Micron Technology (MU) is a Boise, Idaho-based global memory and storage semiconductor company founded in 1978, and one of only three manufacturers in the world capable of producing cutting-edge DRAM and NAND flash memory at scale.

What has transformed Micron from a volatile commodity chipmaker into a must-own AI infrastructure stock is simple: every Nvidia (NVDA) GPU requires High Bandwidth Memory, and Micron (alongside SK Hynix and Samsung) is one of the only companies on the planet that can supply it. CEO Sanjay Mehrotra declared that in the AI era, memory has become a strategic asset for customers, and the numbers back that up emphatically.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

MU Stock

Micron Technology has delivered a staggering total return of 760% over the past 12 months, with a year-to-date (YTD) total return of 250% in 2026, placing it firmly in the top 1% of all Nasdaq performers, while the S&P 500 Index ($SPX) returned approximately 22% over the same period. On June 3, the stock hit an all-time high of $1,089.29, surging from a 52-week low of just $103.38, a nearly 10x move fueled by the AI HBM supercycle, record earnings, and S&P 100 Index ($OEX) inclusion.

Against the S&P 500 Information Technology Index ($SRIT), MU has dramatically outpaced the broader tech sector in 2026, cementing its status as the defining AI memory momentum trade of the current market era.

www.barchart.com

www.barchart.com Micron Delivers Top Results

Micron reported Q2 FY2026 revenue of $23.86 billion, nearly triple the $8.05 billion reported a year earlier, decisively beating the analyst consensus of $20.07 billion by approximately 19.5%, while adjusted EPS of $12.20 surpassed the Street estimate of $9.31 by approximately 31%. DRAM revenue surged to $18.8 billion, and NAND revenue reached $5.0 billion, both reflecting explosive demand from cloud hyperscalers building out AI computing infrastructure at an unprecedented pace. The quarter set new company records across revenue, gross margin, EPS, and free cash flow simultaneously.

Non-GAAP gross margin expanded to 75%, while adjusted free cash flow reached $6.9 billion, a figure that exceeds Micron's entire annual revenue as recently as fiscal 2024. Capital expenditure guidance was raised by $5 billion to over $25 billion for fiscal 2026, with spending expected to rise further into 2027 as Micron accelerates construction of its Taiwan and U.S. fabrication facilities. Reflecting confidence in the sustained strength of its business, the board approved a 30% increase in the quarterly dividend.

For Q3 FY2026, management guided revenue of approximately $33.5 billion, implying 40% sequential growth and over 200% year-over-year (YOY) growth, with non-GAAP gross margins guided at approximately 81% and adjusted EPS of $19.15.

"Micron set new records across revenue, gross margin, EPS, and free cash flow in fiscal Q2, driven by a strong demand environment, tight industry supply, and our strong execution, and we expect significant records again in fiscal Q3," CEO Sanjay Mehrotra stated in the quarterly report. If achieved, Q3 guidance would imply Micron generating over $27 billion in gross profit in a single quarter, marking one of the most profitable quarters for any memory company in history.

Micron Surges on Iran Breakthrough

Micron shares surged more than 6% on Thursday as President Trump announced a breakthrough in U.S.-Iran negotiations, cancelling scheduled military strikes and triggering a broad-based rally across semiconductor stocks. The geopolitical relief trade provided an additional tailwind to Micron, which was already gaining ground on a major price target upgrade from Wolfe Research, raising its target to $1,250 from $550, signaling 25% upside from the market price, citing rising memory prices and strengthening visibility into demand.

Wolfe analysts highlighted that cleanroom capacity constraints will limit bit shipment growth at least through 2027, creating a structurally tight supply environment, while demand growth is being driven above prior estimates by stronger server shipments, predominantly attributed to agentic AI and CPU-driven inference workloads. The combination of easing geopolitical risk and tightening memory supply dynamics reinforces Micron's position as one of the most compelling AI infrastructure plays in the semiconductor sector.

Buy The Dip or Wait for More?

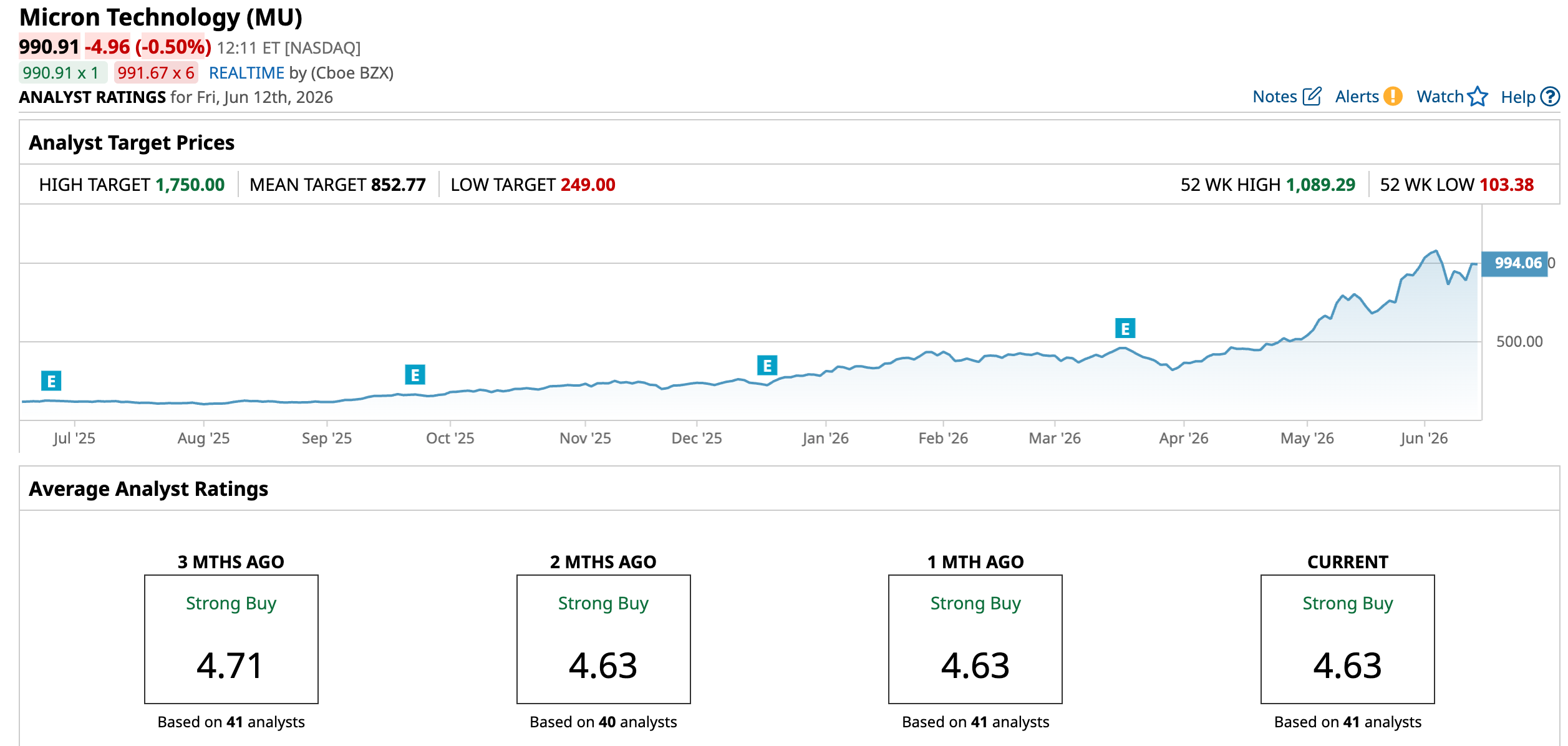

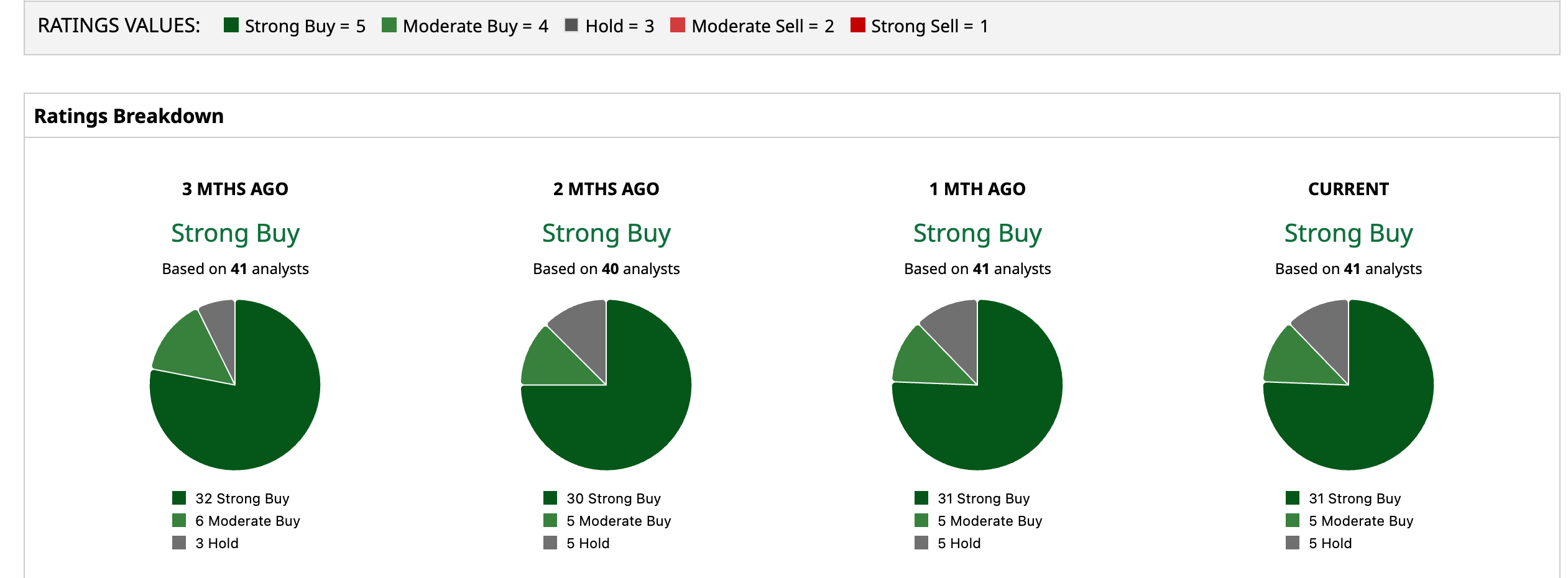

With geopolitical tailwinds from the breakthrough in Iran, Wolfe Research's landmark $1,250 price target upgrade, and Q3 FY2026 guidance pointing toward one of the most profitable quarters in the memory industry's history, Micron's bull case has rarely been stronger. However, Wall Street's consensus reflects a stock that has significantly outpaced near-term fair value. MU carries a "Strong Buy" rating across 41 analyst ratings, comprising 31 "Strong Buy," 5 "Moderate Buy," and 5 "Hold," with a mean price target of $852.77, implying approximately 13.94% downside from current levels. But the Street-high price point of $1,750 indicates a possible 76.6% upside from here.

For long-term investors, MU remains the definitive AI memory supercycle compounder, but disciplined entry points following pullbacks offer the most attractive risk-reward setup.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Iran Ceasefire and a $1,250 Price Target: How to Play Micron Stock Here CubeSmart Stock Is Primed for a Breakout – and It Pays You to Wait with a 5.1% Dividend Yield Waymo Is Doubling Down on Self-Driving Car Ambitions. What That Means for GOOGL Stock. These 2 Dividend Stocks Just Boosted Their Payouts by 13% — And More Income Growth Could Be Ahead