HubSpot, Inc. HUBS and International Business Machines Corporation IBM provide AI-powered software solutions for business enterprises. HubSpot specializes in AI-enabled CRM, marketing, sales and customer service software. The integration of Clearbit, a B2B data provider for marketing intelligence, has facilitated the development of more powerful, advanced and accurate AI capabilities. The adoption of advanced AI tools, such as AI assistance, AI agents, AI insights and ChatSpot, across its entire product suites and customer platform is driving more value to customers.

IBM offers cloud and data solutions that aid enterprises in digital transformation. In addition to hybrid cloud and AI services, the company provides advanced information technology solutions, computer systems, quantum computing and supercomputing solutions, enterprise software, storage systems and microelectronics.

Let us delve a little deeper into the companies’ competitive dynamics to understand which of the two is relatively better placed in the industry.

The Case for HubSpot

HubSpot's AI, which includes cutting-edge features such as AI assistance, AI agents, AI insights, and ChatSpot, is driving more value to customers. HubSpot has integrated HubSpot AI across its entire product suites and customer platform, enabling users to leverage AI features at no additional cost. Pricing optimization and the transition to a seat pricing model are expected to drive customer growth. The seat pricing model lowers the barrier for customers to get started with HubSpot and mitigates pricing friction for upgrades. The model intends to encourage more clients to adopt HubSpot services and expand their usage over time. It is anticipated to lead to healthier customer cohorts and is expected to contribute to the company's growth over time.

The company is embedding generative AI into its CRM, marketing and sales automation tools. The buyout of Frame AI, an AI-powered conversation intelligence platform, has enabled HUBS to unify structured and unstructured data to transform conversations into actionable intelligence. The One HubSpot initiative is a key growth driver. In addition, HubSpot's App Marketplace offers a customer-centric solution by making it simple for companies to find and seamlessly connect the integrations to grow their businesses.

However, HubSpot’s lower-priced starter offerings and seat-based pricing transition may continue affecting average subscription revenue growth in the near term. Although the revised pricing structure supports customer acquisition and upgrade flexibility, lower-priced packages could cannibalize premium offerings. Future pricing increases may also increase cancellation risks or push smaller customers toward free products, limiting monetization opportunities. Moreover, growing investments in data center infrastructure, sales & marketing and research & development continue to strain margins. Despite the increasing top line, mounting losses do not augur well for investor confidence. Reduced spend from small and medium-sized businesses amid a challenging business environment and macroeconomic headwinds remains a concern.

The Case for IBM

IBM is poised to benefit from healthy demand trends for hybrid cloud and AI, which drive the Software and Consulting segments. The company’s growth is expected to be aided by analytics, cloud computing and security in the long term. With a surge in traditional cloud-native workloads and associated applications, along with a rise in generative AI deployment, there is a radical expansion in the number of cloud workloads that enterprises are currently managing. This has resulted in heterogeneous, dynamic and complex infrastructure strategies, which have led firms to undertake a cloud-agnostic and interoperable approach to highly secure multi-cloud management, translating into a healthy demand for IBM hybrid cloud solutions.

IBM has integrated the open-source Mixtral-8x7B large language model into its watsonx AI and data platform. Mixtral-8x7B's incorporation underscores IBM's dedication to cutting-edge AI research and development. Built on innovative Sparse modeling and the Mixture-of-Experts technique, this model excels in rapid data processing and contextual analysis. Its ability to efficiently handle vast datasets makes it a valuable asset for businesses seeking actionable insights. The optimized version of Mixtral-8x7B, developed by Mistral AI, showcases impressive performance gains. Internal tests reveal a remarkable improvement in throughput compared to the standard model. By leveraging quantization techniques to reduce the model size and memory requirements, IBM anticipates significant reductions in latency, potentially boosting its top-line growth.

Despite solid hybrid cloud and AI traction, IBM is facing stiff competition from Amazon.com, Inc.’s AMZN AWS and Microsoft Corporation’s MSFT Azure. Increasing pricing pressure is eroding margins, and profitability has trended down over the years, barring occasional spikes. The company faces a potent threat from AI firm Anthropic as the latter’s Claude Code tool can modernize legacy COBOL systems — a foundational programming language deeply embedded in IBM’s mainframe ecosystem. With Claude Code proposing to substantially automate code exploration, documentation, refactoring and security analysis, it threatened to reduce enterprises’ reliance on specialized legacy service providers like IBM, bringing its sustenance at stake.

How Do Zacks Estimates Compare for HUBS & IBM?

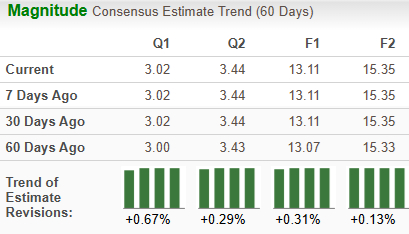

The Zacks Consensus Estimate for HubSpot’s 2026 sales suggests year-over-year growth of 18.3%, while that for EPS implies a rise of 35.1%. The EPS estimates have trended up 0.3% over the past 60 days.

Image Source: Zacks Investment Research

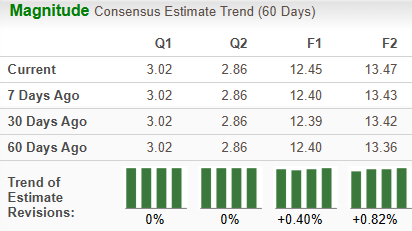

The Zacks Consensus Estimate for IBM’s 2026 sales and EPS indicates year-over-year growth of 6% and 7.4%, respectively. The EPS estimates have trended up 0.4% over the past 60 days.

Image Source: Zacks Investment Research

Price Performance & Valuation of HUBS & IBM

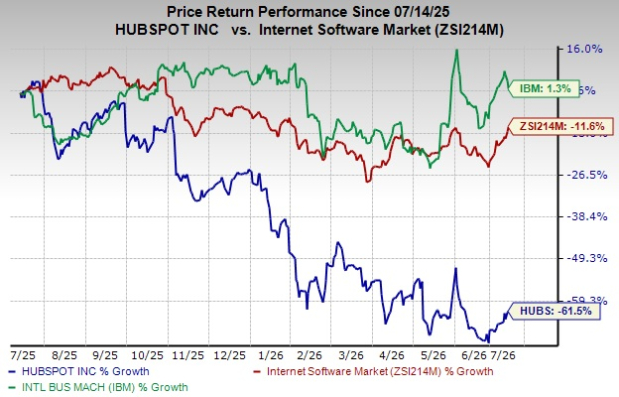

Over the past year, HubSpot has plunged 61.5% compared with the industry’s decline of 11.6%. IBM has gained 1.3% over the same period.

Image Source: Zacks Investment Research

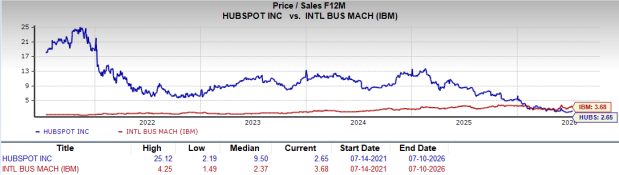

HubSpot looks more attractive than IBM from a valuation standpoint. Going by the price/sales ratio, HubSpot’s shares currently trade at 2.65 forward sales, lower than 3.68 for IBM.

Image Source: Zacks Investment Research

HUBS or IBM: Which is a Better Pick?

HubSpot carries a Zacks Rank #2 (Buy), while IBM carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both companies expect their earnings and revenues to improve in 2026. HubSpot is trading relatively more cheaply than IBM in terms of valuation metrics. With a superior Zacks Rank, HubSpot seems to have an edge over IBM and is therefore a better investment option at the moment.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

International Business Machines Corporation (IBM): Free Stock Analysis Report

HubSpot, Inc. (HUBS): Free Stock Analysis Report

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Microsoft Corporation (MSFT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).