Dividend yields can be perplexing at times, given the two moving parts: the dividend payout, the numerator in the equation, and the stock price, the denominator. More often than not, companies with very high dividend yields are in trouble, and the high yield is due to a crash in their share prices.

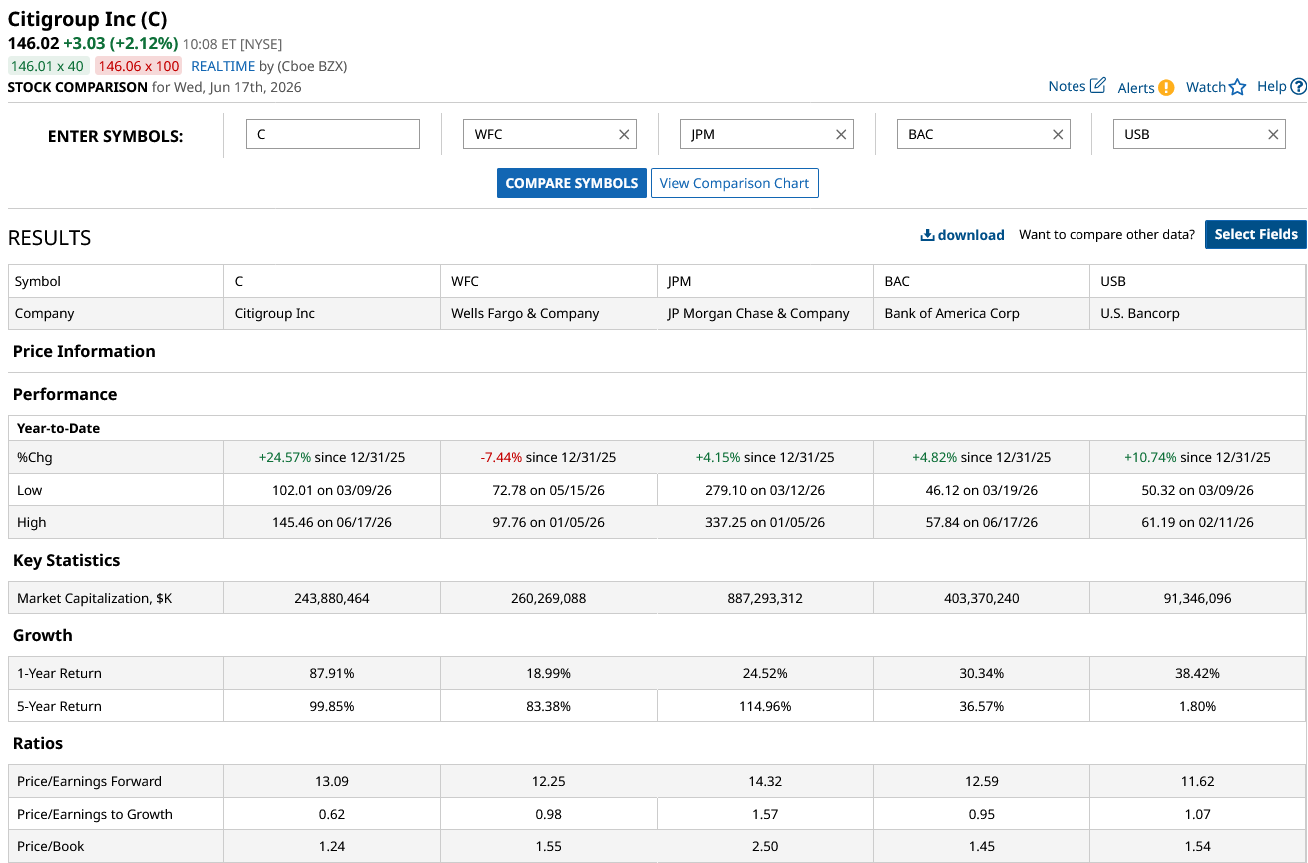

Citigroup (C) is a case in point here. The stock’s dividend yield was well north of 4% when I started covering it in 2023. At that point, its large-cap banking peers, including Bank of America (BAC), J.P. Morgan Chase (JPM), and Wells Fargo (WFC), which, along with Citi, are the top four U.S. banks by assets, had a dividend yield in the ballpark of 2.5%.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Citi’s Dividend Yield Now Trails Major Banks

Cut to 2026, and Citi’s dividend yield has fallen to 1.7%, which, while still higher than the S&P 500 Index ($SPX), is the lowest among the top four U.S. banks. Citi has gradually increased its payouts over the period, but the current dividend yield is now just about a third of what it was in late 2023. The fall in dividend yield could be attributed to the over 275% rise in C stock from its 2023 lows. The stock has consistently outperformed major banks over the last couple of years as markets gave a thumbs-up to the transformation under CEO Jane Fraser.

Citi was a literal no-brainer in 2023. It was trading below its tangible book value and less than half of its total book value while offering a dividend yield of over 4%. However, its valuation multiples have expanded amid the rally over the last three years. The stock had long run ahead of its tangible book value and has now even surpassed its book value, which was $112.22 at the end of Q1 2026. However, Citi’s price-to-book value multiple is still the lowest among large banks even though the gap has narrowed significantly.

www.barchart.com

www.barchart.comCiti’s Return Ratios Have Improved

Citi has been trading at a discount to its peers for a reason. First, its return and profitability metrics are still lower than those of its peers. For instance, Citi’s return on average tangible common equity (RoTCE) was 7.7% in 2025. For context, Bank of America reported a RoTCE of 14.2% last year, while the corresponding number for J.P. Morgan Chase was 20%.

Second, the bank had a complex business, and it was too spread out. Moreover, it has faced regulatory issues more often than other large banks and has had a much higher Stress Capital Buffer (SCB).

Citi’s Turnaround

Meanwhile, Citi’s turnaround has had a visible impact, and the company has exited several non-core markets, flattened its organizational structure, reduced bureaucracy, and is working to address the underlying issues that have put it in the crosshairs with regulators in the past.

The management is optimistic about achieving an RoTCE of between 10% and 11% this year, which it expects to further increase to between 14% and 15% over the medium term once it reaches “steady state” and exits the legacy portfolio. The company has streamlined its business into five verticals, which are Banking, Wealth, Markets, Services, and Cards. The company is also using artificial intelligence (AI) for various purposes, including automation and fraud detection.

The company’s turnaround actions have led to higher earnings and freed up capital, which it has been using to reward shareholders. Last year, it returned over $17 billion to shareholders in the form of dividends and share repurchases. The company repurchased a record $6.3 billion worth of shares in Q1 2026 and is nearing the completion of the $20 billion buyback that it announced last year. At the investor day last month, Citi announced a new $30 billion repurchase plan.

One area where the bank still has some work to do is on the regulatory front, as its SCB is still higher compared to other large U.S. banks. Notably, Citi has had a higher SCB as its business was more complex and globally spread out. Its large credit card portfolio is also among the reasons behind higher capital requirements. However, its SCB dropped to 3.6% last year compared to 4.3% in 2023, and the management expects it to drop even further.

Should You Buy C Stock?

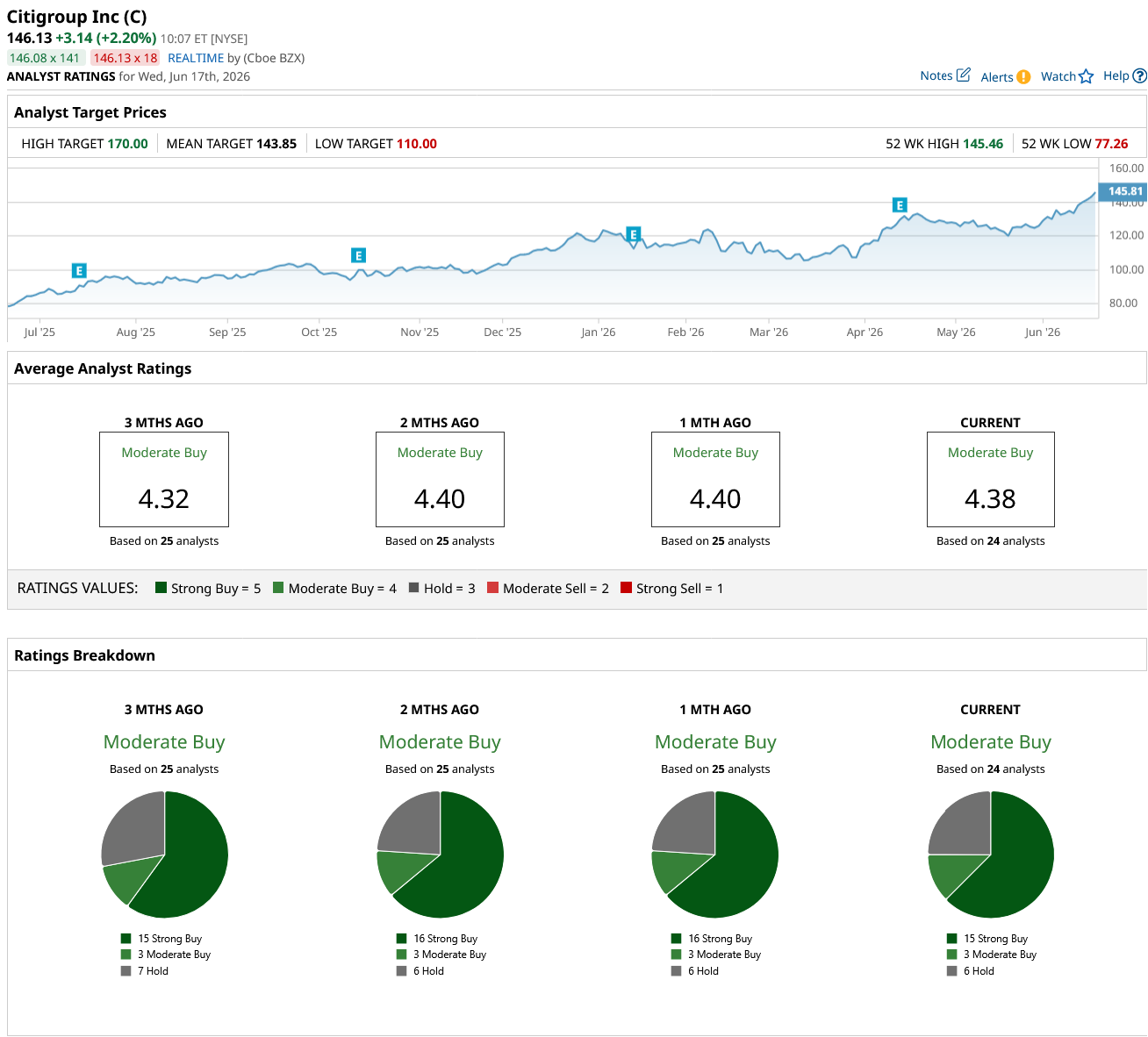

C stock now trades quite close to its mean target price, while the Street-high target price of $170 is 16% higher than current price levels. The sell-side analyst community has been gradually warming up to Citi as the company has shown visible and remarkable progress in its transformation.

I have a slightly bullish view on Citi and expect it to add to its year-to-date (YTD) gains. However, there isn't much margin of safety in this once-beaten-down name now, and we shouldn't be expecting the kind of outsized returns we saw over the last couple of years.

www.barchart.com

www.barchart.com On the date of publication, Mohit Oberoi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Citigroup’s Dividend Yield Now Trails Its Peers, But I’m Still Bullish Target Hiked Its Dividend by 1.8%. It’s Not Enough to Change the Thesis for TGT Stock. General Motor’s Battery Pivot Could Change Everything for GM Stock Clorox Has Fallen 22% and Now Yields 5%. This Dividend King Looks Too Cheap to Ignore.