Micron Technology, Inc. MU is reshaping its business model through long-term supply contracts that aim to reduce the earnings volatility typical of the memory industry. With artificial intelligence (AI) driving unprecedented demand for DRAM and NAND, these agreements could provide greater revenue visibility while supporting stable margins and stronger cash flows.

By the end of the third quarter of fiscal 2026, the company signed 16 Strategic Customer Agreements (SCAs) spanning data center, consumer and automotive markets. These contracts currently cover roughly 20% of Micron's DRAM volume and about one-third of its NAND volume over the contract period. Management expects these agreements to eventually account for half or more of total company revenues, significantly increasing the predictability of future sales.

The SCAs are structured as take-or-pay contracts, requiring customers to purchase committed volumes over multiple years. Most agreements include pricing bands with defined floor and ceiling prices, reducing the impact of sharp market swings while allowing pricing to adjust within agreed limits. Fourteen of the signed agreements represent approximately $100 billion in minimum contracted revenues over the remaining contract term. Customers have also committed about $22 billion through cash deposits and related financial commitments, highlighting confidence in Micron's long-term supply strategy.

These agreements come as AI-driven demand continues to outpace industry supply. Micron expects tight DRAM and NAND market conditions to extend beyond calendar year 2027, supported by limited wafer capacity and slower technology transitions. Combined with strong demand for HBM, data center SSDs and advanced memory products, the company's contract-based model should improve revenue visibility.

While memory remains a cyclical industry, these long-term supply agreements could make Micron's financial performance more stable than in previous cycles. The Zacks Consensus Estimate for fiscal 2026 revenues is currently pegged at $126.66 billion, indicating a robust $238.9% year-over-year surge.

How Do MU's Rivals Compare on Long-Term Revenue Visibility?

Micron's closest U.S.-listed competitors are Western Digital Corporation WDC and Seagate Technology Holdings Plc STX, though both focus primarily on storage rather than DRAM memory. Like Micron, they are benefiting from the AI-driven surge in enterprise storage demand, but their revenue visibility relies more on long-term cloud customer relationships than formal multi-year supply contracts.

Western Digital has seen strong demand for its enterprise SSDs and high-capacity HDDs, supported by AI data center investments and growing cloud deployments. The company expects continued growth as hyperscalers expand storage infrastructure for AI workloads. Western Digital’s third-quarter fiscal 2026 revenues rose 45% year over year to $3.34 billion.

Seagate is also capitalizing on the rising demand for mass-capacity storage. Its Mozaic platform, based on heat-assisted magnetic recording (HAMR) technology, enables higher-capacity hard drives that help customers lower storage costs. In the last reported financial results for the third quarter of fiscal 2026, Seagate’s revenues jumped 44% year over year to $3.11 billion.

Nonetheless, unlike Micron's take-or-pay SCAs that lock in committed purchase volumes, Western Digital and Seagate remain more exposed to fluctuations in enterprise storage spending and hard drive pricing. This gives Micron an advantage in revenue visibility, especially as its multi-year agreements provide committed demand, pricing discipline and stronger cash flow predictability during periods of tight memory supply.

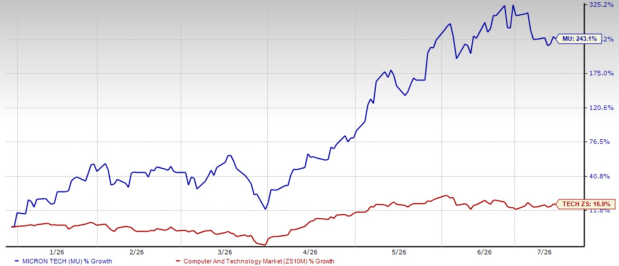

Micron’s Price Performance, Valuation and Estimates

Shares of Micron have surged around 243.1% year to date compared with the Zacks Computer and Technology sector’s return of 16.9%.

Micron Technology YTD Price Return Performance

Image Source: Zacks Investment Research

From a valuation standpoint, MU trades at a forward price-to-earnings ratio of 6.90, significantly lower than the sector’s average of 24.80.

Micron Technology 12-Month Forward P/E Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Micron’s fiscal 2026 and 2027 earnings implies a year-over-year increase of 791% and 107%, respectively. Bottom-line estimates for fiscal 2026 and 2027 have been revised upward in the past 30 days.

Image Source: Zacks Investment Research

Micron currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Micron Technology, Inc. (MU): Free Stock Analysis Report

Western Digital Corporation (WDC): Free Stock Analysis Report

Seagate Technology Holdings PLC (STX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).