Over the past year, SandRidge Energy, Inc. SD has gained 24.2%, significantly outperforming peers Matador Resources MTDR and Range Resources RRC, which have declined 0.9% and 9.7%, respectively. The stock has also comfortably outpaced the sub-industry's 1.4% return during the same period.

SandRidge has steadily strengthened its business through disciplined capital allocation, operational execution and production growth. As the company continues to improve drilling economics while maintaining a strong balance sheet, investors are assessing whether its attractive valuation leaves room for additional upside.

Improving Capital Efficiency Through Cherokee Development

SandRidge continues to enhance the economics of its drilling program through operational improvements in the Cherokee Play. During the first quarter of 2026, the company drilled two wells and completed three wells under its ongoing one-rig development program. Notably, management stated that the third well drilled during 2026 recorded the lowest drilling costs since the program began, reflecting continued progress in execution and cost management.

According to management, these gains stem from disciplined planning, competitive bidding for drilling and completion services, and ongoing optimization of field operations. The company has also proactively secured critical drilling equipment and services, helping reduce exposure to inflationary pressures and supply-chain disruptions that could otherwise increase capital costs.

Operational improvements have translated into lower lease operating expenses, both in absolute terms and on a per-unit basis, supported by efficient operations and higher production volumes from the Cherokee development program. SandRidge plans to drill 10 operated Cherokee wells and complete eight wells in 2026, with the remaining completions scheduled for next year. The company also continues selective leasing activities to consolidate acreage and expand its drilling inventory.

These initiatives demonstrate that SandRidge is not only increasing production but also improving capital productivity by lowering drilling costs, maintaining disciplined operating expenses and expanding its long-term development opportunities. Such improvements strengthen project economics and position the company to generate attractive returns across varying commodity price environments.

Favorable Natural Gas Fundamentals Support Long-Term Growth

The broader industry outlook remains constructive for SandRidge, particularly given its significant exposure to natural gas. According to the U.S. Energy Information Administration (EIA), U.S. natural gas consumption in the electric power sector is projected to increase from 36.5 billion cubic feet per day (Bcf/d) in 2025 to 38.5 Bcf/d in 2026 and 39.8 Bcf/d in 2027, supported by rising electricity demand, expanding gas-fired generating capacity and competitive natural gas prices.

The EIA also expects U.S. LNG exports to rise from 15.3 Bcf/d in 2025 to 16.3 Bcf/d in 2026 before reaching 17.7 Bcf/d in 2027, reflecting continued expansion in export capacity. Since natural gas accounts for roughly 50% of SandRidge's production mix, these structural demand drivers could provide a supportive pricing environment for a substantial portion of the company's production.

On the oil side, the EIA projects U.S. crude oil production to increase from 13.4 million barrels per day (mb/d) in 2025 to 13.5 mb/d in 2026 and 13.7 mb/d in 2027. However, global supply is expected to outpace demand growth, resulting in higher inventories and softer prices. Brent crude is forecast to average $69 per barrel in the second half of 2026 before declining to $58 per barrel in 2027.

Although lower oil prices could weigh on industry profitability, SandRidge appears relatively well-positioned because of its debt-free balance sheet, disciplined capital allocation and ongoing efforts to improve drilling efficiencies and reduce operating costs. These strengths should help the company navigate commodity price volatility while benefiting from favorable long-term natural gas demand trends.

Strong Financial Position Provides Strategic Flexibility

SandRidge maintains a solid financial foundation that supports growth initiatives and shareholder returns. The company ended the first quarter of 2026 with more than $104 million in cash and cash equivalents while remaining debt-free, giving it considerable flexibility to fund development projects internally, pursue acquisitions and withstand commodity price fluctuations without relying on external financing.

Management has also demonstrated a balanced capital allocation strategy. The board increased the regular quarterly dividend 8% and declared an additional one-time special dividend, reflecting confidence in the company's financial outlook. The company’s dividend yield of 3.87% is higher than the industry’s average of 2.28%. Meanwhile, SandRidge retains meaningful authorization for opportunistic share repurchases, allowing it to return excess capital to shareholders while preserving flexibility for future investments.

This combination of financial strength, shareholder-friendly capital allocation and disciplined investment supports the company's long-term growth strategy.

Valuation Snapshot

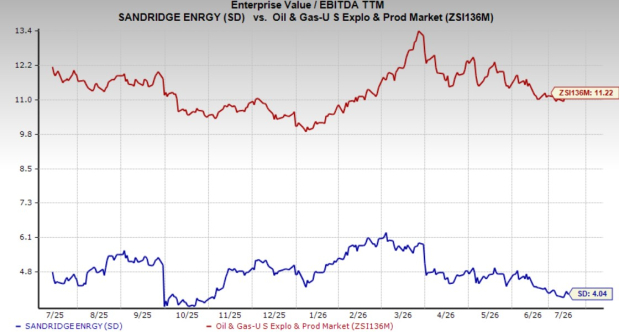

Despite its strong share-price performance, SandRidge appears attractively valued relative to the broader industry. The stock currently trades at a trailing 12-month enterprise value-to-EBITDA (EV/EBITDA) multiple of 4.04X, well below the industry average of 11.22X.

Among peers, Matador Resources trades at 4.47X, whereas Range Resources trades at 5.87X on the same basis. SandRidge's lower valuation suggests that the market may not be fully pricing in its improving operational performance, disciplined capital allocation and strong financial position.

Should You Buy SD Stock?

SandRidge continues to strengthen its business through improving drilling efficiencies in the Cherokee Play, disciplined cost management and a debt-free balance sheet. The company's growing operational efficiency, healthy cash position and shareholder-friendly capital allocation strategy provide a solid foundation for long-term value creation. Additionally, favorable long-term natural gas demand trends could serve as a meaningful tailwind, given that natural gas represents roughly half of its production.

With shares trading at an EV/EBITDA multiple of just 4.04X, well below the industry average, the stock appears attractively valued despite its recent outperformance. While commodity price volatility remains a significant risk, SandRidge's financial strength and operational discipline position it well to manage market cycles.

Given its improving fundamentals and inexpensive valuation, investors looking for exposure to the energy sector may consider buying SandRidge stock for long-term appreciation.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Range Resources Corporation (RRC): Free Stock Analysis Report

SandRidge Energy, Inc. (SD): Free Stock Analysis Report

Matador Resources Company (MTDR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).