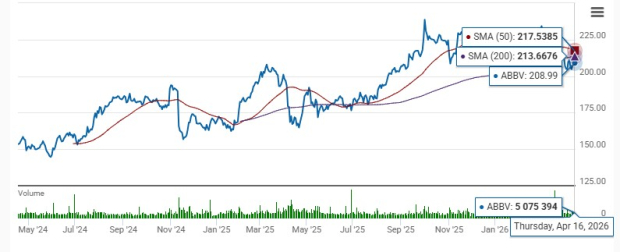

AbbVie ABBV stock is currently trading below its 50-day and 200-day simple moving averages (SMAs). A stock trading below both its 50-day and 200-day simple moving averages is generally viewed as being in a sustained downtrend, reflecting weakness in both short-term momentum and long-term investor sentiment.

In such cases, these moving averages tend to act as resistance levels, making upward moves harder to sustain unless supported by strong volume or positive catalysts. However, while this configuration is typically bearish, it can also indicate that the stock is oversold and nearing a potential rebound or accumulation phase, especially if fundamentals remain intact.

Let’s examine the company’s strengths and weaknesses to better analyze how to play AbbVie stock in this situation.

ABBV’s Successful Immunology Drugs — Skyrizi and Rinvoq

AbbVie lost patent protection for its blockbuster drug, Humira, in the United States in January 2023 and in the EU in 2018. Humira's sales are declining due to loss of exclusivity (LOE) and biosimilar erosion. AbbVie has successfully navigated the LOE of Humira, a drug that once generated more than 50% of its total revenues. It has accomplished this by launching two other successful new immunology medicines, Skyrizi and Rinvoq, which are performing extremely well, bolstered by approvals in new indications, and should support top-line growth in the next few years.

Skyrizi and Rinvoq generated combined sales of $26.0 billion in 2025, exceeding expectations and representing year-over-year growth of more than 40%. The drugs delivered strong performance across all approved indications, especially in the popular inflammatory bowel disease space, which includes two conditions — ulcerative colitis (UC) and Crohn’s disease. In 2026, AbbVie expects combined Skyrizi and Rinvoq sales of more than $31 billion.

Strong immunology market growth, market share gains and momentum from new indications, as well as the potential for five new indications for Rinvoq over the next few years, are expected to drive the drugs’ growth. Rinvoq could be approved for two indications — vitiligo and alopecia areata — in 2026. Phase III data on Rinvoq in hidradenitis suppurativa and systemic lupus erythematosus are expected this year. AbbVie believes that the next wave of potential approvals in Rinvoq could add roughly $2 billion to peak-year sales for the product.

AbbVie expects a low single-digit pricing headwind for both Skyrizi and Rinvoq in 2026 and over the next few years.

ABBV’s Oncology and Neuroscience Drug Contributions

AbbVie’s neuroscience portfolio is also contributing to top-line growth. Sales of its neuroscience drugs increased almost 20% to $10.8 billion in 2025, driven by higher sales of Botox Therapeutic, depression drug Vraylar and newer migraine drugs Ubrelvy and Qulipta.

The initial international launch uptake of Vyalev, a transformative therapy for treating advanced Parkinson’s disease, approved in late 2024, has been encouraging. AbbVie expects Vyalev to achieve blockbuster status in 2026, with sales expected to ramp up substantiallyin the United States, where Vyalev recently received full coverage. AbbVie’s Parkinson’s disease franchise, comprising Vyalev and once-daily oral treatment tavapadon (under review in the United States; FDA decision expected in the third quarter of 2026), is viewed as a key driver of growth in neuroscience.

AbbVie has built a substantial oncology franchise with Imbruvica and Venclexta. Its oncology segment generated combined revenues of $6.6 billion in 2025, up 1.5% year over year, as higher Venclexta sales and contributions from new drugs, Elahere and Epkinly, partially offset the decline in Imbruvica sales.

Some key oncology drugs approved in the past couple of years are Epkinly and Emrelis. Elahere was added to AbbVie’s oncology portfolio with the February 2024 acquisition of Immunogen. These three new drugs have strengthened AbbVie’s oncology franchise. Though oncology sales are slightly slowing down, AbbVie believes the oncology pipeline is robust with several study readouts and initiations expected this year.

Over the next couple of years, AbbVie expects new product approvals for tavapadon and pivekimab sunirine (blastic plasmacytoid dendritic cell neoplasm) and pivotal data readouts for key pipeline candidates, lutikizumab (hidradenitis suppurativa

), Temab-A (metastatic colorectal cancer) and etentamig (third-line-plus multiple myeloma). These pipeline programs have the potential to drive long-term growth for AbbVie, while Skyrizi and Rinvoq will boost near-term growth.

AbbVie on an Acquisition Spree

AbbVie has been on an acquisition spree over the past couple of years to bolster the early-stage pipeline that should drive long-term growth. It is signing several M&A deals in the immunology space, its core area, while also signing some early-stage deals in oncology and neuroscience.

In 2025, AbbVie invested more than $5 billion to acquire innovative pipeline candidates. These include an in-vivo CAR-T platform in immunology from Capstan Therapeutics, bretisilocin, a next-generation psychedelic in depression; ISB-2001, a novel trispecific antibody for multiple myeloma; 295, a long-acting amylin analog for obesity and a next-generation siRNA platform from Arx.

ABBV’s Struggling Aesthetics Segment & Humira Erosion

Sales of Humira are declining due to biosimilar erosion. The launch of Humira biosimilars in the United States in 2023 significantly eroded the drug’s sales in 2024 and 2025. Humira sales declined around 50% in 2025. Humira sales are expected to continue to decline in 2026 as more plans exclude branded Humira and move to exclusive biosimilar contracts.

AbbVie’s Aesthetics unit is also experiencing declining sales due to continued macro challenges and weakened consumer sentiment. Global sales of the aesthetics portfolio declined 0.6% in 2024 and 5.9% in2025.

While Juvederm sales declined 15.6% in 2025, Botox Cosmetics sales deteriorated 4.1%. AbbVie expects the aesthetics category growth to remain challenged in 2026. Global aesthetics sales are projected to be $5 billion in 2026, flat year over year, as moderate growth in Botox Cosmetic is likely to be offset by continued decline in Juvederm sales due to continued headwinds in key dermal filler markets.

ABBV Stock Price, Valuation and Estimate Revision

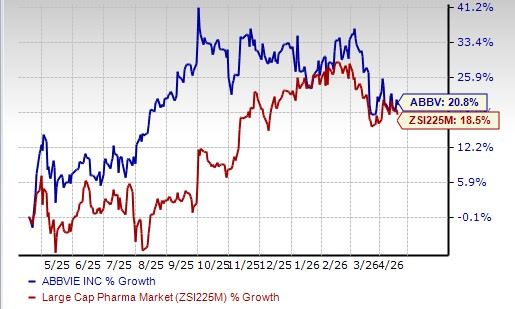

ABBV stock has risen 20.8% in the past year compared with an appreciation of 18.5% for the industry.

ABBV Stock Outperforms Industry

From a valuation standpoint, AbbVie is reasonably priced. Going by the price/earnings ratio, the company’s shares currently trade at 14.20 forward earnings, lower than 16.97 for the industry. However, the stock is trading above its five-year mean of 13.82. The stock is cheaper than other large drugmakers like AstraZeneca AZN, Eli Lilly LLY and J&J JNJ.

ABBV Stock Valuation

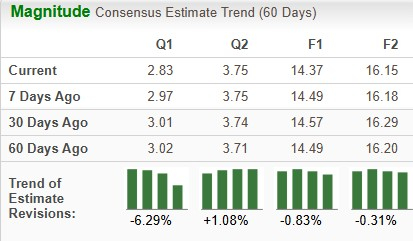

Earnings estimates for 2026 have declined from $14.57 to $14.37 over the past 30 days, while those for 2027 have declined from $16.29 to $16.15 over the same time frame. This is due to the impact of acquired IPR&D and milestones expense expected to be recorded in the first quarter of 2026, as mentioned in a SEC filing released by the company earlier this month.

ABBV Estimate Movement

Stay Invested in ABBV Stock

AbbVie combats its share of headwinds, including the impact of Humira LOE, increasing competitive pressure on Imbruvica and continued macro woes for Aesthetics. The company has faced its biggest challenge — Humira’s patent cliff — quite well and looks well-positioned for continued strong growth in the years ahead.

ABBV delivered robust net sales growth in 2025, which is just the second full year following the Humira LOE in the United States. AbbVie expects another year of robust growth in 2026. It expects total revenues to rise approximately 9.5% in 2026. The top-line growth is likely to be driven by continued strong increase in Skyrizi and Rinvoq sales, a substantial top-line ramp for Vyalev and continued double-digit revenue growth from migraine drugs, partially offset by headwinds from continued Humira erosion and the impact of lower IRA-related pricing on Imbruvica.

It expects high single-digit revenue growth through 2029, as the company has no significant LOE events for the rest of this decade. A substantial portion of this growth is expected to be driven by the robust performance of Skyrizi and Rinvoq. AbbVie also has the flexibility to invest more in R&D and continue acquiring external innovations.

A key reason why ABBV stock seems to have slipped below the 50- and 200-day SMAs could be a lack of news flow, no strong near-term catalysts expected, as well as underlying transition concerns (Humira erosion, softness in the aesthetics segment).

Long-term investors can continue to retain this Zacks Rank #3 (Hold) stock in their portfolio as the company enjoys strong fundamentals, a solid pipeline and growth outlook. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AstraZeneca PLC (AZN): Free Stock Analysis Report

Johnson & Johnson (JNJ): Free Stock Analysis Report

Eli Lilly and Company (LLY): Free Stock Analysis Report

AbbVie Inc. (ABBV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).