Docusign DOCU continues to demonstrate steady business momentum, supported by rising demand for digital agreement solutions and a highly scalable subscription model. However, despite these positives, certain financial and competitive concerns keep the stock in a balanced “Rank 3 – Hold” category for now.

Strong Demand in a Large Untapped Market

Docusign’s core strength lies in its eSignature business, which continues to benefit from the global shift toward digital workflows. The company’s customer base has expanded consistently over recent years, reaching nearly 1.8 million customers in fiscal 2026. This steady growth reflects strong adoption across enterprises and small businesses alike.

Importantly, the overall e-signature market remains far from saturated. Industry estimates suggest that the global market could grow significantly over the next several years, leaving ample room for Docusign to expand. Even with competition from players like Adobe’s ADBE Acrobat Sign, the opportunity pool is large enough to support multiple winners. This gives Docusign a long runway for sustained revenue growth. As Adobe continues to innovate within digital documents, the competitive landscape is evolving but still far from closed.

DOCU’s Subscription Model Adds Stability

One of Docusign’s biggest advantages is its subscription-based business model, which accounts for roughly 97% of total revenues. This model provides predictable cash flows, improves revenue visibility, and enhances customer retention.

The company has also been successful in expanding revenue from existing customers while adding new ones. Subscription revenues grew steadily in fiscal 2026, supported by strong go-to-market strategies and customer engagement initiatives. This recurring revenue structure acts as a cushion during uncertain macro conditions and strengthens long-term financial stability.

DOCU’s International Expansion Driving Growth

Docusign is increasingly tapping global markets to fuel its next phase of growth. International revenues have steadily increased as a percentage of total revenues, reflecting successful expansion efforts in regions like Canada, the UK and Australia.

These markets share similar regulatory and operational frameworks for e-signatures, allowing Docusign to leverage its existing technology efficiently. As digital transformation accelerates globally, international markets could become a major growth driver. Partnerships with global platforms like Microsoft MSFT also support this expansion by enabling broader enterprise adoption across regions.

Strategic Partnerships and Product Innovation

The company is actively enhancing its ecosystem through partnerships and innovation. Collaborations with major platforms like Salesforce CRM and Microsoft allow Docusign to integrate its solutions into widely used enterprise tools, significantly expanding its reach.

For instance, integrations with Salesforce streamline contract workflows directly within CRM environments, while deeper alignment with Microsoft tools enhances productivity within collaboration ecosystems. At the same time, DocuSign is investing in AI-driven solutions such as its Intelligent Agreement Management platform and contract review tools. Even as Adobe strengthens its own AI-driven document capabilities, DocuSign continues to differentiate through workflow automation.

Financial and Competitive Concerns

Despite these positives, there are some red flags investors should not ignore. The company’s liquidity position has weakened, with its current ratio falling below 1 at the end of the fourth quarter of fiscal 2026. This suggests limited short-term financial flexibility compared to industry standards.

Additionally, pricing pressure remains a key risk. As competition intensifies, especially from large players and emerging solutions, Docusign may face challenges in maintaining its pricing power. Large enterprise clients could also push for discounts, impacting margins over time.

No Dividends and Stock Volatility

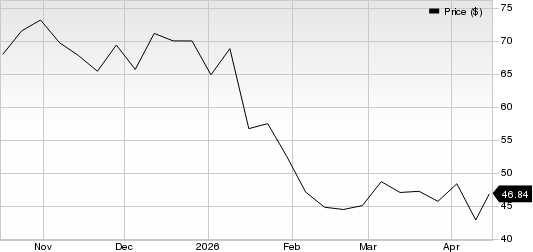

Docusign does not pay dividends, meaning investors rely entirely on stock price appreciation for returns. This becomes a concern given the stock’s recent volatility, including a notable 31% decline over the past six months. For income-focused investors, this reduces the stock’s attractiveness.

Docusign Inc. Price

Docusign Inc. price | Docusign Inc. Quote

Hold DOCU for Now

Docusign’s strong market position, recurring revenue model, and expanding global footprint make it a compelling long-term story. However, liquidity concerns, competitive risks and lack of dividends create a balanced risk-reward scenario.

For now, the stock fits best in a “Hold” category. Investors may consider staying invested while monitoring execution, margin stability and competitive dynamics before making fresh commitments.

DOCU currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks Rank #1 (Strong Buy) stocks here.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT): Free Stock Analysis Report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Adobe Inc. (ADBE): Free Stock Analysis Report

Docusign Inc. (DOCU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).