The commodity complex didn't make a lot of sense early Tuesday morning, or should I say less sense than usual.

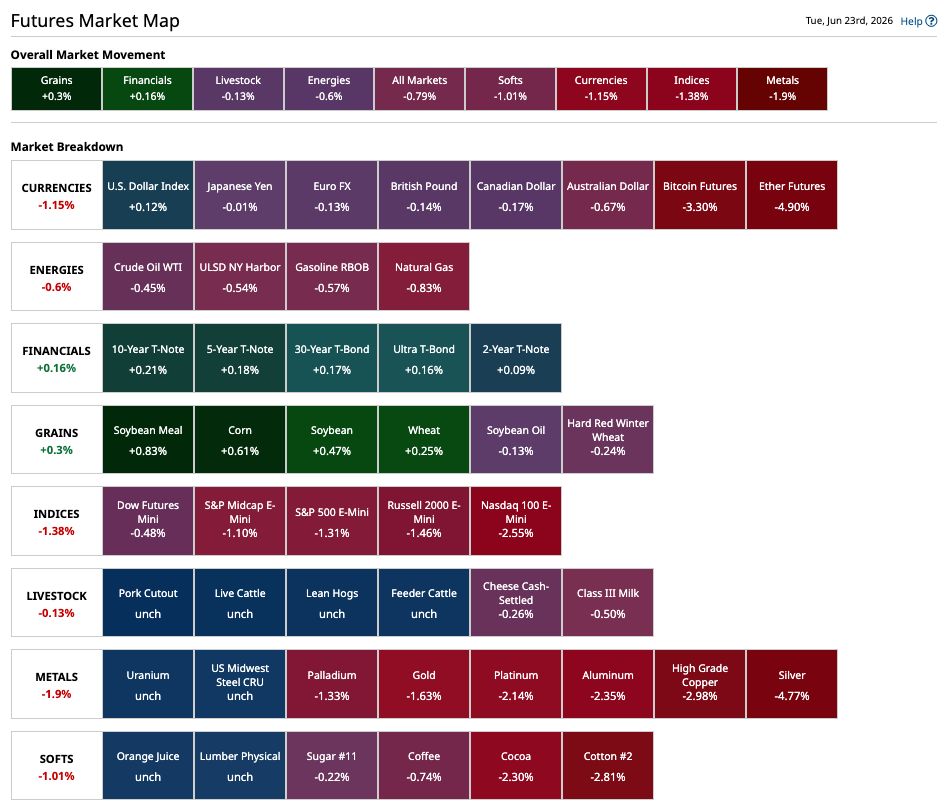

The two sectors in the green to start the day were Financials (US Treasury futures) and Grains, neither having a fundamental reason for buying interest.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

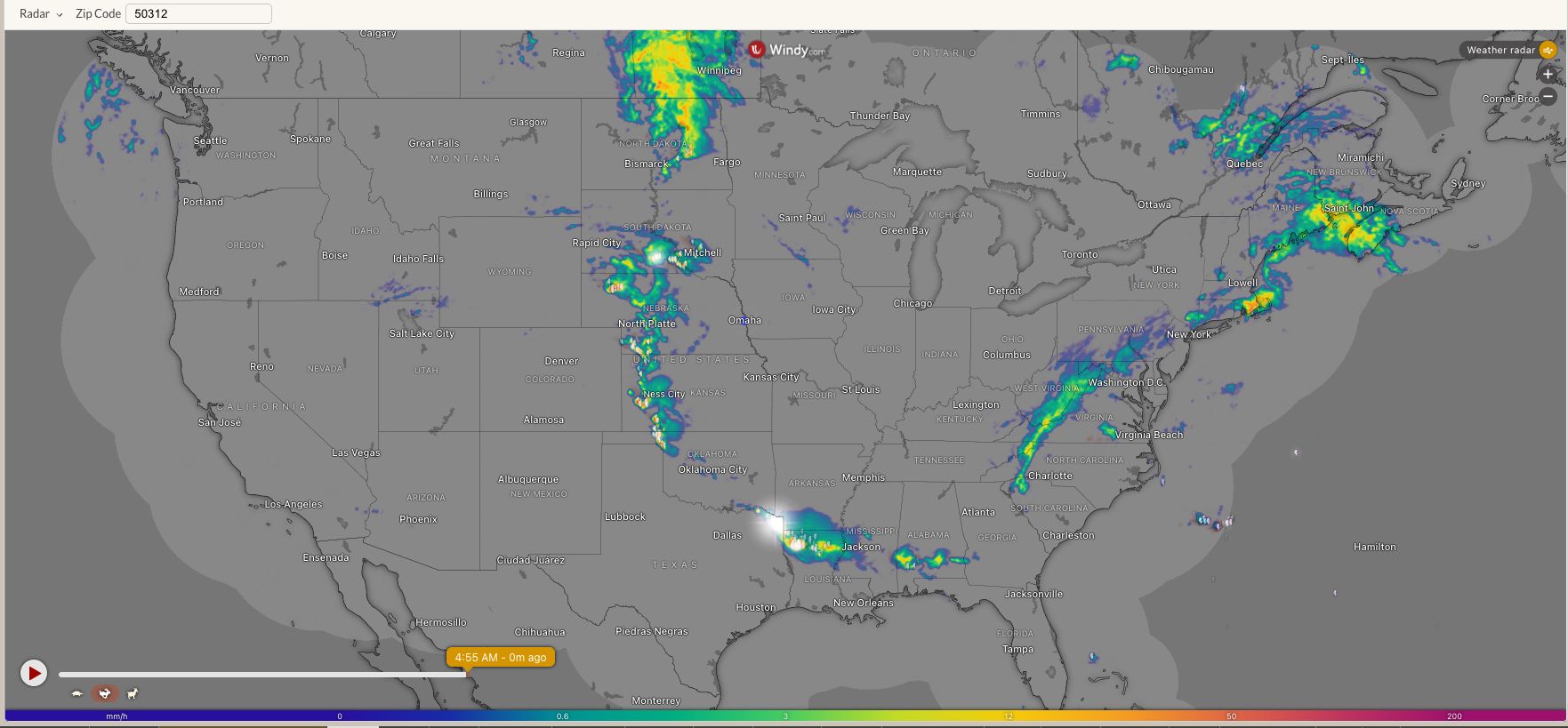

Speaking of Grains, more rains are expected across the Plains and western Corn Belt Tuesday.

Morning Summary: After running through the various sectors of the commodity complex pre-dawn Tuesday, I turned to the piece of blank electronic typing paper to write today’s Morning Commentary. And came up with nothing. Sometimes when I stare at the blank page, the words come tumbling out. Other times, like this morning, all I see is a picture of a polar bear in a blizzard. So, I made myself a second cup of coffee, looked out the window into the Midwest darkness, and wondered aloud into the quiet of the home office about my choice of profession (albeit 40 years too late). Returning to the keyboard, a look at the Barchart Futures Market Heat Map showed all but two sectors in the red. However, the two in the green – Grains and Financials (US Treasury futures) – should have been in the red if markets made sense these days. Recall the outlook is for the US Fed to raise rates in 2026, meaning yields should go up and prices down. As for Grains, another rain system is moving across the Plains early Tuesday morning, expected to make its way beyond the Missouri River as the day progresses. US stock index futures (ESU26) (NQU26) (YMU26) were under pressure following a lower close to Asian markets while Europe is lower at midday.

Corn: As I mentioned, the Grains sector was in the green to start the day with its leader – King Corn – showing quiet gains across the board. July (ZCN26) was up 2.5 cents after adding as much as 3.0 cents overnight with September (ZCU26) also showing a gain of 2.5 cents. Recall Monday’s session saw July close 6.0 cents lower while September was down 5.5 cents. Last night saw the National Corn Index come in at roughly $3.8125, down about 6.0 cents for the day. In other words, the commercial side was not bothered by Monday’s selloff in the old-crop market, keeping national average basis weak with the end of June growing larger on the horizon. As for new-crop, having already mentioned the hybrid September issue, December (ZCZ26) was also up 2.5 cents, 0.5 cent off its overnight high at this writing. Again, Tuesday’s forecast does not look threatening. As for the extended outlook, the latest 6-to-10-day, for June 28 through July 2, shows heat intensifying over the Midwest. Should Watson be concerned by this? Well, logical people will recall the summer solstice was seen this past Sunday, meaning summer has officially arrived, and summer means it is supposed to be hot. But what do I know.

Soybeans: As evidenced by the solid rally in soybeans overnight through early Tuesday morning. After closing 7.0 cents lower to open the week, the July issue (ZSN26) rallied as much as 8.0 cents overnight and was sitting 7.0 cents in the green at this writing. Recall from yesterday’s Afternoon Commentary when I posed the question of how much the pressure might’ve come from the commercial side given the first Jar Jar Binks contract (August) (ZSQ26) closed 5.75 cents lower for the day. The National Soybean Index came in last night down about 6.5 cents, splitting the difference between the two, not really answering the question. So, we’ll see how today unfolds and call what we saw overnight Turnaround Activity for lack of anything better to say. I want to take a moment to mention the latest Commitments of Traders numbers. As of Tuesday, June 16, the noncommercial net-long futures position decreased by 32,855 contracts despite futures closing higher from Tuesday to Tuesday. Recall July was up 16.25 cents with August up 15.75 cents and the more heavily traded November showing a gain of 14.5 cents. Some of this could be due to the awkward switch from old-crop to new-crop, or possibly a reflection of increased commercial support.

Wheat: The wheat sub-sector was in the green to start the day, mostly, with the outlier this time around the HRS market. Here we see the September issue (MWU26) sitting 1.25 cents in the red after sliding as much as 5.0 cents overnight while registering – are you ready for this? – 275 contracts changing hands. In other words, anything could still happen by the time Tuesday morning’s intermission rolls around. The September SRW issue (ZWU26) was up 2.75 cents after closing 6.5 cents in the red to open the week. Last night saw the National Index come in about 6.25 cents lower for the day hinting at slight support from merchandisers, most likely due to rains across the US Midwest SRW growing area slowing harvest. Still, the September-December futures spread closed yesterday covering a bearish leaning 69% calculated full commercial carry, so there’s that to keep in mind. Over in HRW we see the September issue (KEU26) up 0.75 cent pre-dawn after adding as much as 3.5 cents overnight on trade volume of 3,500 contracts. Another look back at Monday’s session and we see September fell as much as 12.75 cents before closing 11.25 cents lower for the day. The National Index came in 10.75 cents lower for the day.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Was Tuesday Morning Like a Picture of a Polar Bear in a Blizzard? Stock Index Futures Plunge as Tech Selloff Rages On, U.S. PMI Data in Focus Stocks Set to Open Mixed as Investors Weigh U.S.-Iran Progress, PCE Inflation Data and Fed Speak Awaited The Quiet Revolution at the Fed: The U.S. Banking Sector Received a Catalyst More Potent than Rate Cuts