As expected, the US president upped his War on Iran over the weekend with headlines telling us of increased fighting over the Strait of Hormuz.

The continued rally in the price of Energies has seen the Fed fund forward curve shift, now indicating a possible rate hike at the conclusion of the September 2026 meeting.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

Meanwhile, US weather was hot and dry over the weekend, sparking a rally in the Grains sector overnight.

Morning Summary: At Sunday night’s open, it looked like US markets were in for just another Manic Monday. As expected, weekend headlines were filled with talk of escalating fighting over the Strait of Hormuz and the US president again saying he was going to “annihilate” the country of Iran, this time if they tried to kill him. WTI crude oil (CLQ26) initially jumped as much as $3.67 (5.1%) with Brent crude adding as much as $3.78 (5.0%). Distillates (HOQ26) gained as much as 13.9 cents (3.9%) while RBOB gasoline added as much as 10.6 cents (3.6%). Are skyrocketing fuel prices an economic cause for concern long-term? Let me answer the question this way: The Fed fund futures forward curve is showing rate hikes are now possible at the conclusion of the September 2026 meeting (September 16), and possibly the January 2027 meeting (January 27) or March 2027 meeting (March 17). Given this, the US dollar ($DXY) would be expected to extend its long-term uptrend against global currencies while US stock indexes could come under increased pressure. As for short-term, given the overnight rally in Energies and selloff in Indices (US stock index futures), I’m expecting the US president to announce another non-existent “deal” with Iran at some point today.

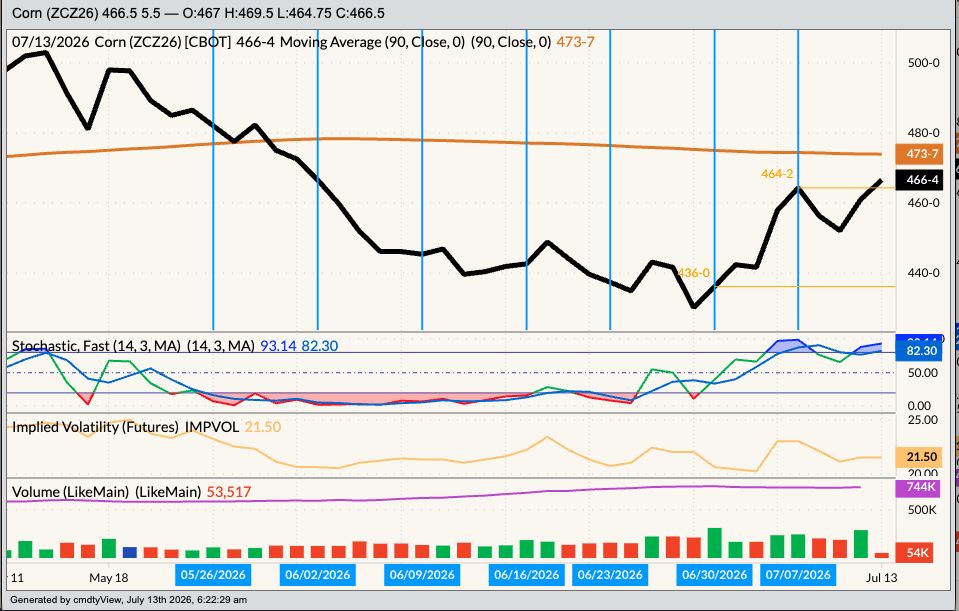

Corn: The Grains sector also jumped at Sunday night’s open on what looked to be solid buying tied to weather. The September corn contract (ZCU26) added as much as 8.0 cents overnight on trade volume of nearly 30,000 contracts and was holding onto a gain of 4.75 cents at this writing. Meanwhile, December (ZCZ26) gained as much as 8.5 cents on trade volume of 53,000 contracts and was sitting 5.5 cents in the green pre-dawn. The US Plains and Midwest were generally hot and dry over the weekend, giving early trade the feel of a long-awaited weather market in the Grains sector. Could it build into something like what we’ve seen in Softs, where coffee and cocoa have exploded on adverse weather conditions in Brazil and West Africa respectively? Fundamentally, King Corn isn’t there yet given it’s forward curve continues to show a carry (contango for those of you in New York). However, last Friday’s Commitments of Traders report (legacy, futures only) showed funds added to their net-long futures position by 36,800 contracts as of Tuesday, July 7. Since then, the September issue is up only 0.75 cent while December is up 2.0 cents. Technically, the contract’s 90-day moving average is hanging over the head of the more-heavily traded December issue.

Soybeans: As one would expect given the combined efforts of the US president and US weather, the oilseed sub-sector was solidly in the green overnight through early Monday morning. The August soybean oil contract rallied as much as 1.2 cents (1.7%)[i] while the more heavily traded December issue (ZLZ26) also gained as much as 1.2 cents (1.7%). As for soybeans, the first Jar Jar Binks Contract[ii] (August) added as much as 17.0 cents on trade volume of about 7,700 contracts and was sitting 10.0 cents higher at this writing. The more heavily traded November issue (ZSX26) gained as much as 16.5 cents while registering 38,000 contracts changing hands and was up 8.0 cents to start the day. A look back at Friday’s session and we see August closed 14.0 cents higher while November was 9.25 cents in the green. When the calculating was done, the National Soybean Index came in with a gain of about 13.5 cents meaning basis weakened slightly versus August and strengthened against November. The bottom line for the basis market is it remains neutral compared to previous 5-year and 10-year weekly closes. The Commitments of Traders report showed Watson added 36,180 contracts to its net-long futures position as of Tuesday, July 7.

Wheat: The wheat sub-sector also started the week with a rally, though winter markets struggled to hold gains as the overnight session wore on. The September HRW issue (KEU26) added as much as 14.75 cents on trade volume of 6,200 contracts before running out of momentum. Through early Monday morning September had lost as much as 4.0 cents and was sitting 2.0 cents in the red at this writing. While it’s possible there was some harvest pressure that emerged overnight, through the magic of open orders, it has been my experience few commercial interests use that avenue. Given this, the more likely reason for the break was a round of selling from the noncommercial side. Over in SRW we see the September issue (ZWU26) down 1.5 cents after rallying as much as 12.75 cents and losing as much as 4.0 cents on trade volume of 20,000 contracts. All the talk of weather problems in Europe has been interesting to follow, though USDA did not increase its US wheat export guess in its latest release of KENO numbers (the July WASDE report). Not only that, but 2026-27 export demand is expected to be down 133 mb from the 2025-26 estimate of 908 mb.

[i] I’ve been asked why I add percent changes. This way we can compare the moves made by related markets not based on the same quantity. For example, distillates (diesel fuel) is priced in dollars and cents per barrel where soybean oil is priced in cents per pound.

[ii] Something created for comic relief but ultimately viewed as annoying.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Did the Commodity Complex Remind Me of the Bangles to Start the Week? Stocks Set to Open Lower as SK Hynix Sparks Chip Selloff, U.S. Inflation Data and Big Bank Earnings Awaited Huge Earnings, Inflation Data and Other Key Things to Watch this Week ‘Shark Tank’ Star Kevin O’Leary ‘Can’t Stand It’ When Young People Spend $28 on Lunch But Only Make $70k — ‘I Mean, That’s Just Stupid’