Popular coffeehouse chain Starbucks Corporation (SBUX) is reportedly developing in-house software that uses artificial intelligence (AI) to decrease its reliance on outside software vendors. Starbucks depends upon a Microsoft (MSFT) system that tracks inventory and an International Business Machines (IBM) tool that manages maintenance. According to a Bloomberg report, the company’s AI-based software is set to roll out by the end of next year, which could reduce its dependence on these software giants.

Right now, Starbucks is spending about $400 million a year on software, which is expected to be reduced with the help of AI. The company is reportedly examining every contract and service as part of a wider plan to reduce costs by $2 billion. While software stocks did not take the news kindly, SBUX’s stock gained 2.54% intraday on July 9 as a result of this.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Starbucks Stock

Headquartered at the Starbucks Center in Seattle, Washington, Starbucks is one of the world’s largest coffeehouse chains. The company operates a broad network of company-owned and licensed stores across major markets, supported by wholesale and consumer-packaged goods businesses.

It has continued to refine its store portfolio while expanding drive-thru and international locations, strengthening digital ordering and loyalty engagement, and responding to inflation-related cost pressures. These recent developments reflect Starbucks’ effort to balance growth, customer experience, and profitability in a competitive global market. The company has a market capitalization of $121.28 billion.

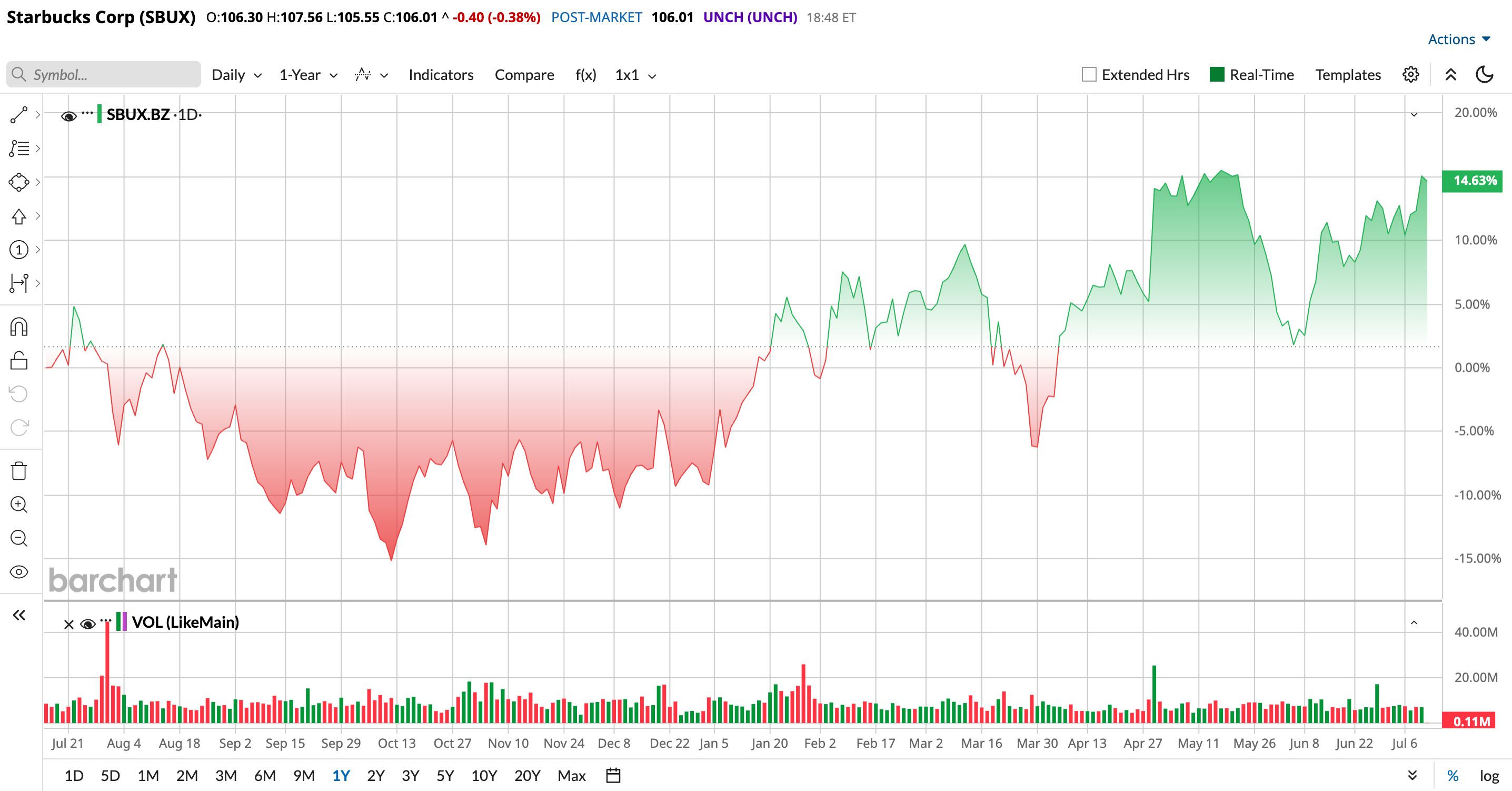

Investors also responded positively to CEO Brian Niccol’s “Back to Starbucks” plan, which focuses on simpler menus, faster service, better staffing, and upgraded in-store execution. Over the past 52 weeks, Starbucks’ stock has gained 11.4%, while it is up 25.9% year-to-date (YTD). The stock had reached a 52-week high of $108.88 on May 14, but is down 2.6% from that level.

www.barchart.com

www.barchart.com On a forward-adjusted basis, Starbucks’ price-to-earnings (non-GAAP) ratio of 44.67 times is quite a lot higher than the industry average of 15.75 times.

Starbucks Q2 Results: Sales Trends, Margin Pressure and Turnaround Efforts in Focus

For the second quarter of fiscal 2026 (quarter ended March 29), Starbucks reported a 6.2% growth in global comparable store sales. This was primarily driven by a 3.8% increase in comparable transactions and a 2.3% increase in average ticket. The North American segment pulled its weight, with comparable store sales in the region growing by 7.1%, primarily driven by a 4.4% increase in comparable transactions and a 2.6% increase in average ticket.

Starbucks’ net revenues increased 8.8% year-over-year (YOY) to $9.53 billion, led by a 7.3% growth in net revenues from company-operated stores. However, after excluding significant operating expenses, its operating income amounted to $828.10 million. In the North American segment, the company’s operating income decreased by 9.1% YOY to $679.90 million. Starbucks’ overall non-GAAP EPS increased by 22% annually to $0.50.

For fiscal 2026, Starbucks expects global and U.S. comparable store sales growth of 5% or greater, while consolidated net revenues are expected to remain flat YOY. Analysts believe Starbucks can further improve its bottom line. For the current fiscal year, its EPS is expected to grow 12.7% YOY to $2.40, followed by a 27.9% increase to $3.07 for the next fiscal year. For the third quarter, analysts expect the company’s EPS to grow 30% to $0.65.

What Do Analysts Think About Starbucks’ Stock?

In May, following a decisive earnings beat in the second quarter of fiscal 2026, analysts at TD Cowen upgraded the stock from “Hold” to “Buy” and raised the price target from $106 to $120. TD Cowen analysts reported seeing “numerous tangible drivers” that should fuel positive sales revisions against a strong category backdrop.

In the same month, Stifel analysts raised the price target on Starbucks from $115 to $117, while maintaining a “Buy” rating on its stock. The financial model was modified to include the joint venture with Boyu Capital in China. Historical operating income for the China business is available, but major uncertainties still exist.

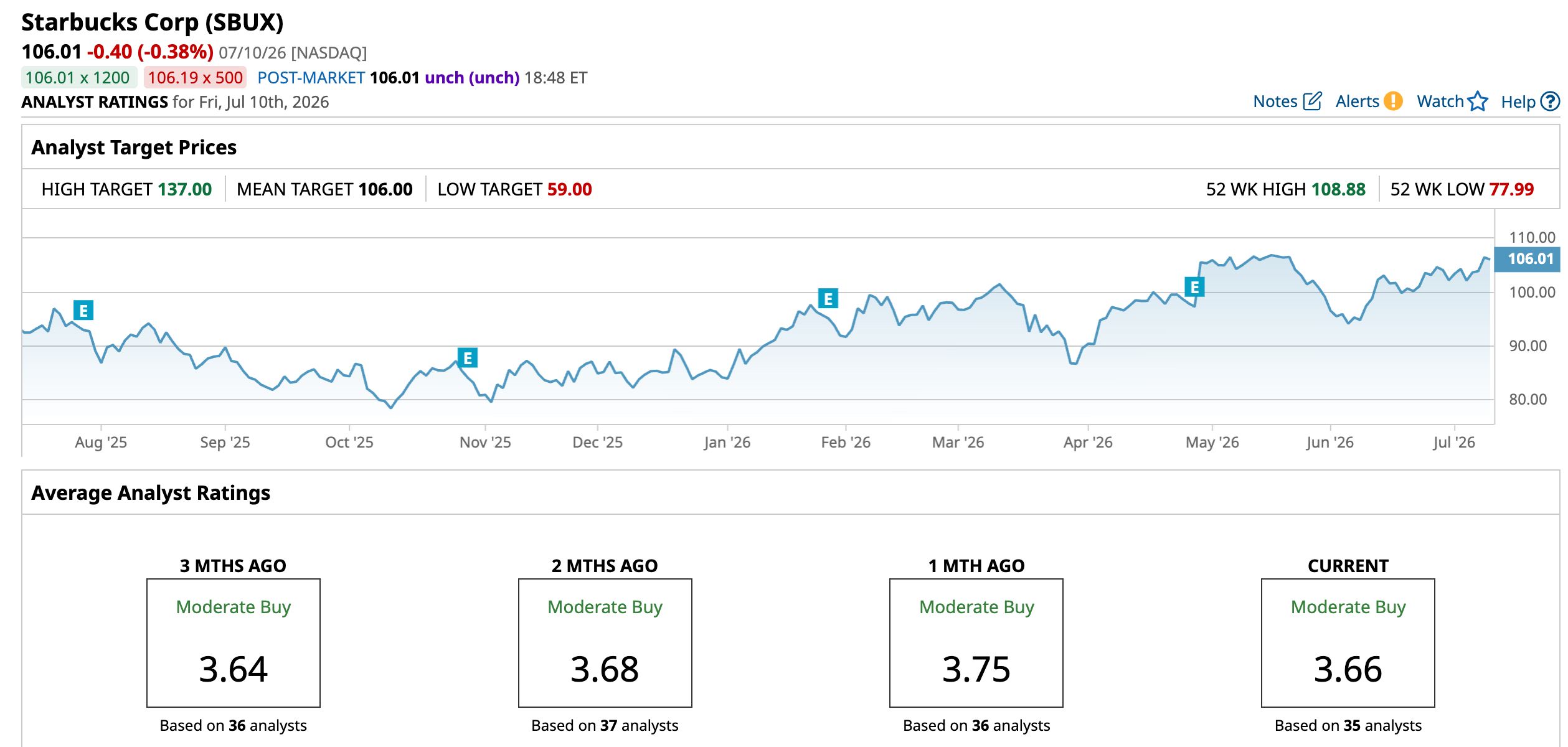

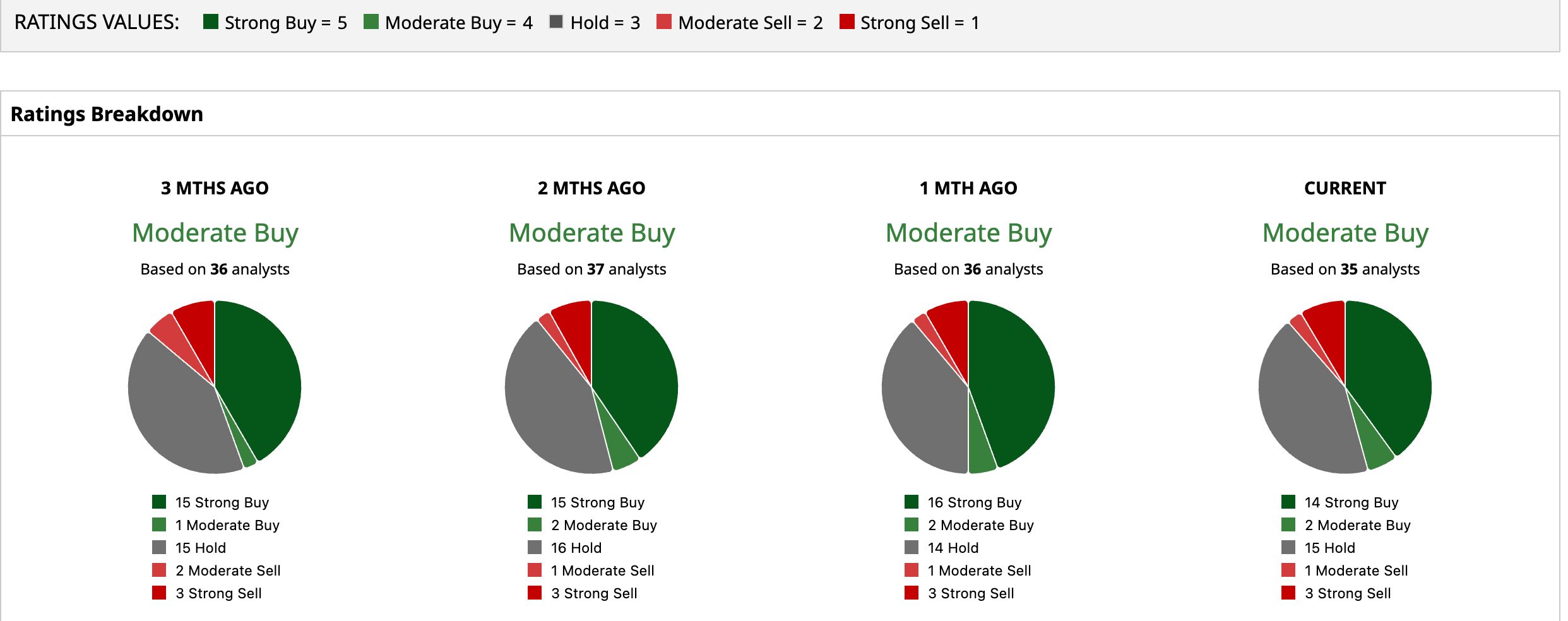

Starbucks has been a popular name on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating. Of the 35 analysts rating the stock, 14 analysts have rated it a “Strong Buy,” two analysts suggest a “Moderate Buy,” while 15 analysts are playing it safe with a “Hold” rating, one analyst suggested a “Moderate Sell,” and three analysts gave a “Strong Sell” rating. The consensus price target of $106 is roughly flat compared to current levels. However, the Street-high price target of $137 indicates a 29.2% upside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Navitas Semiconductor Stock Is on the Ropes. It Faces a New Patent Infringement Lawsuit. Grok’s Ongoing Market Share Decline Raises Questions About SpaceX’s AI Strategy Post-IPO Starbucks Is Serving Up Your Coffee with a Side of AI. What That Means for SBUX Stock. Nvidia Stock Has Been Flat, But NVDA Price Targets are Higher - Shorting Puts Works