Alphabet (GOOG) (GOOGL), the parent company of Google, is all set to report its second quarter results on July 22. Investors have plenty of reasons to be optimistic heading into earnings after Alphabet raised the bar with a strong first quarter. Here’s why bulls are optimistic ahead of Alphabet’s Q2 print.

www.barchart.com

www.barchart.com A Strong First Quarter Raised the Bar

Alphabet’s strong first quarter has raised the bar for the rest of 2026. With total revenue up 22% year-over-year (YoY) to $109.9 billion, marking the company’s 11th consecutive quarter of double-digit revenue growth.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

When the AI boom began, investors questioned whether generative AI would disrupt Google's search business. But Google integrated AI into search, which has resulted in increased engagement. Search and Other revenue climbed 19% YoY in Q1, reaching $60.4 billion, accounting for 55% of total company revenue, which increased 22% to $109.9 billion. According to CEO Sundar Pichai, search queries climbed to their highest level ever. Plus, AI-powered experiences such as AI Overviews and AI Mode continue to drive user engagement.

Alphabet’s advertising business is also benefitting from these AI improvements. The company said more than 30% of Search advertising spend now flows through AI-powered campaigns such as AI Max and Performance Max. Notably, advertising revenue increased by 15.5% to $77.2 billion.

Google Cloud and AI Could Be the Biggest Earnings Catalyst

While Search accounts for the bulk of Alphabet’s total revenue, Google Cloud has also become its fastest-growing business. Cloud revenue surged 63% YoY to $20 billion. Demand for Alphabet's generative AI offerings continued to accelerate, with revenue from these products rising nearly 800% YoY and making Enterprise AI the top growth driver within Google Cloud. The segment’s operating income nearly tripled to $6.6 billion in the quarter.

Importantly, Google Cloud’s backlog stood at $462 billion, led by strong enterprise demand and the inclusion of Tensor Processing Unit (TPU) hardware agreements. Alphabet unveiled its eighth-generation TPUs, introducing separate chips optimized for AI model training and inference workloads. These TPUs deliver three times the processing power and twice the performance of Ironwood. Alphabet continues to strengthen its AI infrastructure by becoming one of the first cloud providers to offer Nvidia's (NVDA) upcoming Vera Rubin NVL72 platform alongside its existing Blackwell- and Hopper-based systems.

Compared to last year, the company has signed double the number of deals worth between $100 million and $1 billion. Additionally, it has signed multiple contracts exceeding $1 billion. According to management, more than half of the current backlog is expected to translate into revenue over the next 24 months.

Can Alphabet Sustain Its AI Momentum? Here's What Investors Should Watch

The majority of investors' concerns this year have been that hefty capital investment has not been justified by earnings growth. Alphabet continues to increase spending aggressively to support AI demand. Despite the company’s AI investments, its bottom line also improved dramatically. Adjusted earnings per share jumped 82% to $5.11 in the quarter. The company also generated $10.1 billion in free cash flow and ended the quarter with $126.8 billion in cash and marketable securities against $77.5 billion in long-term debt. Alphabet also increased its quarterly dividend by 5%, reinforcing management's confidence in future cash generation. Investors will now most likely focus less on what has happened in Q1 and more on whether management can sustain this pace throughout the remainder of 2026.

Capital expenditures totaled $35.7 billion during Q1. Around 60% of infrastructure spending went toward servers, while the remaining 40% funded data centers and networking equipment. Management now expects capital expenditures of $180 billion and $190 billion in 2026, with much higher investment in 2027 as it expands its AI infrastructure footprint. This rise in expenses will most likely put pressure on profitability.

Furthermore, investors will also be looking for updates on Alphabet's expanding hardware business. The company now plans to begin delivering TPU hardware directly to select customers' own data centers, creating a new revenue opportunity beyond traditional cloud services. While management expects only a small portion of it to be recognized as revenue later in 2026, the vast majority of this revenue is expected in 2027.

Analysts expect second quarter revenue to increase by 21% YoY to $116.8 billion, while adjusted earnings could rise by 25.5% to $2.31 per share. For the full year, analysts forecast an earnings increase of 31.6%, with earnings growth dipping to 2.4% in fiscal 2027.

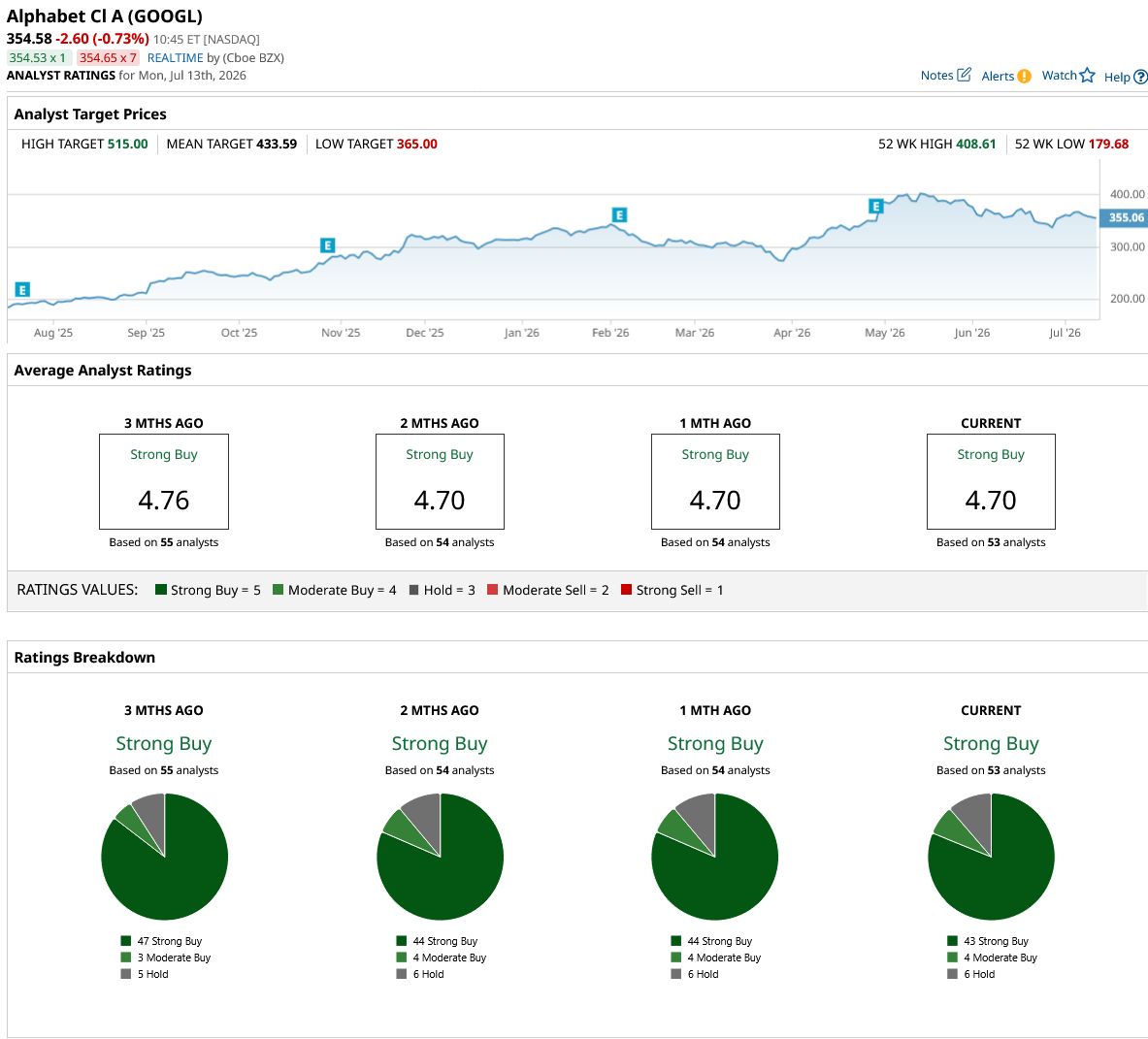

What Analysts Are Saying About GOOG Stock

Overall, on Wall Street, GOOG stock is a consensus “Strong Buy.” Of the 53 analysts covering the stock, 43 rate it a “Strong Buy,” four say it is a “Moderate Buy,” and six rate it a “Hold.” GOOG stock has surged 13% year-to-date (YTD), surpassing the overall market gain. Analysts forecast the stock can rise by 22% from current levels based on its average target price of $433.59. Plus, its high price estimate of $515 suggests the stock has an upside potential of 45% over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why Delta Air Lines Could Be a Top Stock to Buy for the Rest of 2026 Why Analysts Are Betting Western Digital Stock Can Gain Another 30% from Here COIN Stock Alert: 3 Reasons Why Coinbase Shares Are In Focus A New Report Says Meta Platforms Could Overtake Google AI. How to Play META Stock Here.