Valued at $30.6 billion by market cap, VICI Properties Inc. (VICI) is a leading real estate investment trust that owns a portfolio of experiential properties, primarily casinos, resorts, and entertainment venues. The company leases these assets to major operators under long-term agreements, positioning itself as a landlord rather than an operator. Its portfolio is heavily concentrated in high-profile gaming destinations, including Caesars Palace Las Vegas, MGM Grand and the Venetian Resort Las Vegas, three of the most iconic entertainment facilities on the Las Vegas Strip.

Shares of this diversified commercial REIT have underperformed the broader market over the past year. VICI has declined 11.4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 26.6%. In 2026, VICI stock is down marginally, compared to the SPX’s 5.2% rise on a YTD basis.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Narrowing the focus, VICI has also trailed the State Street Real Estate Select Sector SPDR Fund (XLRE). The exchange-traded fund has surged 5.1% over the past year. Moreover, the ETF’s 9.2% returns on a YTD basis outshine the stock’s marginal dip over the same time frame.

www.barchart.com

www.barchart.com On Apr. 29, VICI Properties reported results for the first quarter ended March 31, 2026, delivering steady, contract-driven growth. Total revenues rose 3.5% year over year to approximately $1.02 billion, supported by built-in rent escalations and contributions from prior acquisitions. The portfolio remained fully occupied, with all tenants meeting lease obligations, underscoring the resilience of its triple-net lease model.

Core cash flow performance was solid, with Adjusted Funds From Operations (AFFO) of $650.9 million and $0.61 per share, up 5.7% and 4.5% year over year, respectively. The results reinforced the company’s consistent, income-focused profile, and the stock responded positively, gaining 2.1% in the following trading session.

For the current fiscal year, ending in December 2026, analysts expect VICI’s FFO to grow 3.4% to $2.46 per share on a diluted basis. The company’s earnings surprise history is impressive. It beat or matched the consensus estimates in each of the last four quarters.

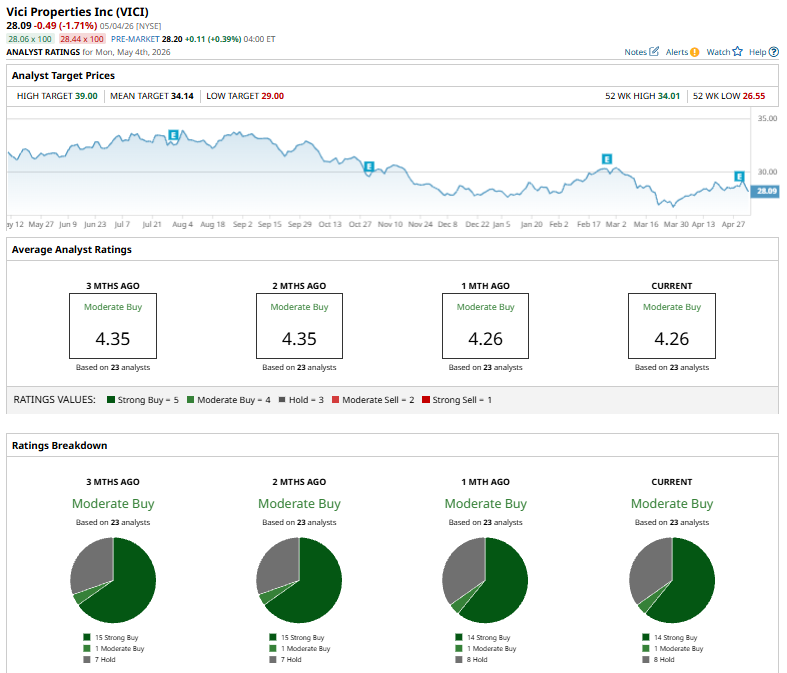

Among the 23 analysts covering VICI stock, the consensus is a “Moderate Buy.” That’s based on 14 “Strong Buy” ratings, one “Moderate Buy,” and eight “Holds.”

www.barchart.com

www.barchart.com This configuration is bearish than two months ago, with 15 analysts suggesting a “Strong Buy.”

On Apr. 21, Barclays raised its price target on VICI Properties to $34 from $33 while maintaining an “Overweight” rating. The revision comes as part of its Q1 outlook for the net lease REIT sector.

The mean price target of $34.14 represents a 21.5% premium to VICI’s current price levels. The Street-high price target of $39 suggests an upside potential of 38.8%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Reddit Stock Is an Earnings Season Winner. Investors Thank Advertising Revenue for That. DDOG Earnings Play Has a HUGE Return Potential Stock Index Futures Climb as U.S.-Iran Ceasefire Holds, JOLTs Report and Earnings in Focus This Blue-Chip Dividend Stock Is Becoming an AI Star