Regional banking institutions continue to operate within an environment influenced by interest rate volatility, regulatory requirements and evolving customer needs. Within this backdrop, Peoples Bancorp of North Carolina, Inc. PEBK and HomeTrust Bancshares, Inc. HTB represent two North Carolina-based bank holding companies with distinct operating models and market presence. PEBK conducts its banking operations through Peoples Bank, offering a range of commercial and consumer banking services, lending and deposit products while primarily serving customers within North Carolina. In contrast, HTB operates through HomeTrust Bank, providing a broader portfolio of banking products and financial services across a larger regional footprint in the Southeastern United States.

HomeTrust's platform reflects a more diversified and growth-oriented strategy, supported by a wider geographic presence and a broader customer base. This enables the company to capitalize on opportunities across multiple regional markets. Peoples Bancorp, by comparison, maintains a more concentrated community banking model, emphasizing relationship-based banking and serving customers within its established local markets.

While both institutions operate within the regional banking space, differences in scale, geographic diversification and operating focus — PEBK's localized, community-centric approach versus HTB's broader regional banking platform — result in distinct strategic positioning and competitive dynamics. This leads to a key consideration: which institution is better positioned to navigate the evolving banking landscape and deliver sustained shareholder value? Let’s take a closer look.

Stock Performance & Valuation: PEBK vs. HTB

PEBK (up 13.8%) has underperformed HTB (up 15.4%) over the past three months. However, in the past year, Peoples Bancorp has rallied 50.2% compared with HomeTrust's gain of 30.3%.

Image Source: Zacks Investment Research

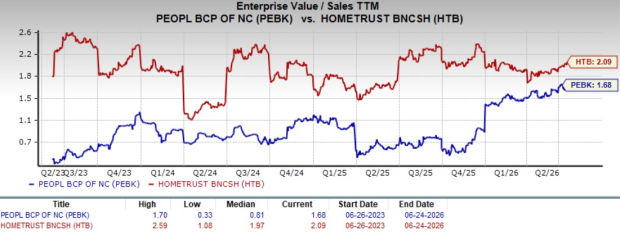

Meanwhile, PEBK is trading at a trailing 12-month enterprise value-to-sales (EV/S) ratio of 1.7X, above its median of 0.8X over the past three years. HTB’s trailing 12-month EV/S multiple sits at 2.1X, above its last three-year median of 1.9X. PEBK and HTB both appear to be expensive when compared with the Zacks Finance sector’s average of 1.4X.

Image Source: Zacks Investment Research

Factors Driving Peoples Bancorp Stock

Peoples Bancorp is benefiting from steady balance sheet expansion and an improving funding mix. Loan and deposit balances continued to grow during the first quarter of 2026, while core deposits increased as a share of total deposits. This stronger base of low-cost funding, combined with lower funding costs, supported higher net interest income and margin expansion, contributing to stable earnings growth despite a modest rise in credit provisioning.

The company's disciplined lending strategy and prudent credit risk management remain key strengths. Peoples Bancorp maintains a diversified loan portfolio with no significant concentration in any single industry and follows rigorous underwriting standards supported by regular portfolio reviews and stress testing. While the allowance for credit losses increased in line with loan growth, asset quality remained healthy, reflecting PEBK 's conservative approach to managing credit risk.

Peoples Bancorp's solid capital position enhances its financial resilience and supports long-term shareholder returns. The bank remains well capitalized, comfortably exceeding regulatory capital requirements, providing the flexibility to withstand economic uncertainties while maintaining a stable operating profile. Further, PEBK continued to increase its quarterly cash dividend, reflecting management's commitment to returning capital to shareholders and confidence in its long-term financial strength.

Factors Driving HomeTrust Stock

HomeTrust continues to benefit from improving profitability, driven by a favorable funding mix and disciplined balance sheet management. Lower funding costs and changes in deposit mix supported net interest margin expansion during the first quarter of 2026, helping lift net interest income despite modest pressure on asset yields. Reduced credit loss provisions further supported earnings, highlighting HTB’s ability to navigate a changing interest rate environment.

The company's diversified business model and expansion strategy provide a strong platform for long-term growth. HomeTrust has expanded its presence across high-growth markets in the Southeast through acquisitions, new banking offices and commercial lending initiatives. Its broad lending portfolio, spanning commercial, residential and specialized financing businesses, enables HTB to serve a diverse customer base while reducing reliance on any single lending segment.

HomeTrust's conservative risk management and solid capital position further strengthen its investment appeal. The bank follows disciplined credit approval processes, maintains a high-quality investment portfolio and remains well capitalized above regulatory requirements, providing the financial flexibility to pursue growth opportunities while remaining resilient during periods of economic uncertainty. Its continued dividend increases and active share repurchases also demonstrate management's commitment to enhancing long-term shareholder value.

Choose PEBK Over HTB Now

Both Peoples Bancorp and HomeTrust possess solid fundamentals, but they appeal to investors with different investment preferences. PEBK offers a relatively straightforward community banking model supported by steady loan and deposit growth, prudent credit management and a strong capital position. Its focus on relationship banking and disciplined execution has translated into consistent operating performance, making its earnings profile more predictable.

HomeTrust, meanwhile, presents a more diversified growth story. Its broader geographic footprint, wider lending platform and expansion across high-growth markets provide greater long-term growth opportunities. However, its larger and more diversified franchise also requires continued execution across multiple business lines, making its operating story comparatively more complex.

From a valuation perspective, both stocks appear to trade at premium valuations relative to the broader Finance sector, reflecting investor confidence in their underlying fundamentals. Despite this, PEBK appears to offer relatively better value, suggesting its current valuation is more aligned with its consistent operating performance and stable growth profile. HTB, on the other hand, appears to reflect relatively higher investor expectations, leaving less room for upside while making sustained execution critical to justify its premium valuation.

Given its combination of consistent fundamentals, simpler business model and relatively more reasonable valuation, Peoples Bancorp appears to be the better regional bank stock to buy right now. While neither stock looks inexpensive at current levels, PEBK offers a more balanced risk-reward profile, making it a relatively more attractive choice for investors seeking steady long-term returns.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Peoples Bancorp of North Carolina, Inc. (PEBK): Free Stock Analysis Report

HomeTrust Bancshares, Inc. (HTB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).