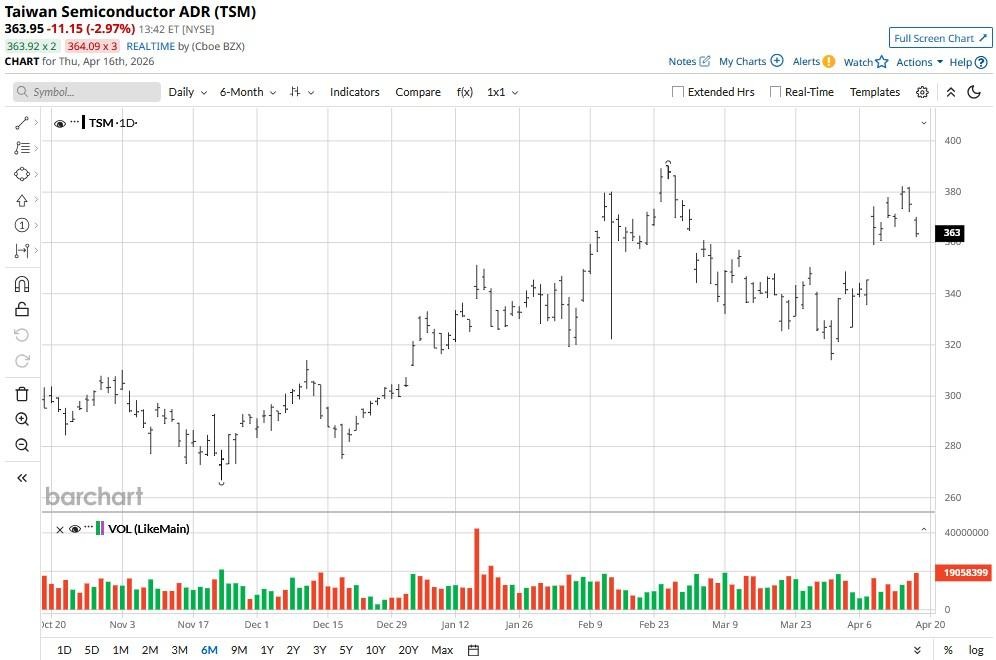

Investors are bailing on Taiwan Semiconductor (TSM) shares today, even after the company posted blockbuster earnings for its first quarter.

The world’s largest foundry saw its profit increase by 58% year-over-year as revenue climbed to a record on insatiable artificial intelligence (AI) demand.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Despite this post-earnings dip, TSM stock remains up about 14% versus the start of this year.

www.barchart.com

www.barchart.comWhy Did TSMC Stock Slip on Thursday?

TSM shares slipped this morning because of three big reasons: cautious guidance, valuation risks, and rising capex.

While AI chip demand remains robust, management’s decision to maintain, rather than lift it full-year outlook significantly signals a potential plateau in non-AI segments like smartphones and PCs.

Plus, TSMC hinted at a meaningful increase in capital expenditures, now targeting the upper end of its $52 billion to $56 billion range.

This aggressive spending, coupled with a forward price-to-earnings (P/E) ratio of about 26x, well above its five-year median, triggered profit-taking among investors wary of priced-for-perfection valuations.

Is It Worth Buying the Dip in TSM Shares?

EFM Asset Management’s senior analyst Daniel Heyler, nonetheless, remains positive on TSMC’s long-term trajectory, especially since it's strongly positioned to weather the expected helium supply shock from the Iran war.

Speaking recently with CNBC, Heyler cited the firm’s prowess in recycling, deep inventory buffers, and priority status with international gas suppliers for his bullish view on the semiconductor stock.

TSMC shares are worth buying on the post-earnings dip because the company’s unrivaled moat in 2nm and 3nm process technologies makes it the fundamental backbone of the global AI revolution.

Taiwan Semiconductor’s rising capex is not a sign of waste but a calculated bet on a future where every industry requires high-performance computing.

A 0.96% dividend yield makes it all the more attractive to own in 2026.

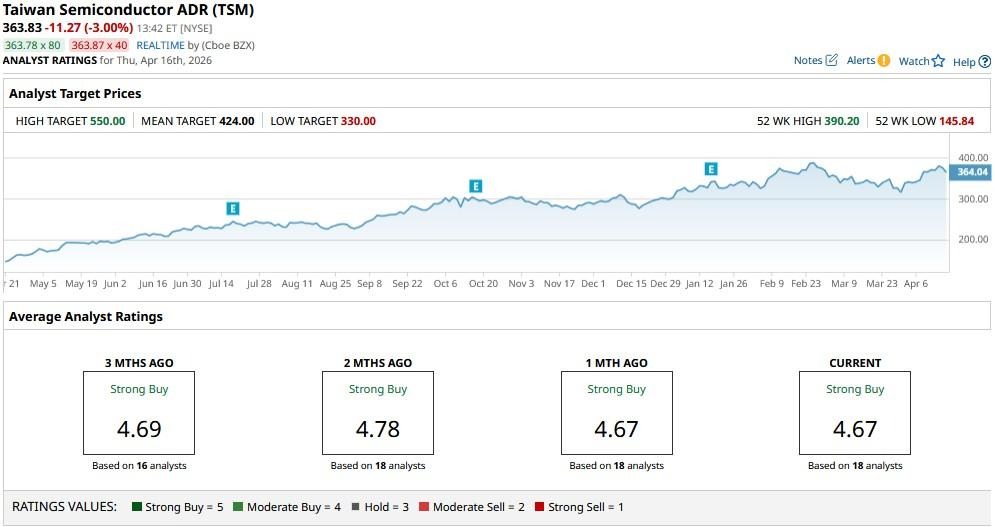

Wall Street Remains Bullish on Taiwan Semiconductor

Wall Street also remains bullish on TSMC stock, given its dominant market share in foundry and a track record of passing through cost increases to customers like Apple (AAPL) and Nvidia (NVDA).

The consensus rating on Taiwan Semiconductor currently sits at a “Strong Buy," with the mean price target of about $424 indicating potential upside of about 17% from here.

www.barchart.com

www.barchart.com On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Is Bloom Energy Stock a Buy, Sell, or Hold at New All-Time Highs? Does the QQQ ETF Have a Bad Case of Premature Accumulation? Is the Software Apocalypse Real? Piper Sandler Just Slashed Its Price Target on Salesforce Stock. As Airline Stocks Sell Off on Jet Fuel Prices, Delta Is the Top-Rated Stock to Buy on the Dip