Watts Water Technologies, Inc. WTS reported first-quarter 2026 adjusted earnings per share (EPS) of $3.04 compared with $2.37 in the prior-year quarter. The bottom line beat the Zacks Consensus Estimate by 11.8%.

The company’s quarterly net sales increased 21% year over year to $677.3 million. The top line beat the Zacks Consensus Estimate by 7.2%. Organic sales were up 12% year over year due to favorable prices and higher volumes supported by strong growth in the data center market.

Management highlighted that the company delivered a strong start to 2026, supported by organic growth across all regions and record first-quarter net sales, operating income, operating margin and EPS, reflecting disciplined execution and continued focus on delivering value to customers. The company also emphasized that it is actively navigating geopolitical and trade-related uncertainties while continuing to invest in higher-growth opportunities such as data centers and digital solutions.

In addition, management noted that productivity and automation initiatives under the One Watts Performance System are helping drive efficiency and margin performance. Despite the solid start to the year, the company maintained its full-year 2026 outlook given the dynamic macroeconomic environment.

Supported by a strong balance sheet and healthy cash flow generation, management remains focused on disciplined capital allocation and creating sustainable long-term shareholder value.

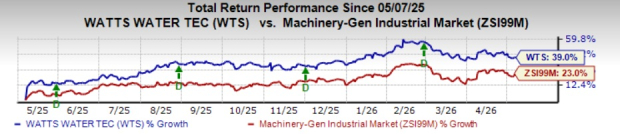

Shares of the company have gained 39% in the past year compared with the Zacks Manufacturing - General Industrial industry’s growth of 23%.

Image Source: Zacks Investment Research

WTS’ Segment Results

Americas: Net sales increased 23% year over year to $515 million on a reported basis and rose 16% organically, primarily driven by favorable pricing and incremental volumes supported by strong data center demand. Acquisitions contributed $31 million in incremental sales, accounting for 7% of reported growth. Segment margin expanded 80 basis points (bps) as benefits from price realization, productivity improvements and volume leverage more than offset the impacts of inflation, tariffs and acquisition-related dilution.

Europe: Net sales increased 12% year over year to $121 million on a reported basis and grew 1% organically. Reported sales growth benefited from favorable foreign exchange, which contributed 11% to reported results. Organic sales growth was primarily driven by favorable pricing, which offset a modest decline in volumes. Segment margin contracted 20 bps as gains from price realization, productivity initiatives and restructuring actions were more than offset by inflationary pressures and volume deleverage.

APMEA: Net sales increased 29% year over year to $41 million on a reported basis and rose 3% organically, driven by growth in China, Australia and New Zealand, partially offset by weakness in the Middle East. Acquisitions contributed $6 million, or 19%, to reported sales growth, while favorable foreign exchange added 7%. Segment margin expanded 120 bps, supported by trade sales volume leverage, productivity gains and acquisition accretion, which more than offset inflation and affiliate volume deleverage.

WTS’ Other Details

Gross profit increased 19.7% year over year to $326.1 million. Selling, general and administrative expenses rose 15.2% to $192.9 million. Operating income was $133 million, up 51.7% year over year. Adjusted operating income was $135.9 million, up 28.1% year over year.

Operating margin expanded 390 bps to 19.6%. The adjusted operating margin was 20.1%, up 110 bps year over year. Margin performance was driven by favorable pricing, productivity improvements and volume leverage, which more than offset the impacts of inflation, investments, tariffs and acquisition-related dilution. Operating margin also benefited from lower restructuring charges, partially offset by higher acquisition-related expenses.

WTS’ Cash Flow & Liquidity

For the first quarter ended March 29, 2026, Watts Water generated $17.9 million of cash from operating activities compared with $55.2 million in the prior-year period.

For the first quarter, free cash flow was $6.6 million compared with $45.6 million a year ago.

Free cash flow declined primarily due to higher capital expenditures and elevated working capital levels, which more than offset the benefit of increased net income. The rise in working capital was driven by higher accounts receivable linked to stronger net sales, increased inventory levels resulting from incremental tariffs and strategic inventory investments to support anticipated end-market demand, as well as higher annual customer rebates tied to sales growth and payment timing. Management expects free cash flow to improve sequentially through 2026 as working capital is gradually monetized in line with normal business seasonality.

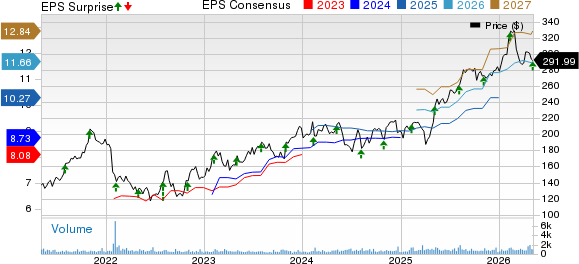

Watts Water Technologies, Inc. Price, Consensus and EPS Surprise

Watts Water Technologies, Inc. price-consensus-eps-surprise-chart | Watts Water Technologies, Inc. Quote

On May 4, 2026, the company announced a 21% increase in its quarterly dividend, raising the payout from 52 cents per share to 63 cents, effective June 2026.

During the first quarter of 2026, the company also repurchased nearly 13,000 shares for approximately $3.8 million. As of quarter-end, about $125 million remained available under the share repurchase program authorized in 2023, which has no expiration date.

As of March 29, 2026, the company had $374.7 million in cash and cash equivalents with $197.8 million of long-term debt compared with the respective figures of $405.5 million and $197.7 million as of Dec 31, 2025.

WTS’ Guidance

For 2026, the company maintained its prior outlook and continues to expect reported sales growth in the range of 8% to 12%, with organic sales growth projected between 2% and 6%.

The company expects adjusted EBITDA margin to be between 21.5% and 22.1%, representing a change of down 40 bps to up 20 bps year over year.

The company anticipates operating margin to be between 18.8% and 19.4%, reflecting an expansion of 40-100 bps, while adjusted operating margin is forecast at 19.1% to 19.7%, implying a decline of 50 bps to an increase of 10 bps.

For the second quarter of 2026, the company expects reported sales growth of 10% to 14% and organic sales growth of 4% to 8%. Adjusted EBITDA margin is projected between 22.3% and 22.9%, while adjusted operating margin is expected in the range of 20% to 20.6%.

WTS’ Zacks Rank

Watts Water currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Recent Performance of Peers in the Same Space

Flex Ltd. FLEX reported fourth-quarter fiscal 2026 adjusted EPS of 93 cents, which surpassed the Zacks Consensus Estimate by 8.1%. The bottom line compared favorably with 73 cents posted in the prior-year quarter.

Revenues increased 17% year over year to $7.5 billion. It beat the consensus mark by 8.1%. The growth was primarily driven by strong momentum across all three segments, with Cloud and Power Infrastructure emerging as the standout performer.

Fortive Corporation FTV reported first-quarter 2026 adjusted EPS of 70 cents from continuing operations, which surpassed the Zacks Consensus Estimate of 64 cents. The bottom line increased 25.4% year over year.

Revenues increased 7.7% year over year to $1069.4 million. The top line beat the Zacks Consensus Estimate by 3.8%. Core revenues jumped 5.3%.

Sensata Technologies Holding plc ST reported first-quarter 2026 adjusted EPS of 86 cents, up from 78 cents a year ago. The bottom line beat the Zacks Consensus Estimate by 2.4%.

Revenues for the quarter reached $934.8 million, up 2.6% from a year ago. The figure came near to the upper end of management’s expectations ($917-$937 million) and beat the consensus estimate by 0.7%. Strength Aerospace, Defense and Commercial Equipment segments drove the top-line performance.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Sensata Technologies Holding N.V. (ST): Free Stock Analysis Report

Flex Ltd. (FLEX): Free Stock Analysis Report

Watts Water Technologies, Inc. (WTS): Free Stock Analysis Report

Fortive Corporation (FTV): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).