Woodward, Inc. WWD reported first-quarter fiscal 2026 adjusted net earnings per share (EPS) of $2.17, which jumped 60.7% year over year and beat the Zacks Consensus Estimate by 31.5%.

Quarterly net sales increased 29% year over year to $996 million. The upside is fueled by market tailwinds across Aerospace and Industrial. The top line beat the consensus estimate by 10.1%.

Management highlighted that the company delivered a strong first-quarter 2026 performance that exceeded expectations, reflecting broad-based year-over-year growth across both segments, driven by strong demand and disciplined execution by our global teams. In Aerospace, margin expansion was supported by a richer mix of commercial services activity and robust defense OEM demand, while Industrial results benefited from strength in power generation, transportation and oil and gas markets.

The company’s continued focus on operational excellence is driving productivity gains and more consistent execution across the portfolio. Building on this strong start to the year, WWD raised its full-year sales and earnings guidance.

Post this announcement, the stock surged 15% in the after-market trading session yesterday. In the past year, shares have gained 78.3% compared with the Zacks Aerospace - Defense Equipment industry’s rise of 39.9%.

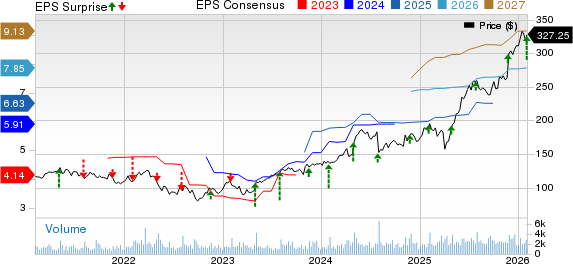

Image Source: Zacks Investment Research

WWD’s Segment Results

Aerospace: Net sales were $635 million, up 29% year over year, driven by broad-based strength across commercial services, commercial OEM and defense OEM. Defense OEM and defense services sales were up 23% and 1%, respectively, year over year. Commercial OEM sales were up 22% year over year, while services jumped 50%.

Segmental earnings were $148 million, up from $95 million a year ago. The gains were fueled by effective price realization, a more favorable product mix and higher sales volumes, though partly tempered by planned investments in Aerospace manufacturing and ongoing inflationary pressures. Margins expanded 420 basis points (bps) to 23.4%.

Woodward, Inc. Price, Consensus and EPS Surprise

Woodward, Inc. price-consensus-eps-surprise-chart | Woodward, Inc. Quote

Industrial: Net sales totaled $362 million, up 30% year over year, driven by gains across transportation, power generation and oil & gas markets. Core industrial sales, excluding the China on-highway impact, rose 22%.

Transportation sales rose 55%, and oil and gas sales increased 28%. Power generation grew a modest 7%, reflecting the sale of the combustion business in the prior year. Without that divestiture, power generation sales would have grown in the mid-20s on a percentage basis.

Segmental earnings were $67 million, up from $40 million in the year-ago quarter. In the core industrial segment, margins increased 410 bps to 18.5% of sales, led by strong pricing, higher volume and favorable mix, partially offset by inflationary pressures.

Other Details of WWD

Gross margin was up 480 bps year over year to 29.3%.

Total costs and expenses were $827.3 million, up 23.3% year over year.

Adjusted EBITDA was $207.8 million compared with $134.9 million a year ago.

WWD’s Cash Flow & Liquidity

As of Dec. 31, 2025, Woodward had $454.3 million in cash and cash equivalents with $457 million of long-term debt (less the current portion).

For the quarter ended Dec. 31, 2025, WWD generated $114.4 million of net cash from operating activities, increasing from $34.5 million reported in the prior-year period.

Free cash flow was $70 million compared with $1 million in the year-ago period. This uptick was driven by strong aerospace commercial services and higher China on-highway revenue within its Industrial segment. Notably, the company did not see the typical seasonal decline in demand and maintained steady production levels despite fewer working days during the quarter.

Capital expenditures reached $44 million in the first quarter, up from $34 million. The company expects capital spending to rise meaningfully over the remaining three quarters, driven primarily by the Spartanburg facility build-out and other ongoing automation initiatives.

In the quarter under review, WWD returned $146 million to its shareholders in the form of $17 million of dividends and $129 million worth of share repurchases.

WWD’s Fiscal 2026 Guidance

On the back of a strong first-quarter performance, Woodward has raised its guidance for fiscal 2026. The updated outlook assumes a continued robust demand environment, supporting ongoing sales growth and additional margin expansion.

Woodward expects consolidated net sales to rise 14% to 18% compared with the previous guidance of 7% to 12%. Aerospace is projected to grow 15% to 20% compared with the earlier projection of 9% to 15%, and Industrial is anticipated to increase 11% to 14% compared with the prior expectation of 5% to 9%.

Management stated that it plans to wind down the China on-highway business by the end of fiscal 2026. Aerospace segment earnings are still expected to be 22% to 23% of segment sales. Industrial segment earnings are estimated to be 16% to 17% compared with the prior view of 14.5% to 15.5% of segment sales.

Adjusted free cash flow is still anticipated to be between $300 million and $350 million. The company continues to project free cash flow in the range of $300-$350 million.

The company raised EPS guidance to $8.2-$8.6 from the previous expectation of $7.5-$8.

WWD’s Zacks Rank

Woodward currently carries a Zacks Rank #2 (Buy).You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Recent Performance of Other Companies

Teledyne Technologies Inc. TDY reported fourth-quarter 2025 adjusted earnings of $6.30 per share, which surpassed the Zacks Consensus Estimate of $5.83 by 8.1%. The bottom line also improved 14.1% from $5.52 recorded in the year-ago quarter.

Total sales were $1.61 billion, which beat the Zacks Consensus Estimate of $1.57 billion by 2.7%. The top line also surged 7.3% from $1.50 billion reported in the year-ago quarter.

Textron Inc. TXT reported fourth-quarter 2025 adjusted earnings of $1.73 per share, which missed the Zacks Consensus Estimate of $1.74 by 0.8%. However, the bottom line rose 29.1% from $1.34 in the year-ago quarter.

The company reported total revenues of $4.18 billion, which outpaced the Zacks Consensus Estimate of $4.14 billion by 0.8%. The top line also rose 15.7% from the year-ago quarter’s level of $3.61 billion.

Hexcel Corporation HXL reported fourth-quarter 2025 adjusted earnings of 52 cents per share, which came in line with the year-ago quarter’s figure. However, the bottom line topped the Zacks Consensus Estimate of 50 cents by 4%.

The company’s net sales totaled $491.3 million in the fourth quarter, which beat the Zacks Consensus Estimate of $478 million by 2.7%. The top line also rose 3.7% from the year-ago quarter’s reported sales of $473.8 million.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Textron Inc. (TXT): Free Stock Analysis Report

Hexcel Corporation (HXL): Free Stock Analysis Report

Teledyne Technologies Incorporated (TDY): Free Stock Analysis Report

Woodward, Inc. (WWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).