Amazon.com, Inc. (AMZN), headquartered in Seattle, Washington, is the world's largest online retailer and marketplace. The company engages in the retail sale of consumer products, advertising, and subscription services through online and physical stores. With a market cap of $2.8 trillion, its products include books, music, computers, electronics, and numerous other products. Amazon offers personalized shopping services, web-based credit card payment, and direct shipping to customers. It also operates a cloud platform offering services globally.

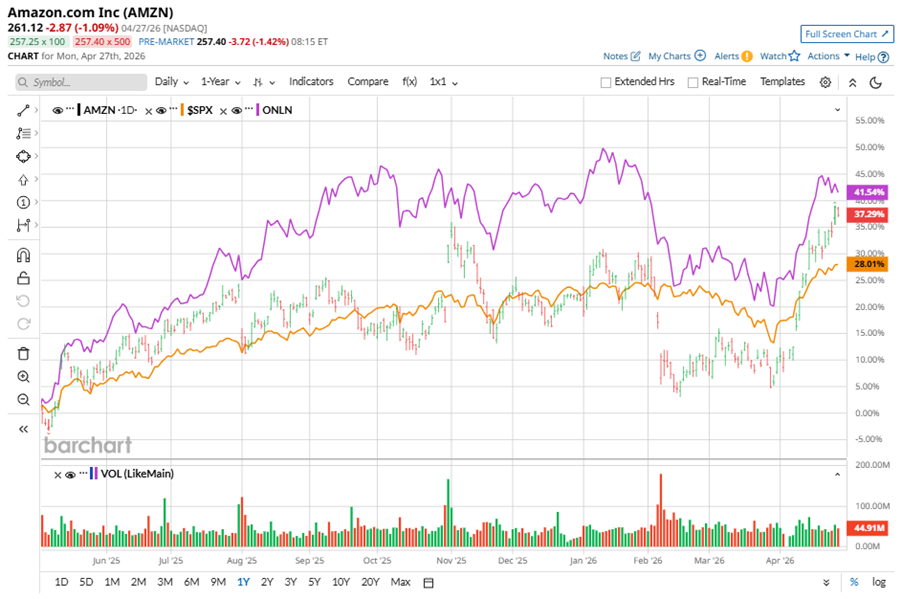

Shares of this online retail behemoth have outperformed the broader market over the past year. AMZN has gained 38.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 29.8%. In 2026, AMZN stock is up 13.1%, surpassing the SPX’s 4.8% rise on a YTD basis.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Narrowing the focus, AMZN has lagged behind the ProShares Online Retail ETF (ONLN). The exchange-traded fund has gained about 42.9% over the past year. However, the stock’s double-digit returns on a YTD basis outshine the ETF’s 1.5% gains over the same time frame.

www.barchart.com

www.barchart.com Amazon’s outperformance is driven by strength across retail, AWS, and ads. Retail keeps growing on pricing, selection, and faster delivery from its regionalized fulfillment network, which also cuts costs. Meanwhile, AWS hit $35.6 billion in Q4 revenue, with a $142 billion run rate and $244 billion backlog, as AI adoption fuels cloud demand. Advertising grew to $21.3 billion, benefiting from high-margin sponsored placements and streaming. Meta Platforms, Inc.’s (META) multi-billion deal to use Graviton chips for AI signals strong AWS demand, while analysts raised price targets ahead of earnings. Amazon also plans an $11.6 billion Globalstar, Inc. (GSAT) buy to expand its Amazon Leo satellite network with direct-to-device service by 2028, acquired Fauna Robotics for consumer-facing humanoids, and is building a “Transformer” phone with Alexa+ to push AI services.

For fiscal 2026, ending in December, analysts expect AMZN’s EPS to grow 7.5% to $7.71 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

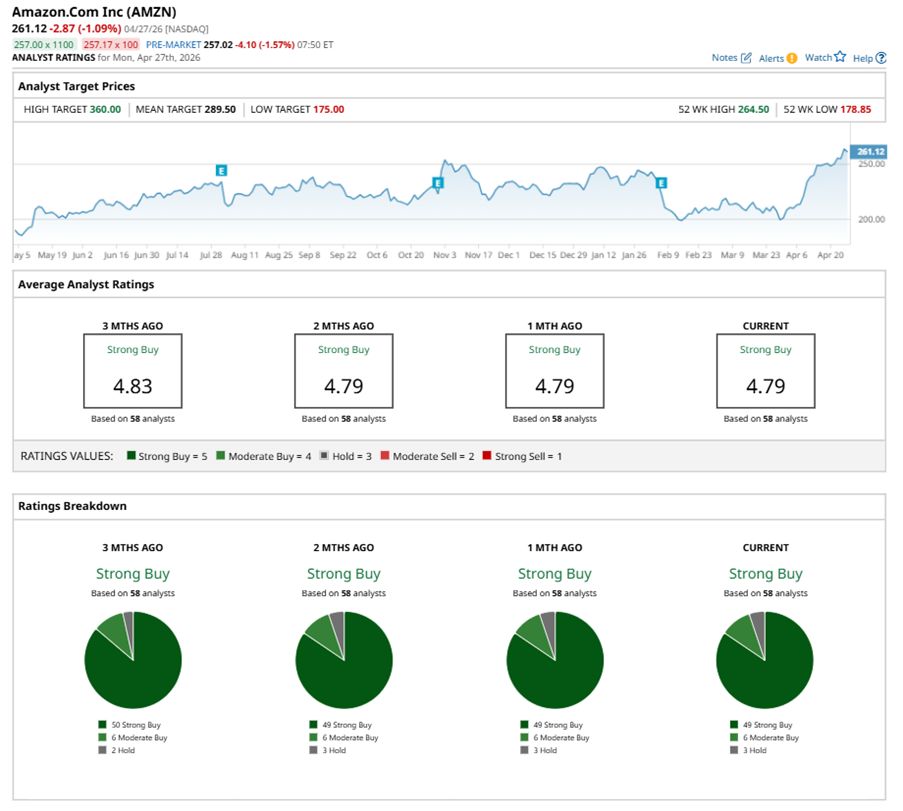

Among the 58 analysts covering AMZN stock, the consensus is a “Strong Buy.” That’s based on 49 “Strong Buy” ratings, six “Moderate Buys,” and three “Holds.”

www.barchart.com

www.barchart.com This configuration is less bullish than three months ago, with 50 analysts suggesting a “Strong Buy.”

On Apr. 27, Monness analyst Brian White maintained a “Buy” rating on AMZN and set a price target of $280, implying a potential upside of 7.2% from current levels.

The mean price target of $289.50 represents a 10.9% premium to AMZN’s current price levels. The Street-high price target of $360 suggests an ambitious upside potential of 37.9%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Kevin Warsh Has Been Labeled a ‘Sock Puppet.’ A Potential Federal Reserve ‘Shadow Chair’ Is a Much Greater Threat for Investors. Follow the Trend Seeker: Beaten-Down SelectQuote Stock Surges 54% in 1 Month as Barchart’s Data Signals ‘Buy’ AMD Stock Slides on Analyst Downgrade. What to Know. Is Qualcomm Stock a Buy Amid Reports of OpenAI Partnership?