Domino's Pizza Inc. (DPZ) stock dropped over 8% on Monday, April 27, after its pre-market Q1 earnings release. The market was disappointed with lower-than-expected revenue. But its free cash flow margin was strong. DPZ stock could still be undervalued.

DPZ fell over 8.8% to $335.30, a new three- and six-month low. This just seems overdone, given the company's strong free cash flow (FCF) and FCF margins.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

DPZ stock - last 6 months - Barchart - April 27

DPZ stock - last 6 months - Barchart - April 27 However, that does not mean DPZ cannot tank further. However, this provides a good buying point for value investors, as well as short-put plays.

What DPZ Stock Could Be Worth

I discussed the company's pre-release earnings and valuation in an April 24 Barchart article, “Domino's Pizza Stock Could Be Cheap Ahead of Earnings Next Week.”

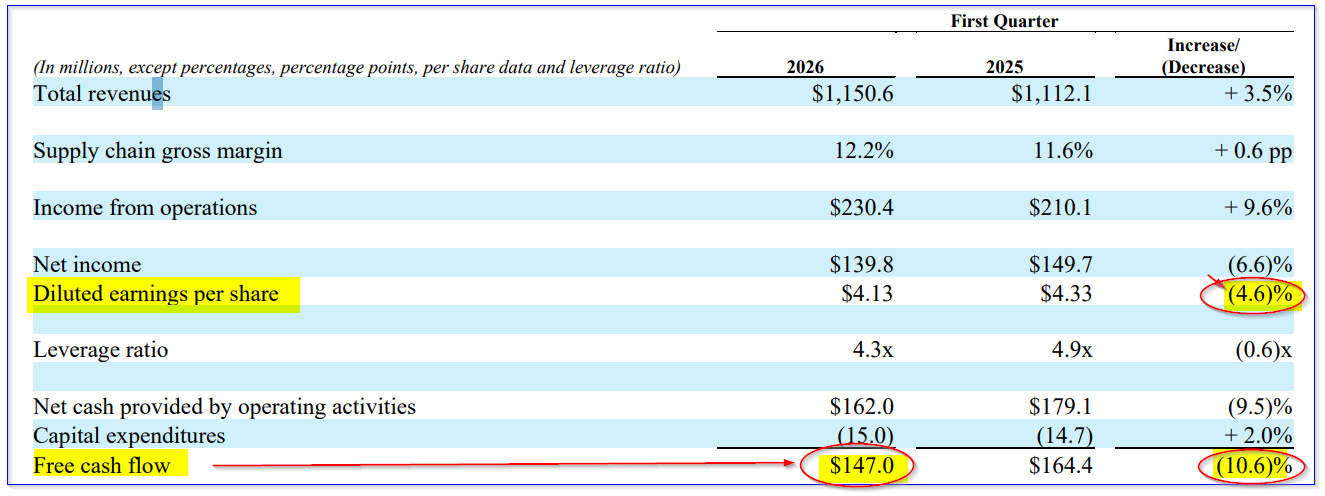

Revenue came in at $1.15 billion, but analysts were expecting slightly more, according to Seeking Alpha. However, it still represented a 3.46% YoY growth rate.

In addition, income from operations was up 9.6% YoY to $230.4 million. However, diluted earnings per share (EPS) were down 4.6%.

Moreover, free cash flow (FCF) was off by 10.6%. These last 2 points could account for why the market was so disappointed.

Domino's Pizza Q1 Earnings release - April 27, 2026

Domino's Pizza Q1 Earnings release - April 27, 2026 But, let's look closer. First, free cash flow (FCF) margin is still very strong. It came in at 12.77% (i.e., $147m / $1,150.6m).

That was lower than last year's Q1 14.78% FCF margin, according to Stock Analysis, but higher than the Q4 figure of 11.45%.

Next, remember that I wrote in Friday's Barchart article that as long as Domino's could come in with a 13% FCF margin, analysts might be willing to raise their targets.

This was based on last year's 13.6% average FCF margin performance.

Third, over the trailing 12 months, including seasonal effects, Domino's FCF margin has risen, according to Stock Analysis data.

Q1 2026 TTM FCF margin ……….. 13.14%

Q4 2025 TTM FCF margin ……….. 13.59%

Q1 2025 TTM FCF margin …………12.11%

That allows us to forecast FCF going forward at least at a 13% FCF margin rate, as I did in my April 24 article.

Forecasting FCF

For example, analysts now project 2026 revenue will be $5.23 billion, and for 2027 it will rise to $5.44 billion.

That means over the next 12 months (i.e., 3/4x the 2026 est + 1/4x the 2027 est.) revenue will exceed $5.28 billion :

(0.75 x $5.23b) + (0.25 x $5.44b) = $3.9225b + $1.36b = $5.2825 billion NTM revenue

Now, assuming Domino's can continue to make a 13.6% FCF margin, as it did in 2025, FCF will rise to

$5.2825 billion NTM rev. x 0.1359 = $718 million est. NTM FCF

That would be 6.9% over the 671.5 million in FCF it made in 2025. This could keep its valuation strong.

Price Targets for DPZ Stock

Historically, DPZ stock has traded at a 24.33x cash flow multiple, according to Morningstar figures. That is the same as a 4.1% cash flow yield (i.e., 1/24.33).

However, that is for price/cash flow from operations (CFFO), not P/FCF. After deducting capex spending, it likely works out to a 20x multiple or a 5.0% FCF yield (i.e., 1/05).

Therefore, let's use that 5% FCF yield metric to value the NTM FCF:

$718m FCF est. / 0.05 = $14,360m = $14.36 billion market value

That is still well over today's market cap (Yahoo! Finance) of $11.153 billion, i.e., a 28.75% upside:

$14.36b / $11.153b = 1.2875

So, DPZ's price target is 28.75% higher:

$335.30 x 1.2875 = $431.70 per share price target (PT).

That's only slightly lower than my prior PT of $434.84.

However, keep in mind that this assumes management can continue to generate strong FCF margins, equal to last year. Other analysts agree. Yahoo! Finance reports that 33 analysts have an average PT of $458.29, and Barchart's mean survey PT is $465.00.

Moreover, AnaChart, which tracks recent analyst recommendations, shows that 24 analysts have an average PT of $483.25.

So, DPZ's 8.8% drop today seems well overdone. However, there is no guarantee it won't keep falling. One way to play it is to short out-of-the-money (OTM) puts.

Shorting OTM DPZ Puts

I discussed shorting the $350.00 put expiring May 15 in my April 24 article. At the time, it was 6% lower than the spot price (i.e., out-of-the-money), but now it's 4.38% in-the-money.

That means the investor who shorted this put may end up with an unrealized loss if their collateral is assigned. The breakeven point was $344.05 after receiving the $5.95 income.

However, after doubling down at Monday's mid-point price of $17.55, the net breakeven will be $326.50 (i.e., $350-$23.50 income received), or 2.62% below Monday's close.

That's why it makes sense to hold on and possibly double down here. That way, the investor can increase their yield and potentially dramatically lower their net buy-in cost.

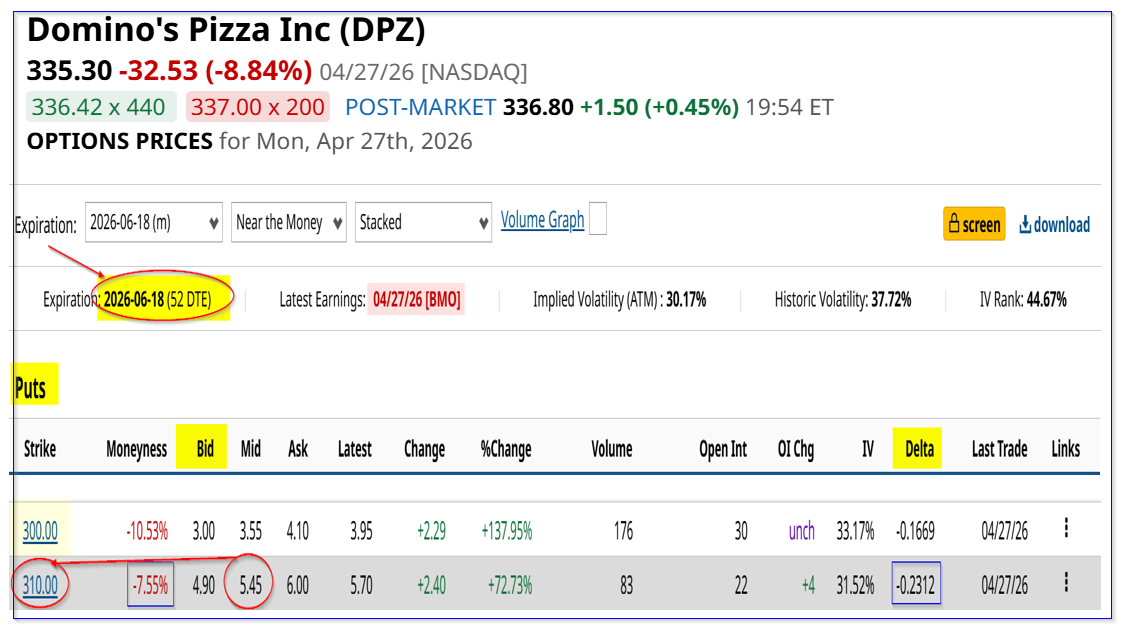

However, for new DPZ investors, look at the June 18 expiry period, 52 days from now. It shows that the $310 put strike price has a midpoint premium of $5.45.

DPZ puts expiring June 18 - Barchart - As of April 27, 2026

DPZ puts expiring June 18 - Barchart - As of April 27, 2026 That provides a short-seller a 1.758% yield over the next month and a half (i.e., $5.45/$310). That strike price is over 7.5% lower than today's close, but the breakeven point would be:

$310 - $5.45 = $304.55 breakeven, or -9.17% lower

The bottom line is that DPZ stock looks too cheap here. One way to play it is to generate income by shorting OTM puts.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Domino's Pizza Stock Drop May Be Overdone, Based on Its Strong FCF Margins AMD Earnings Bull Put Spread has a High Probability of Success "Sell in May" Could Be Bad News for the Kiwi Dollar Micron Stock Keeps Soaring, as Investors Make Unusually Heavy MU Option Trades