Seagate Technology Holdings plc STX has been a prominent player in the global data storage market, benefiting from secular tailwinds such as cloud computing, AI workloads and data center expansion. Seagate’s key financial strength is its consistent and improving cash flow generation. However, despite strong operations, the company still faces concerns due to high debt and a stretched balance sheet.

Seagate generates strong cash flow, enabling investments in innovation, acquisitions and business growth while continuing to reward shareholders through dividends and buybacks. In fiscal 2025, it reduced debt by $684 million, reflecting a balanced capital allocation strategy. For second-quarter fiscal 2026, it reported $723 million in operating cash flow and $607 million in free cash flow, returning $154 million via dividends and retiring $500 million in debt. With expectations of higher free cash flow ahead driven by strong demand, efficiency and disciplined spending, Seagate remains well-positioned to support its HAMR transition, sustain dividends and improve profitability.

Despite strong cash flows, Seagate’s leverage remains elevated, which could pressure the company’s ability to sustain dividends, execute buybacks and pursue future acquisitions. As of Jan. 2, 2026, Seagate held $1.05 billion in cash against $4.5 billion in long-term debt, resulting in a high debt-to-capital ratio of 90.7% versus the industry’s 36.8%. This elevated leverage, driven by acquisitions and growth investments, supports expansion but also raises financial risk.

Nonetheless, there have been important improvements. The net leverage ratio was 1.1, supported by adjusted EBITDA of $962 million, up 16% sequentially and 63% year over year in the December quarter. With rising profitability and cash flow, the company expects leverage to decline further while continuing to reduce debt.

How STX’s Competitors are Placed on Leverage & Liquidity

Western Digital Corporation WDC is balancing shareholder returns with strategic investments, via dividends and ongoing share buybacks. Strong execution drove fiscal second-quarter operating cash flow to $745 million and free cash flow to $653 million, up 95%, enabling WDC to return more than 100% of FCF to shareholders. It repurchased $615 million in stock and paid $48 million in dividends, with total returns reaching $1.4 billion since late fiscal 2025 and a new $4 billion buyback authorization in place. However, with $2 billion in cash against $4.7 billion in debt, its leveraged balance sheet remains a concern, requiring sustained cash flow to support obligations and future growth.

Micron Technology MU boasts a strong balance sheet with $16.7 billion in cash and investments and $20.2 billion in liquidity, supporting acquisitions, growth and shareholder returns. It generated $20.3 billion in operating cash flow in the first half of fiscal 2026, delivering $10.8 billion in free cash flow even after $9.5 billion in capex, while returning cash via buybacks and dividends. However, the projected capex of more than $25 billion for fiscal 2026 focused on DRAM and HBM expansion raises risks. If AI-driven demand falls short or pricing weakens, the high capital intensity could pressure free cash flow and limit financial flexibility.

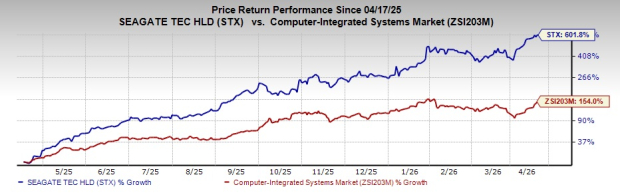

STX’s Price Performance, Valuation & Estimates

In the past year, STX shares have skyrocketed 601.8%, outperforming the Computer Integrated Systems industry’s growth of 154%.

Image Source: Zacks Investment Research

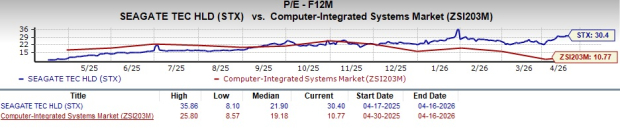

Valuation-wise, STX seems attractive, as suggested by the Value Score of B. In terms of forward price/earnings, STX’s shares are trading at 30.4X, higher than the industry’s 10.77X.

Image Source: Zacks Investment Research

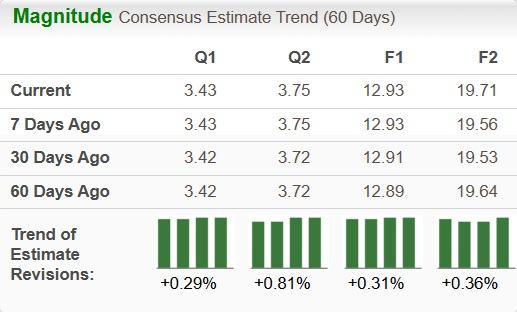

The Zacks Consensus Estimate for STX’s earnings for fiscal 2026 has been revised up marginally over the past 60 days.

Image Source: Zacks Investment Research

Currently, Seagate has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Western Digital Corporation (WDC): Free Stock Analysis Report

Seagate Technology Holdings PLC (STX): Free Stock Analysis Report

Micron Technology, Inc. (MU): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).