Microsoft (MSFT) stock has underperformed its peers so far in 2026. Shares of this technology giant have fallen about 20%, lagging rivals such as Alphabet (GOOG) (GOOGL), whose stock has increased by more than 14% amid artificial intelligence (AI) enthusiasm, and Amazon (AMZN), which is up about 4% year-to-date.

Moreover, MSFT stock has also lagged the broader index, with the S&P 500 Index ($SPX) gaining more than 7% so far in 2026.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Microsoft remains one of the biggest beneficiaries of the AI revolution, but investors are becoming increasingly concerned about the enormous cost of staying ahead. The company is expected to spend $190 billion on capital expenditures in 2026 as it expands data centers and AI infrastructure to support future growth.

While those investments could strengthen Microsoft's competitive position over the long term, they are also putting pressure on profit margins today. For instance, Microsoft’s gross margin was down year over year during the last reported quarter, reflecting aggressive investment in AI infrastructure and growing AI product usage. Investors hoping for faster returns are growing impatient as spending continues to rise.

Adding to those concerns, management has guided for only modest near-term acceleration in Azure growth. At the same time, ongoing supply constraints — particularly around AI infrastructure capacity — are expected to persist through at least 2026, limiting Microsoft's ability to fully capitalize on demand.

The result is a growing disconnect between Microsoft's massive AI ambitions and the pace at which those investments are translating into financial results.

That disconnect has weighed heavily on investor sentiment and helped make Microsoft one of the weakest-performing mega-cap technology stocks this year.

www.barchart.com

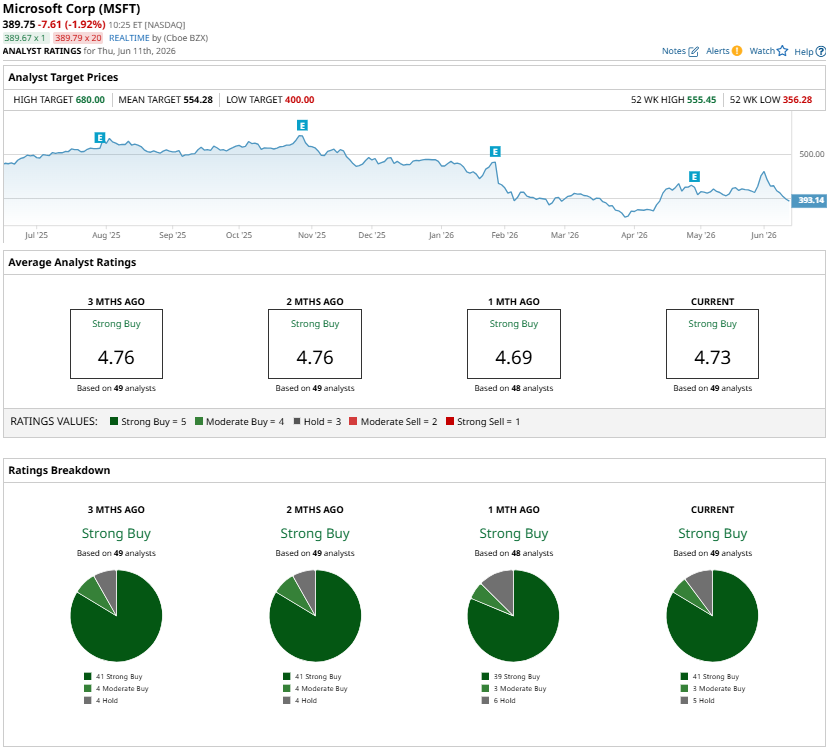

www.barchart.com Is MSFT Stock a Buy, Hold, or Sell?

Despite recent stock underperformance, Microsoft remains one of the best-positioned companies to capitalize on the booming AI and cloud computing markets. While the market has focused on the company's heavy spending on AI infrastructure, the underlying business continues to deliver strong results.

In its latest quarter, Microsoft reported revenue of $82.9 billion, up 18% year-over-year. Microsoft Cloud revenue jumped 29% to $54.5 billion. Azure, the company’s flagship cloud platform, grew 40% as enterprises increasingly adopt AI-powered solutions.

Management highlighted that customer demand for AI services continues to exceed available capacity, suggesting growth is currently limited by infrastructure constraints.

That demand is also reflected in Microsoft's backlog. Commercial remaining performance obligations (RPO) surged 99% to $627 billion, with about one-quarter expected to convert into revenue over the next year. Longer-term commitments climbed 138%, indicating customers are making significant multi-year investments in Microsoft’s cloud and AI ecosystem.

The company’s AI business is now generating an annual revenue run rate of more than $37 billion, up 123% from a year ago. Adoption of Microsoft Copilot is accelerating rapidly, with paid seats exceeding 20 million. The number of organizations deploying more than 50,000 Copilot seats has quadrupled, highlighting growing enterprise-scale adoption.

Looking ahead, management expects momentum to continue. Azure is projected to maintain growth near 40%, while additional AI infrastructure coming online could further boost growth.

From a valuation standpoint, Microsoft remains attractive given its leadership in enterprise software and cloud computing, as well as its massive AI opportunity. Further, it trades at a forward P/E ratio of 24.6x, which compares favorably to Amazon’s 31.8x and Alphabet’s 25.2x.

Plus, Microsoft pays a dividend yield of 0.90% and is on track to join the list of Dividend Aristocrats next year.

Wall Street is bullish about Microsoft's prospects, with analysts continuing to assign the stock a “Strong Buy” rating.

www.barchart.com

www.barchart.com The Bottom Line

Microsoft's underlying business remains strong. Cloud demand continues to grow at a healthy pace, AI adoption is accelerating across its ecosystem, and the company's expanding backlog provides strong visibility into future revenue growth. While concerns around elevated AI spending and near-term capacity constraints have pressured sentiment, these challenges appear temporary.

With multiple growth drivers in place and management maintaining a positive outlook, Microsoft stock remains a Buy and is well-positioned to deliver attractive shareholder returns.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Microsoft Stock Trails Rivals in 2026. How to Play MSFT Stock Here. Virgin Galactic Stock Leads Space Stocks Higher Ahead of SpaceX IPO The SpaceX IPO: Why I Think Next Week, Not Friday, Is the Real Event Crocs Stock Has Rallied 45% YTD. Baird Says It’s Not Done Yet.