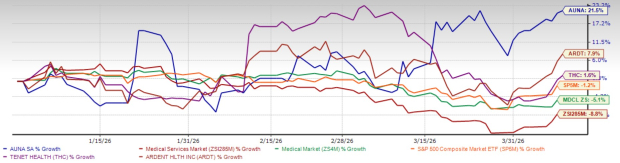

Shares of Auna S.A. AUNA, a Latin America-based healthcare service provider, have gained 21.5% so far this year. This compares to the 8.8% fall of the industry, the broader Medical sector’s 5.1% plunge and the S&P 500 composite’s 1.2% decline. The company has also fared better than its peers, Ardent Health ARDT and Tenet Healthcare THC, which have returned 7.9% and 1.6%, respectively, over the same period.

Auna’s YTD Price Comparison

Image Source: Zacks Investment Research

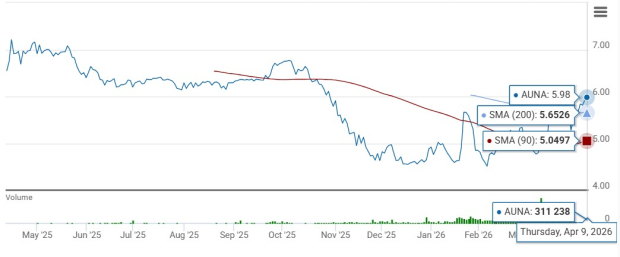

Yesterday, the stock closed the session at $5.98, nearly 34% higher than its 52-week low of $4.46. At current levels, shares are trading above their 90-day simple moving average (SMA) and 200-day SMA, suggesting solid upward momentum.

AUNA’s Technical Indicator

Image Source: Zacks Investment Research

Auna’s last quarterly update described 2025 as a stabilization phase, marked by an overhaul in its Mexico operations and a stronger capital structure. It now expects a return to growth in 2026. With improved perspective and predictability across operations, the company is projecting 12% revenue growth for the year, driven by sustained commercial momentum and operational execution. Adjusted EBITDA is also expected to rise 12% on an FX-neutral basis, supported by tighter cost control and continued investments in strategic growth initiatives.

Here are some key trends shaping the outlook.

AUNA’s Mexico Recovery Underway

The company continues to build out its healthcare network in this large and underpenetrated market through investments in infrastructure, technology and talent. Mexico operations showed strong signs of recovery in late 2025 and into 2026, following leadership adjustments in Monterrey. Under it, Auna S.A. is expanding its reach across larger segments of the privately insured population, rolling out packaged service offerings and strengthening collaboration with leading physicians to grow into key market segments — Out-of-Pocket, Corporates and Government Agencies. This should help broaden the revenue base and improve capacity utilization.

In the fourth quarter of 2025, the company secured favorable tier classifications with two major insurance providers and was awarded an extension to serve the ISSSTELEON healthcare plan under significantly improved commercial terms. Since the acquisition of Opción Oncología’s physician practice, oncology revenues are growing rapidly and are further supported by the launch of the new Oncocenter at Doctors Hospital.

Peru: A Key Contributor to Auna’s Growth

The Peru business continues to contribute strongly in terms of growth and profitability, underscoring the strength of Auna S.A.’s vertically integrated model at scale. Thefourth-quarter top line benefited from high-complexity services, which lifted average ticket sizes, as well as drove volumes higher on the back of investments in new medical equipment, increased bed capacity and targeted marketing initiatives. On the health plans side, Oncosalud’s plan memberships grew 4.4%, while its oncology MLR continued to improve, reaching a record low of 48.5%.

Peru’s growth profile has been strengthened with the authorization to begin the refurbishment, completion and opening of Centro Ambulatorio Trecca in Lima in 2028. The 23-storied, ambulatory facility is projected to expand the company’s addressable market and transform care delivery for up to three million beneficiaries annually for EsSalud, Peru’s Social Health Insurance agency.

AUNA’s Colombia Strategy

In response to political headwinds in Colombia, Auna S.A. has deliberately moderated growth by managing contracted services with intervened payors to mitigate payment risk and prioritize a positive cash cycle. The company reduced its exposure to Nueva EPS, one of the major government-intervened payors in Colombia, and diversified the payor base by adding Salud Total under a new Prospective Global Payments (“PGP”) program. Risk-sharing models like PGPs continued to expand in the fourth quarter, growing to 21% of segment revenues, up from 17% in the previous quarter.

Higher average tickets in surgery and sustained growth in emergency treatments like chemotherapy and imaging services had more than offset lower volumes as a result of reduced services to intervened payors.

A Look at Auna’s Liquidity and Debt Position

Auna S.A. entered 2026 with a significantly strengthened balance sheet, highlighted by a 42% increase in the year-end cash position. This gives it ample financial flexibility to continue executing on its strategic growth initiatives in Mexico and Peru. Free cash flow increased 35% over 2024, largely due to disciplined cost and expense management.

The company’s Net Debt-to-Adjusted EBITDA remained stable at 3.6X. The goal remains to bring down the leverage to below 3X over the medium term, mainly through EBITDA recovery, margin expansion and sustained free cash flow generation.

How Valuation Stacks Up for Auna S.A.

From a valuation perspective, AUNA appears attractive. Its shares are trading at a forward, 12-month, price/earnings (P/E) of 6.63X, lower than its median and industry average.

Auna’s 1 Year P/E

Image Source: Zacks Investment Research

Meanwhile, ARDT and THC trade at a P/E of 8.16X and 11.51X, respectively, over the past year.

Conclusion

Auna S.A. started 2026 on a stronger note, with its stock already outpacing the industry, peers and the broader market. Enhanced leadership and operational actions are driving early signs of recovery in Mexico, while Peru’s sustained strong performance has been a solid boost. In Colombia, risk mitigation measures are supporting cash generation.

With a stronger liquidity position, the company appears well-positioned to continue advancing its growth strategy across markets. Given Auna S.A.’s discounted valuation, existing investors may consider maintaining their positions. Prospective buyers, however, can wait for a better entry point.

AUNA carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Tenet Healthcare Corporation (THC): Free Stock Analysis Report

Auna S.A. (AUNA): Free Stock Analysis Report

Ardent Health, Inc. (ARDT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).