Uber Technologies (UBER) offers a popular ride-hailing app. But very few investors realize that the company has evolved into a global transportation and delivery giant spanning rides, food delivery, grocery, advertising, and subscription services.

UBER stock is down 9% year-to-date (YTD). Yet Wall Street is becoming increasing bullish following the firm's first-quarter earnings report, with several analysts raising their price targets between $105 and $119, pointing to accelerating growth in rides, delivery, advertising, and subscriptions. Analysts believe shares could have more than 50% potential upside from current levels.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Here are three reasons for the recent price upgrades, and why investors should pay attention to Uber.

www.barchart.com

www.barchart.com Reason #1: Uber’s Core Business Is Still Running Hot

Uber released it Q1 report on May 6. The strong quarter prompted many analysts to upgrade their price targets. In fact, the high price estimate of $150 for UBER stock, assigned by Evercore ISI, suggests the stock can climb as high as 100% over the next 12 months. One of the biggest reasons analysts remain bullish is that Uber’s core business remains strong across multiple segments. CEO Dara Khosrowshahi called Q1 an “exceptional start to 2026” despite difficult conditions that included weather disruptions and geopolitical uncertainty.

Gross bookings climbed 25% year-over-year (YOY) to $53.7 billion, driving a 14% increase in total revenue to $13.2 billion. Delivery revenue grew 34%, led by grocery and retail categories along with strong customer retention. Even Uber Freight, which has struggled through a weak freight environment over the last two years, has resumed growing for the first time in nearly two years.

The company now operates across 70 countries. Currently, Uber has more than 50 million Uber One members and 10 million drivers and couriers globally, highlighting the scale of its platform. According to management, Uber One customers spend three times more than regular customers. In fact, the membership program now accounts for more than half of Uber’s bookings while continuing to grow 50% YOY.

Uber’s unique and smart strategy of expanding beyond simple ride-sharing has impressed Wall Street. The company has launched travel-related services, including hotel bookings integrated directly into the Uber app through its partnership with Expedia (EXPE). Management believes travel could become a major long-term opportunity because airports already account for roughly 15% of Uber’s mobility gross bookings. The company is also seeing strong momentum in suburban and less densely populated markets.

Reason #2: The Profit Machine Is Finally Kicking In

The second reason for enthusiam around UBER stock is Uber’s improving profitability. Most growing businesses struggle with generating profits while scaling, but that doesn’t seem to be an issue for Uber. Adjusted earnings climbed 44% YOY to $0.72 per share. Management credited strict cost controls, operating leverage, and lower insurance costs to this growth.

Uber also generated $2.3 billion in free cash flow and returned $3 billion to shareholders through stock buybacks during the quarter. Additionally, the company expects to generate “hundreds of millions of dollars” in insurance savings during 2026, thanks to improvements in its insurance strategy, policy changes, and technology upgrades.

Reason #3: Uber Wants to Own Everyday Spending

Uber’s long-term position in several enormous future markets, such as AI-powered commerce and autonomous driving, is promising. Uber is building what management calls an “everyday utility” platform that connects transportation, food delivery, grocery shopping, travel, and logistics in a single ecosystem. This will increase cross-platform engagement, resulting in growth across all of its businesses.

Autonomous vehicles could eventually become a trillion-dollar market opportunity, and the company’s large existing network gives it a major competitive advantage. Uber now has more than 30 autonomous vehicle partners across mobility and delivery, while autonomous mobility trips increased more than 10 times YOY. The firm continues to expand partnerships with names like Zoox, Nuro, Alphabet's (GOOGL) Waymo, Lucid (LCID), Nvidia (NVDA), Baidu (BIDU), and more. Uber expects to have autonomous operations in up to 15 cities by the end of 2026.

Why Uber Still Looks Like a Long-Term Winner

With expanding profit margins, multiple growth engines, massive AI opportunities, and early leadership in autonomous transportation, Uber looks like the type of business that could keep thriving for years to come. Accordingly, the current dip in UBER stock might be a great buying opportunity.

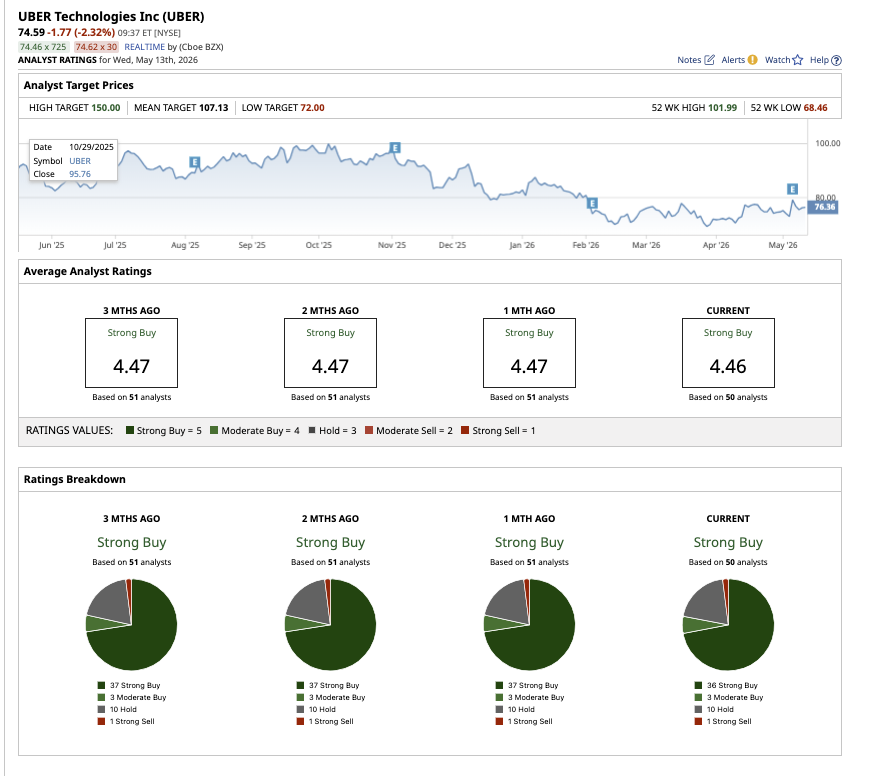

Overall, UBER stock holds a consensus “Strong Buy” rating. Of the 50 analysts covering shares, 37 have a “Strong Buy” recommendation, three have a “Moderate Buy” rating, nine suggest a “Hold” rating, and one analyst has a “Strong Sell.” Based on the average price target of $106.80, UBER stock has potential upside of 43% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wix.com Stock Is the Latest Victim of the AI Trade as Shares Plunge Nearly 30% Uber Stock: 3 Reasons Why Analysts See Over 50% Upside Potential 3 Dividend Aristocrats Under $100 to Buy and Hold Forever Magnum Ice Cream Company Surges on Takeover Speculation. What to Know.