SoFi Technologies, Inc. SOFI is benefiting from growing demand for its online banking services and the Galileo platform. Interest rate cuts boost its lending business growth through competitive loan and refinancing options. The company’s innovative new product launches and strategic partnerships lift its reputation among clients.

However, weak liquidity and heavy reliance on personal loans put pressure on profitability and scalability. The absence of dividends further deters risk-averse investors seeking stability and consistent income.

How is SOFI Faring?

SoFi Technologies’ continuous digitalization across industries, particularly in the financial sector, presents a significant opportunity. The company is focusing on online banking and offering a comprehensive suite of products and services to support the rising demand for online financial platforms. Its technology platform, Galileo, is gaining popularity and is being adopted by new financial firms, giving the company a clear pathway for sustainable growth.

The company’s lending business benefits from Federal Reserve interest rate cuts. Lower interest rates reduce borrowing costs, improving its loan origination volumes and enhancing its overall profitability. This encourages more customers to take loans and refinance existing ones, enabling the company to extend its customer base.

Stricter forgiveness policies under the Trump administration further enable SOFI to offer competitive rates and flexible terms in its student loan-refinance business. These criteria may prompt borrowers to seek refinancing options to lower repayment costs, creating opportunities for the company to expand its customer reach.

SOFI’s large-scale production and sales enable it to have an efficient cost structure. Recent collaborations and new launches are expected to enhance scalability. Its recent $2 billion partnership with Fortress Investment Group aims to diversify its revenue streams toward fee-based, less capital-intensive models. The Nova Credit integration enhances SoFi’s risk assessment capabilities and expands its market reach and customer engagement.

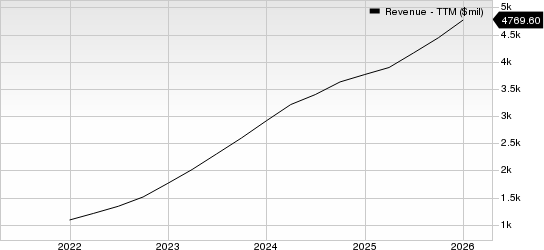

SoFi Technologies, Inc. Revenue (TTM)

SoFi Technologies, Inc. revenue-ttm | SoFi Technologies, Inc. Quote

However, SoFi’s heavy reliance on the personal loan segment exposes it to credit risk. Personal loans constitute nearly 70% of SOFI’s lending portfolio. Though this segment has driven revenue growth, it inherently carries a higher default risk, resulting in the stock being unappealing to risk-averse investors.

SOFI’s current ratio (a measure of liquidity) at the end of the fourth quarter of 2025 was 0.78, lower than the industry average of 1.2. A current ratio below 1 often indicates that the company may not be well-positioned to pay off its short-term obligations.

The company has neither declared nor indicated any intention to pay cash dividends, making share price appreciation the sole avenue for return, which is subject to market volatility and business performance. This makes the stock unattractive for income-seeking investors who rely on regular dividend payouts.

SOFI’s fourth-quarter 2025 results were impressive. It earned an adjusted profit of 13 cents per share, which beat the Zacks Consensus Estimate by 8.3% and marked a massive improvement of 160% from the year-ago quarter. Revenues of $1 billion surpassed the consensus estimate by 3.2% and rose 40% year over year.

SoFi Technologies currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Earnings Snapshots of Some Players

Waste Connections, Inc. WCN reported impressive fourth-quarter 2025 results.

Waste Connections’ adjusted earnings (excluding 28 cents from non-recurring items) of $1.29 per share marginally beat the Zacks Consensus Estimate and increased 11.2% year over year. WCN’s revenues of $2.4 billion met the consensus estimate and grew 5% from the year-ago quarter.

Equifax Inc. EFX posted impressive fourth-quarter 2025 results.

Equifax’s adjusted earnings were $2.09 per share, outpacing the Zacks Consensus Estimate by 2.5% but declining 1.4% from the year-ago quarter. EFX’s total revenues of $1.6 billion surpassed the consensus estimate by 1.3% and grew 9.2% on a year-over-year basis.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Equifax, Inc. (EFX): Free Stock Analysis Report

Waste Connections, Inc. (WCN): Free Stock Analysis Report

SoFi Technologies, Inc. (SOFI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).