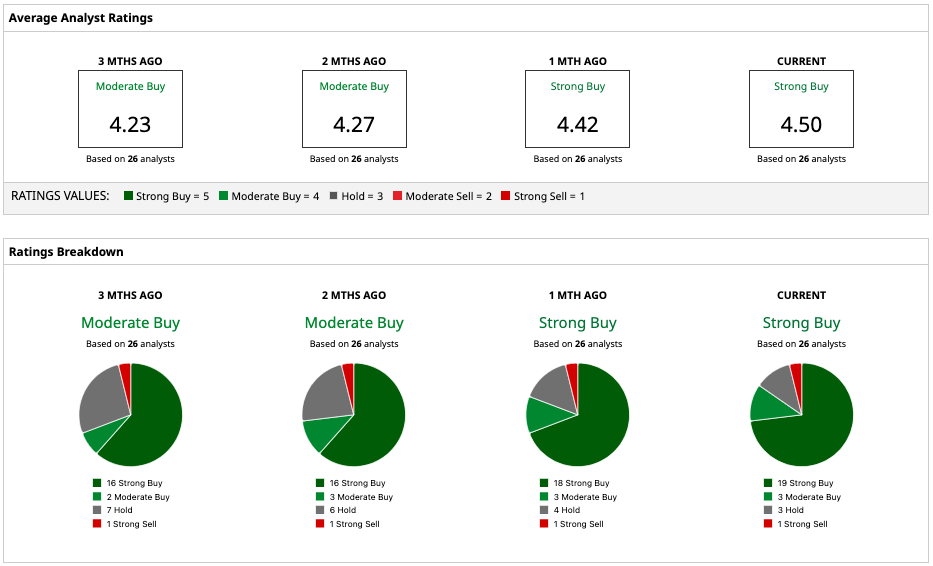

Analyst Opinion

Thus, analysts have deemed UNH stock to be a “Strong Buy.” The mean target price of $403.92 indicates an upside potential of about 0.74% from current levels. Out of 26 analysts covering the stock, 19 have a “Strong Buy” rating, three have a “Moderate Buy” rating, three have a “Hold” rating, and one has a “Strong Sell” rating.

www.barchart.com

www.barchart.com On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Morgan Stanley Revamps Its Dell Stock Price Target After Blowout Earnings. Dell Is Expanding Beyond the AI Boom. Subdued Put Activity Signals Opportunity in 4 Cash-Secured Puts for Income and Value Dell Stock Looks Poised to Keep Climbing. Here’s Why. How to Play QNT Stock After the Quantinuum IPO