The central question for investors is not whether FIGS, Inc. FIGS is improving. It is whether the stock already reflects too much of that improvement.

A strong revenue quarter, a raised sales outlook, and expanding customer metrics support the bullish case. A richer earnings multiple and visible cost pressure make the answer less straightforward.

FIGS Bulls Can Point to Better Guidance

FIGS raised its fiscal 2026 revenue growth outlook to 14%-16%, up from its prior view of 10%-12%. That followed first-quarter fiscal 2026 revenues of $159.9 million, up 28% year over year.

Active customers surpassed 3 million for the first time, while average order value rose 4.2% to $124. Those metrics point to customer acquisition and better spending per order.

The niche remains attractive because healthcare apparel is replenishment-driven and tied to a resilient workforce. Investors comparing FIGS with brand-led apparel names such as NIKE, Inc. NKE and lululemon athletica inc. LULU may focus on whether brand strength can support repeat demand without sacrificing profitability.

FIGS also has flexibility. The company ended the quarter with $277 million in cash, cash equivalents and short-term investments, remained debt-free, and repurchased $8.8 million of shares.

FIGS, Inc. Price, Consensus and EPS Surprise

FIGS, Inc. price-consensus-eps-surprise-chart | FIGS, Inc. Quote

FIGS Bears Will Focus on Margin Pressure

The cautious case starts with gross margin. FIGS reported a 67.7% gross margin in the first quarter, up only 10 basis points year over year despite the revenue gain.

Tariffs, inbound freight pressure from higher oil prices and a pause in the duty drawback program remain headwinds. Management expects gross margin to decline modestly year over year in the second quarter and more meaningfully in the third quarter before improving in the fourth quarter.

Marketing also limits operating leverage. Marketing expense rose to $29.5 million in the first quarter, or 18.4% of revenues, compared with 14.5% a year earlier.

That spending supported brand campaigns and partnerships, but earnings may not scale as quickly as revenues if sales growth slows from the first-quarter pace.

FIGS Valuation Leaves Less Room for Error

Valuation is the biggest constraint on a clean buy case. FIGS trades at 39.96X forward 12-month earnings per share.

That multiple is above 15.11X for the Zacks sub-industry, 22.53X for the broader Zacks sector, and 20.9X for the S&P 500. A premium can be justified when growth is durable, but it leaves little room for weaker margins or a sharper second-half slowdown.

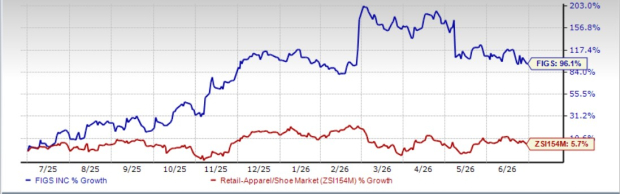

The stock is up 96.1% over the past year, even after declining 25% over the past three months. That rally raises the hurdle for new buyers.

At this level, investors need confidence that product innovation, international expansion, Community Hubs and TEAMS can keep revenue growth broad-based.

Image Source: Zacks Investment Research

FIGS Cash Flow Adds a Note of Caution

Cash flow complicates the growth story. Operating cash flow was an outflow of $3.2 million in the first quarter, compared with positive operating cash flow of $9.2 million a year earlier.

Working capital was the main drag. Inventory build supported spring color drops, the Nurses Week cadence and international scaling.

That does not invalidate the growth strategy. It does mean investors should watch whether FIGS converts higher sales into cash more efficiently.

Management expects working capital consumption to ease, helped by faster replenishment cycles, tighter buys and supplier lead-time gains. Until that shows up consistently, cash conversion remains a useful check on the valuation.

FIGS Ratings Back a Wait-and-See Stance

The bottom line is that FIGS looks fundamentally better, but not clearly cheap. Revenue momentum, customer gains and a debt-free balance sheet support interest, while cost pressure, negative operating cash flow and a premium multiple argue for patience.

The stock currently carries a Zacks Rank #3 (Hold). That fits a balanced setup in which the business is improving, but the near-term risk-reward is not one-sided. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Style Scores are mixed. FIGS has a Momentum Score of A, but also a Value Score of D, Growth Score of C and VGM Score of D.

Style Scores complement the Zacks Rank, with stronger grades generally more favorable. For FIGS, the Momentum Score supports keeping the stock on watch, while the weak Value and VGM Scores reinforce a wait-and-see stance at today’s valuation.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

FIGS, Inc. (FIGS): Free Stock Analysis Report

NIKE, Inc. (NKE): Free Stock Analysis Report

lululemon athletica inc. (LULU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).