Howmet Aerospace Inc. HWM has consistently delivered margin expansion over recent quarters. In the fourth quarter of 2025, the cost of sales rose 3.4% year over year, primarily due to higher input costs and increased headcount. This followed year-over-year increases of 8.9% in the third quarter and 6.1% in the second quarter, while the cost of sales remained flat in the first quarter.

Despite these headwinds, Howmet has maintained consistent margin expansion. The company reported an adjusted EBITDA margin of 28.8% in the first quarter of 2025, 28.7% in the second quarter and 29.4% in the third quarter. In the fourth quarter, HWM sustained this momentum with a margin of 28.7%, marking a 300-basis point improvement from the prior year.

Also, the Engine Products, Fastening Systems and Engineered Structures segments reported margin gains of 290, 290 and 350 basis points, respectively, supported by a favorable product mix, manufacturing footprint optimization and effective pricing actions.

Strong demand from both the commercial and defense aerospace markets continues to support the company’s overall performance. For 2026, Howmet expects adjusted EBITDA margin to be 30.1-30.5%. The company reported adjusted EBITDA of 29.3% in 2025. Strong pricing and ongoing productivity improvements are expected to support Howmet’s margin expansion in 2026.

Margin Performance of HWM’s Peers

Among its major peers, RTX Corp.’s RTX total costs and expenses increased 10.9% year over year to $22 billion in the fourth quarter of 2025. RTX Corp. generated an adjusted operating profit of $2.6 billion in the fourth quarter. RTX Corp. reported adjusted operating profit of $2.1 billion in the prior-year quarter.

Its another peer, GE Aerospace’s GE cost of sales surged 23.7% year over year in the fourth quarter of 2025. GE Aerospace’s operating profit increased 14% year over year. GE Aerospace’s operating margin was 19.2%, down 90 bps year over year.

HWM's Price Performance, Valuation and Estimates

Shares of Howmet have surged 100.9% in the past year compared with the industry’s growth of 27.1%.

Image Source: Zacks Investment Research

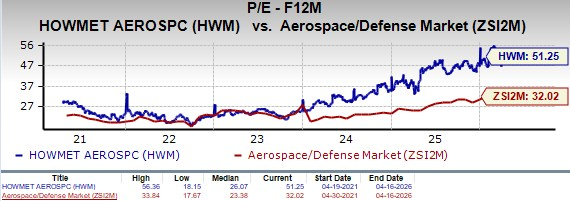

From a valuation standpoint, HWM is trading at a forward price-to-earnings ratio of 51.25X, above the industry’s average of 32.02X. Howmet carries a Value Score of F.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for HWM’s 2026 earnings has increased 2.9% over the past 60 days.

Image Source: Zacks Investment Research

Howmet currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

#1 Semiconductor Stock to Buy (Not NVDA)

The incredible demand for data is fueling the market's next digital gold rush. As data centers continue to be built and constantly upgraded, the companies that provide the hardware for these behemoths will become the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to take advantage of the next growth stage of this market. It specializes in semiconductor products that titans like NVIDIA don't build. It's just beginning to enter the spotlight, which is exactly where you want to be.

See This Stock Now for Free >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

GE Aerospace (GE): Free Stock Analysis Report

Howmet Aerospace Inc. (HWM): Free Stock Analysis Report

RTX Corporation (RTX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).