Realty Income O stock has been acting like a classic income name in a jumpy market, not immune to daily swings, but still supported by its dividend identity and defensive lease profile. The stock recently traded around $64, and so far in the year has gained 13.4%.

While Realty Income has underperformed the Zacks REIT and Equity Trust - Retail industry, it has rallied more than its peers like Agree Realty Corporation ADC and Essential Properties Realty Trust, Inc. EPRT, as well as the S&P 500 Composite.

This move has come while investors continue to deal with mixed market signals. Elevated interest rates, oil-price worries and geopolitical headlines have kept volatility alive, even though corporate earnings have helped the broader market stay resilient. For REITs, the rate backdrop matters because higher yields can pressure valuations and raise financing costs.

So, should investors buy, hold or sell O now? To answer this, let’s weigh the positives and concerns, starting with its steady income record, portfolio scale, funding flexibility and growth plans, while also recognizing that the stock is not risk-free in a volatile market.

Image Source: Zacks Investment Research

The Dividend Story Still Matters for Realty Income

Realty Income’s biggest appeal remains its monthly dividend record. In April 2026, the company declared its 670th consecutive monthly common stock dividend of 27.05 cents per share, or $3.246 annualized. It also noted that it has increased the dividend for more than 31 consecutive years, keeping its Dividend Aristocrat status.

This record does not make the stock a guaranteed winner, but it does give income-focused investors a clear reason to stay interested. The company also raised its dividend in March, marking its 134th increase since listing on the NYSE in 1994.

Scale and Occupancy Add Stability to Realty Income

The company’s portfolio gives it another layer of support. As of Dec. 31, 2025, Realty Income owned or held interests in 15,511 properties leased to 1,761 clients across 92 industries. Occupancy stood at 98.9%, up from 98.7% as of both Sept. 30, 2025 and Dec. 31, 2024.

This broad base helps reduce reliance on any single tenant or industry. The company also reported a weighted average remaining lease term of about 8.8 years, which supports rental visibility. This matters in volatile markets, where investors often prefer businesses with more predictable cash flows.

Growth Is Still Visible for Realty Income

Realty Income is not just relying on its existing portfolio. In 2025, it invested $6.3 billion, with a pro-rata share of $6.2 billion, at an initial weighted average cash yield of 7.3%. It also guided for about $8 billion of investment volume in 2026 and projected AFFO per share of $4.38-$4.42.

The company’s leasing results were also encouraging. For full-year 2025, re-leased units generated a rent recapture rate of 103.9%, while fourth-quarter re-leasing came in at 104.9%.

Partnerships Broaden the Funding Base of Realty Income

Another positive is Realty Income’s push to diversify capital sources. Its partnership with GIC includes more than $1.5 billion of combined commitments for a programmatic joint venture, a $200 million Mexico industrial portfolio commitment and GIC’s role as a cornerstone investor in Realty Income’s U.S. Core Plus fund.

The Apollo partnership adds another angle. Apollo-managed funds plan to invest $1 billion for a 49% interest in a portfolio of roughly 500 U.S. retail assets, with Realty Income continuing to manage the properties. Management said that the structure supports its private capital initiative and reduces dependence on public equity markets.

Rate Sensitivity, Macro Volatility Remain Concerns for O

Realty Income’s business remains sensitive to interest-rate movements and broader macro volatility. When rates stay elevated, REITs can face pressure because borrowing costs rise, property valuations may come under strain and income investors may compare dividend yields more closely with bond yields. This does not weaken Realty Income’s operating profile, but it can limit near-term upside for the stock.

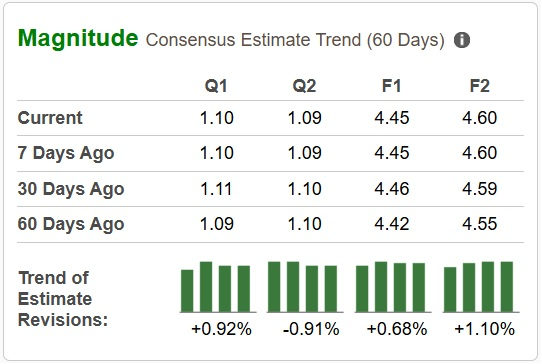

O's Estimate Revisions and Valuation

Estimate revisions reflect a somewhat mixed trend. Over the past 30 days, estimates for O’s 2026 FFO per share have been tweaked marginally southward to $4.45, while estimates for 2027 have been revised upward to $4.60, indicating a balanced view of growth and cost pressures.

Image Source: Zacks Investment Research

Valuation-wise, Realty Income stock is trading at a forward 12-month price-to-FFO of 14.07X, below the retail REIT industry average of 16.83X but ahead of its three-year median. O stock is also currently trading at a reasonable discount compared with its industry peers, Agree Realty Corporation and Essential Properties Realty Trust. However, this valuation disparity might not be as favorable as it seems. Agree Realty is trading at a forward 12-month price-to-FFO of 16.52X, while Essential Properties Realty Trust is trading at 14.96X.

However, the Value Score of D suggests that Realty Income may not be a bargain at current levels. Still, the company’s strategic investments, consistent dividend growth, underpinned by predictable rental income, keep it appealing for long-term income-oriented investors.

Image Source: Zacks Investment Research

Holding the Stock Looks Like the Sensible Call for O

Realty Income remains a high-quality REIT for investors who value monthly income, scale and steady operating execution. Its dividend history, high occupancy, active investment pipeline and private-capital partnerships support the long-term story. At the same time, the stock has already recovered meaningfully, and the interest-rate backdrop can still create pressure on valuation and financing costs.

For new investors, the current price may not offer a wide margin of safety. For existing shareholders, the business looks sound enough to keep. Given this balance, as well as estimate revisions and valuation, the most reasonable approach is to hold the stock amid market volatility.

At present, Realty Income carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Realty Income Corporation (O): Free Stock Analysis Report

Agree Realty Corporation (ADC): Free Stock Analysis Report

Essential Properties Realty Trust, Inc. (EPRT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).