Chipotle Mexican Grill, Inc. CMG and CAVA Group, Inc. CAVA remain two key contenders in fast casual, but their operating profiles are distinctly different. Chipotle is a scaled category leader, supported by broad brand awareness, strong restaurant economics, digital depth, a debt-free balance sheet and a sizable long-term restaurant runway. CAVA, meanwhile, is still in an earlier phase of national expansion, supported by traffic-led momentum and a differentiated position as the leader in Mediterranean fast casual.

For investors, the debate comes down to a clear question: Is Chipotle’s scale and proven operating model more compelling, or does CAVA’s faster growth and category momentum offer the stronger edge? Let’s analyze.

The Case for CMG Stock

Chipotle remains one of the most established operators in fast casual, with a large domestic footprint and a long-term goal of reaching 7,000 restaurants in North America. The company also continues to pursue international growth, including partner-operated openings in Mexico and South Korea, while Singapore is likely to open in 2027. Europe remains a longer-term opportunity, supported by positive comps across countries and continued restaurant development. In the Middle East, geopolitical conditions may delay some partner-operated openings, although CMG’s long-term view of the region remains intact.

The company’s Recipe for Growth strategy is focused on strengthening the core business, improving execution, expanding digital capabilities, accelerating menu innovation, developing talent and broadening global access. A key part of that strategy is operational improvement. Chipotle is rolling out high-efficiency equipment, including dual-sided planchas, three-pan rice cookers and high-capacity fryers, to improve prep, throughput and culinary consistency. The equipment is already in more than 600 restaurants, with a target of 2,000 by year-end, and the company is seeing benefits translate into hundreds of basis points of comp-sales improvement in markets where it has been deployed.

Technology and loyalty are also important elements of Chipotle’s growth case. Chipotle Kitchen, its digital make-line display, is designed to improve accuracy, speed and consistency, and the company expects to roll it out across all restaurants by year-end. Ava Cado, its AI assistant, is being expanded from hiring support into operational insights, scheduling, prep planning and cook-to-needs guidance. Rewards also remain a major opportunity, as only about 20% of in-restaurant transactions are linked to the program compared with nearly 90% of app transactions. Recent in-restaurant enrollment efforts have already lifted daily enrollees by nearly 25%.

Menu innovation is helping Chipotle defend traffic and frequency. The high-protein lineup — Chicken Al Pastor and Cilantro Lime Sauce — supported incremental transactions, while Chipotle Honey Chicken adds another limited-time offering to sustain engagement. Add-on protein reached nearly one-fourth of all transactions and remained elevated, reinforcing Chipotle’s protein-led positioning. Group occasions also remain underpenetrated, with catering and Build Your Own Chipotle representing more than 2% of combined sales, while the company sees potential for these occasions to become a double-digit sales mix over time.

However, Chipotle’s near-term setup is more measured. The company maintained a comparable sales outlook of about flat, reflecting a cautious view of the consumer environment. Profitability remains pressured by cost inflation in items such as beef and freight, along with wage pressure, benefits expense, marketing, utilities and delivery costs.

The Case for CAVA Stock

CAVA offers a faster-growth investment profile, supported by strong traffic trends, expanding brand awareness and a differentiated Mediterranean platform. The company’s latest results showed continued momentum, with same-restaurant sales growth driven by positive traffic. CAVA has maintained a measured value stance, taking a modest January price increase while keeping base bowl and pita pricing flat.

Restaurant expansion remains the central driver of CAVA’s long-term story. The company ended the first quarter with 459 restaurants across 29 states and the District of Columbia, while new restaurant productivity remained above 100% and systemwide average unit volumes reached $3 million. Recent entries into Cincinnati, St. Louis and Columbus, along with a planned entry into Minneapolis, highlight CAVA’s opportunity to expand into new geographies while building density in existing markets.

CAVA is also using menu innovation to deepen guest engagement. The return of roasted white sweet potato resonated with guests, while Pomegranate-Glazed Salmon marked the company’s first seafood offering. Salmon broadens the protein platform and fits naturally within the Mediterranean positioning of the brand. Although the item is expected to pressure the margin rate, it is priced to be penny-profit neutral, supporting profit-dollar contribution while expanding guest choice.

Operational infrastructure is becoming increasingly important as CAVA scales. CavaCore, the company’s modern data platform, and CAVA Current, its real-time commerce platform, are designed to improve visibility, order processing, personalization and demand planning across restaurants. CAVA is also investing in talent development through its Flavor Your Future platform and Assistant General Manager rollout. Restaurants with AGM coverage are outperforming those without, supporting the company’s focus on maintaining execution quality as it expands.

CAVA has raised its full-year 2026 outlook. The company now expects 75-77 net new restaurant openings, compared with prior guidance of 74-76. Same Restaurant Sales growth is expected to be in the range of 4.5%-6.5%, up from the prior projection of 3%-5%. Adjusted EBITDA is now expected to be $181-$191 million, up from $176-$184 million. The company also noted that second-quarter trends are tracking in line with the first quarter and above the revised full-year range, while still embedding moderation later in the year. This framing supports a forward view that balances current momentum with a more cautious macro backdrop.

However, CAVA’s faster growth comes with execution and cost risks. The outlook includes a 20-40-basis-point headwind tied to elevated energy costs and an approximately 100-basis-point restaurant margin-rate drag from the national salmon rollout. Labor investments, higher preopening costs and third-party delivery mix are also factors to watch.

How Does the Zacks Consensus Estimate Compare for CMG & CAVA?

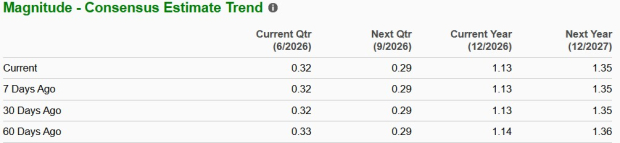

The Zacks Consensus Estimate for Chipotle’s 2026 sales indicates a rise of 8.4% year over year, while earnings per share (EPS) suggest a decline of 3.4% from the prior-year figure. In the past 60 days, earnings estimates for 2026 have declined 0.9%.

CMG Earnings Estimate Trend

Image Source: Zacks Investment Research

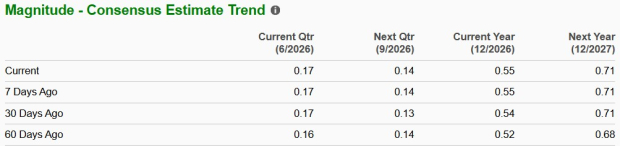

The Zacks Consensus Estimate for CAVA’s 2026 sales and EPS suggests year-over-year increases of 26.2% and 1.9%, respectively. In the past 60 days, earnings estimates for 2026 have increased 5.8%.

CAVA Earnings Estimate Trend

Image Source: Zacks Investment Research

Price Performance & Valuation of CMG & CAVA

CMG stock has declined 10.9% in the past six months against the industry's growth of 0.5%. Meanwhile, CAVA shares have gained 39.5% in the same time frame.

CMG & CAVA Stock Six-Month Price Performance

Image Source: Zacks Investment Research

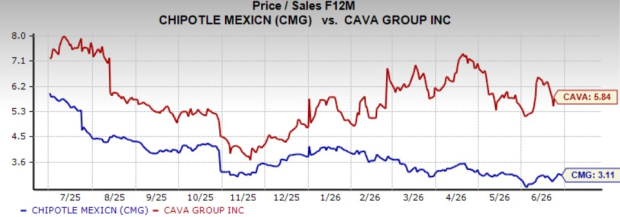

Chipotle is trading at a forward 12-month price-to-sales (P/S) multiple of 3.11, below the industry average of 3.31 over the last year. CAVA's forward 12-month P/S multiple sits at 5.84 over the same time frame.

Image Source: Zacks Investment Research

Our Take

Chipotle and CAVA offer contrasting investment profiles in the fast-casual space. Chipotle remains the more established operator, supported by scale, brand recognition, digital engagement, restaurant technology and a sizable long-term unit-growth runway. However, its near-term setup is more restrained, with flat comparable sales guidance, cost pressures and downward earnings estimate revisions.

CAVA, in contrast, offers the faster-growth profile, supported by traffic-led same-restaurant sales growth, strong new-restaurant productivity and an improved 2026 outlook. Its measured value stance, menu innovation and expanding national footprint strengthen the operating story. This is also reflected in its estimate revision trend and relative stock performance.

Although CAVA trades at a premium valuation and faces salmon-related margin pressure, its stronger growth trajectory gives it the better edge in this faceoff. With both stocks carrying a Zacks Rank #3 (Hold) at present, CAVA appears better positioned from an operating-momentum standpoint, while Chipotle remains a high-quality long-term compounder with a more measured near-term profile. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chipotle Mexican Grill, Inc. (CMG): Free Stock Analysis Report

CAVA Group, Inc. (CAVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).