Biotech giant Bristol-Myers Squibb Company BMY is scheduled to report first-quarter 2026 results on April 30, before market open. The Zacks Consensus Estimate for sales and earnings is pegged at $10.94 billion and $1.44 per share, respectively.

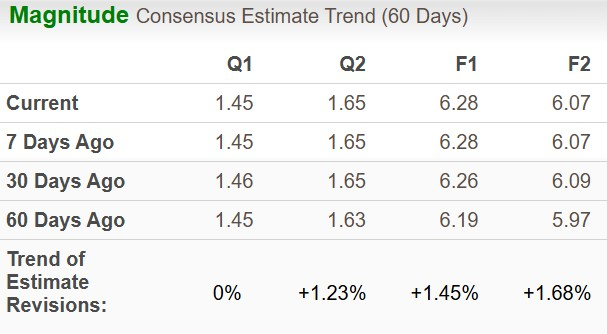

Earnings estimate for 2026 has increased to $6.28 from $6.26 per share over the past 30 days, while that for 2027 has decreased to $6.07 from $6.09.

Image Source: Zacks Investment Research

BMY’s Earnings Surprise History

BMY has an excellent track record. Its earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 18.84%. In the previously reported quarter, the company’s earnings beat estimates by 9.57%.

Image Source: Zacks Investment Research

What Our Model Predicts for BMY

Per our proven model, the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat.

Earnings ESP for BMY is -1.02%. The company currently carries a Zacks Rank #3. You can uncover the best stocks to buy or sell before they're reported with our Earnings ESP Filter.

Factors Influencing BMY’s Q1 Results

BMY’s top line has likely gained from an increase in growth portfolio sales. The growth portfolio primarily comprises sales from drugs like Opdivo, Opdivo Qvantig, Orencia, Yervoy, Reblozyl, Camzyos, Breyanzi, Opdualag, Zeposia, Abecma, Sotyku, Krazati and Cobenfy.

Consistent label expansions in newer metastatic and adjuvant indications (MSI-high colorectal cancer and first-line non-small cell lung cancer) have likely maintained momentum for immuno-oncology drug Opdivo in the first quarter. The Zacks Consensus Estimate and our model estimate for Opdivo sales are pegged at $2.2 billion and $2.17 billion, respectively.

The approval of Opdivo Qvantig (nivolumab and hyaluronidase-nvhy) injection for subcutaneous use has boosted BMY’s immuno-oncology portfolio. Initial uptake is robust across all approved tumor types in the United States.

Opdualag sales remain robust, particularly in the United States, where it continues to serve as a standard of care in first-line melanoma.

The Zacks Consensus Estimate and our model estimate for Opdualag sales are pegged at $295 million and $304 million, respectively.

The Zacks Consensus Estimate and our model estimate for Orencia sales are pegged at $769 million and $772 million, respectively.

The Zacks Consensus Estimate and our model estimate for Yervoy sales are pegged at $658 million and $650 million, respectively.

Reblozyl posted solid growth in both the U.S. and international markets in the last reported quarter, driven by strong growth in demand from first- and second-line MDS-associated anemia patients. The same trend has likely continued in the first quarter.

The Zacks Consensus Estimate and our model estimate for Reblozyl sales are pegged at $592 million and $602 million, respectively.

Breyanzi sales have likely benefited from strong demand growth across all its approved indications. Domestic sales reflect growth in large B-cell lymphoma and label expansion in new indications. International sales are being driven by continued strong demand across existing markets, along with incremental demand from newly launched markets.

The Zacks Consensus Estimate and our model estimate for Breyanzi sales are pegged at $373 million and $375 million, respectively.

Camzyos sales, too, have likely seen strong growth, driven by increased demand in the United States on the back of new patient starts and higher demand in newly launched markets outside the country.

The newly launched schizophrenia drug Cobenfy is off to a solid start, and sales have likely grown sequentially in the first quarter.

Increase in demand for psoriasis drug Sotyktu has likely been partially offset by higher rebates.

However, as in the previous quarters, total quarterly revenues have likely been adversely impacted by a decline in sales from the legacy portfolio, which includes Eliquis, Revlimid, Pomalyst, Sprycel and Abraxane, among others.

Generic competition for Sprycel, Revlimid, Abraxane and Pomalyst has likely pulled down revenues from this portfolio. BMY expects this segment to decline a further 12-16% in 2026.

The Zacks Consensus Estimate for Pomalyst’s first-quarter sales is pegged at $388 million and our model estimate for the same is pinned at $282 million.

Eliquis sales continue to benefit from strong global demand.

The Zacks Consensus Estimate and our model estimate for Eliquis’ first-quarter sales are pegged at $3.8 billion and $3.9 billion, respectively.

Bristol-Myers collaborated with Pfizer PFE for Eliquis in 2007. Profits and losses are shared equally worldwide, except in certain countries where Pfizer commercializes Eliquis and pays BMY a sales-based fee.

BMY expects Eliquis sales to grow 10-15% in 2026, supported by sustained global demand. Guidance includes the impact of the recent price reduction, which is expected to expand patient access while eliminating the inflation penalty. Sales are anticipated to be weighted toward the second half of the year.

Operating expenses have likely declined in the first quarter, primarily due to the company’s ongoing strategic productivity initiative.

BMY’s Price Performance and Valuation

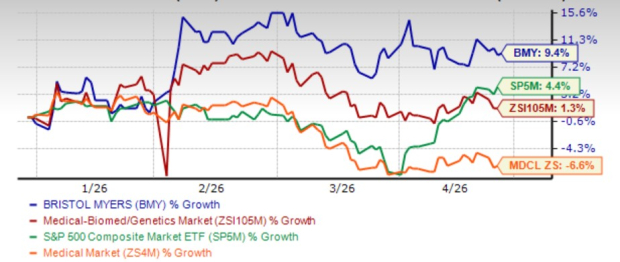

Shares of BMY have gained 9.4% year to date compared with the industry’s growth of 1.3%. The stock has also outperformed the sector and the S&P 500 in this time frame.

Image Source: Zacks Investment Research

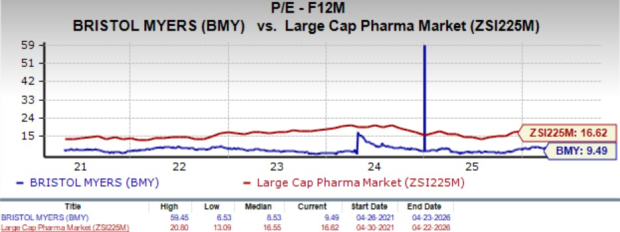

Going by the price/earnings ratio, BMY’s shares currently trade at 9.49x forward earnings, higher than its mean of 8.53x but lower than 16.55x for the large-cap pharma industry.

Image Source: Zacks Investment Research

Investment Thesis for BMY

Legacy products accounted for 45% of total sales in 2025, and the continued erosion of these revenues will weigh on overall top-line growth.

While drugs like Reblozyl, Breyanzi, Camzyos and Opdualag have enabled BMY to stabilize its revenue base, these drugs will take some time to fully offset the significant decline in legacy drug sales.

Approvals of additional new drugs and label expansions of key drugs should help BMY’s cause.

BMY’s strategic collaborations and acquisitions aimed at bolstering its pipeline are noteworthy, though they have been funded by a significant increase in debt, which remains a concern.

BMY continues to pursue strategic acquisitions and collaborations to expand its pipeline. The recent acquisition of Orbital Therapeutics adds OTX-201, a preclinical RNA CAR-T therapy designed to reprogram cells in vivo for autoimmune diseases, along with Orbital’s RNA platform.

In 2025, Bristol Myers partnered with BioNTech BNTX to co-develop the bispecific antibody pumitamig (BNT327) for solid tumors. Early phase II data in triple-negative breast cancer showed encouraging antitumor activity and manageable safety with chemotherapy. Pumitamig targets PD-L1 and VEGF-A, a dual pathway seen as a promising oncology approach.

The company is also making steady progress on its cost optimization program, targeting $2 billion in annualized savings by 2027, with approximately $1 billion already realized in 2025. This positions operating expenses to trend lower, supporting margin expansion beginning in 2026.

Stay Invested in BMY Stock

BMY is one of the largest biotechs and such large biotech companies are generally considered safe havens for investors interested in this sector.

Regardless of how the first-quarter results turn out, we recommend prospective investors to adopt a wait-and-watch approach before turning constructive on the stock. For existing shareholders, however, remaining invested appears prudent, supported by the company’s attractive dividend yield of 4.29%, which provides a compelling incentive to hold the shares.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bristol Myers Squibb Company (BMY): Free Stock Analysis Report

Pfizer Inc. (PFE): Free Stock Analysis Report

BioNTech SE Sponsored ADR (BNTX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).