Chewy, Inc. CHWY has emerged as a dominant player in the online pet retail space, benefiting from the steady growth in pet ownership and the ongoing shift toward e-commerce. However, despite the strong market position, the stock is currently trading at a notable discount to its industry peers, raising an important question for investors: Does this valuation gap signal an attractive buying opportunity or reflect underlying concerns?

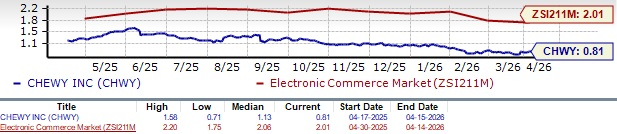

CHWY is currently trading at a trailing 12-month price-to-sales (P/S) multiple of 0.81X, which is at a discount compared with the industry’s average of 2.01X.

CHWY’s Valuation Snapshot

Image Source: Zacks Investment Research

This valuation is especially notable when compared with peers such as Central Garden & Pet Company CENT, which has a trailing 12-month P/S of 0.75, Petco Health and Wellness Company, Inc. WOOF at 0.15 and BARK, Inc. BARK at 0.19.

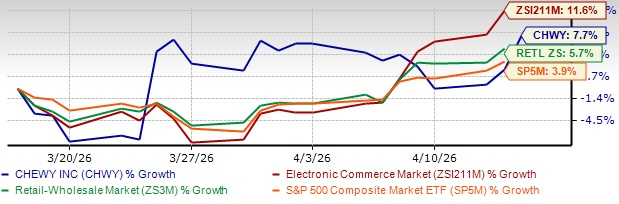

Chewy has witnessed a decent increase in its stock price in the past month. Closing yesterday’s trading session at $27.17, the stock has rallied 7.7% in a month, compared with the industry’s growth of 11.6%. Chewy's strategic initiatives and operational efficiency have enabled it to outperform the Retail - Wholesale sector’s 5.7% growth and the S&P 500 index’s 3.9% rise.

Image Source: Zacks Investment Research

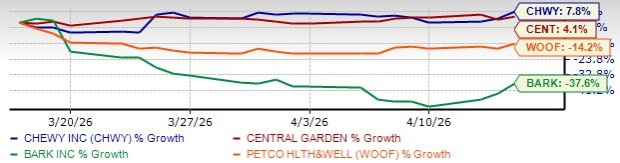

CHWY has outperformed its competitors, including Central Garden, Petco Health and BARK. In the same period, shares of Central Garden and BARK have increased 4.1% and declined 37.6%, respectively. Meanwhile, shares of Petco Health have slumped 14.2%.

CHWY’s Performance vs. Peer Performance

Image Source: Zacks Investment Research

Chewy Builds Momentum With Autoship Strength & AI Innovation

Chewy is entering fiscal 2026 with improving business momentum, underpinned by steady market share gains, increasing customer engagement and a resilient revenue structure. The company continues to benefit from favorable dynamics within the pet care industry, where demand tends to be stable due to recurring purchase behavior and strong emotional ties between consumers and their pets. This backdrop, combined with ongoing premiumization trends, is supporting Chewy’s positioning within the expanding digital pet ecosystem. With the active customer base reaching 21.3 million and management indicating continued sequential additions, the company appears well placed to further strengthen its competitive standing.

A key driver of Chewy’s growth remains its recurring revenue model, led by the Autoship program. Autoship now accounts for more than 83.3% of total net sales and continues to outpace overall company growth, enhancing revenue visibility and customer retention. This subscription-based model not only stabilizes demand but also supports higher customer lifetime value. Additionally, the company is seeing increased traction in higher-margin categories such as health, wellness and veterinary services, which are contributing to improved net sales per active customer and reinforcing long-term spending trends.

Beyond its core retail operations, Chewy is increasingly leveraging technology to drive efficiency and differentiation. The company has developed an integrated enterprise data platform and is actively embedding artificial intelligence across multiple functions, including customer service, fulfillment, pharmacy operations and marketing. These initiatives are expected to enhance personalization, improve search functionality and optimize operational productivity. Management anticipates that AI-led efficiencies will generate a financial benefit in the low tens of millions of dollars in fiscal 2026, with the potential to scale to more than $50 million in annualized savings by fiscal 2027 as adoption broadens.

Strategic expansion initiatives are also contributing to Chewy’s evolving growth profile. The company is building an omnichannel presence through its Chewy Vet Care offering, which currently operates 18 locations across five states. This initiative not only diversifies revenue streams but also strengthens customer acquisition and retention by integrating services with its digital platform. At the same time, the introduction of Chewy Made and the continued expansion of private-label products provide an incremental margin opportunity, particularly within the large consumables category, where penetration remains relatively low.

What to Expect From CHWY in the Future?

For fiscal 2026, Chewy expects net sales to reach $13.6-$13.75 billion, indicating approximately 8-9% year-over-year growth. This outlook is supported by continued share gains, stable demand in the pet category and balanced growth across active customer additions and higher spend per customer, with no reliance on pricing inflation.

The company also expects another year of meaningful profitability expansion, guiding for adjusted EBITDA margins in the range of 6.6-6.8%, implying roughly 100 basis points of year-over-year improvement. Notably, EBITDA growth is projected to outpace revenue growth by nearly three times, supported by operating leverage, disciplined cost management and structural drivers such as SG&A efficiencies, high-margin category mix and AI-led productivity gains, which are expected to deliver meaningful cost savings.

Upward Estimate Revisions Signal Optimism on CHWY’s Earnings

Reflecting positive sentiment around Chewy, the Zacks Consensus Estimate for EPS has seen upward revisions. In the past 30 days, the consensus estimates for the current and next fiscal years have increased 7 cents to $1.63 and 8 cents to $1.99 per share, respectively.

Image Source: Zacks Investment Research

How to Play CHWY Stock?

Chewy offers a compelling opportunity for long-term investors, supported by the strength of its recurring Autoship revenue model, rising customer engagement and continued expansion across strategic growth initiatives, including Chewy Vet Care, private brands and AI-led efficiencies. The company’s expanding active customer base and steady market share gains further reinforce confidence in its long-term growth trajectory. Coupled with disciplined financial execution and solid business momentum, Chewy remains well positioned to deliver sustained growth and long-term value creation.

Given this setup, existing investors may consider gradually increasing their exposure, while new investors could view current levels as an attractive entry point. Chewy currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Central Garden & Pet Company (CENT): Free Stock Analysis Report

Petco Health and Wellness Company, Inc. (WOOF): Free Stock Analysis Report

Chewy (CHWY): Free Stock Analysis Report

BARK, Inc. (BARK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).