The AI boom stopped being a software story the moment Big Tech started pouring concrete. Amazon (AMZN), Microsoft (MSFT), Alphabet (GOOG) (GOOGL), and Meta (META) are now expected to spend as much as $725 billion combined on capital expenditures this year. Much of that spending is flowing directly into AI infrastructure like data centers, networking hardware, advanced chips, and the materials needed to build them.

That raises an important question for investors. If Nvidia (NVDA) became the face of AI, who supplies the companies supplying Nvidia?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

One answer may be AXT (AXTI) .

The semiconductor materials maker quietly became one of the market’s top-performing AI-adjacent stocks, turning a beaten-down share price into an 8,436.55% one-year return at its peak. Although the move looks wild on the surface, the business behind it is more grounded than many investors realize.

barchart.com

barchart.com AI Data Centers Need More Than GPUs

AI servers require compound semiconductors to move data rapidly while minimizing heat and power loss. That’s where AXT comes in. The company manufactures substrates made from gallium arsenide, indium phosphide, and germanium, all of which are materials used in fiber-optic networking, wireless infrastructure, and high-performance chips.

Essentially, AI data centers cannot function efficiently without fast optical connections between racks of GPUs. AXT helps make those connections possible. Indium phosphide substrates are increasingly used in optical networking products supporting cloud computing and AI workloads.

The timing could hardly have been better. Meta Platforms alone expects 2026 capital expenditures up to $135 billion. Microsoft remains on pace to spend $190 billion this fiscal year building AI-enabled data centers. Alphabet raised planned capex to roughly $185 billion, and Amazon will hit $200 billion.

Regardless of the lens that investors use, AI infrastructure spending is no longer experimental. It is becoming mandatory.

AXT’s Numbers Finally Started Moving

For years, AXT looked like a forgotten small-cap semiconductor supplier. Revenue drifted lower after the pandemic-era electronics slowdown while larger competitors captured investor attention. Then demand recovered.

Revenue rose 38.6% year-over-year (YOY) to $26.9 million in the first quarter. More importantly, backlog reached a record $100 million, signaling stronger future demand. Gross margin also improved to 29.6% from 20.9% a year earlier.

The numbers speak loudly. The market cap is $7.52 billion; 2025 revenue was $88.3 million; GAAP gross margin came in at 12.7%; Long-term debt was $0, a statistic that matters in a balance sheet. Many speculative AI plays funded expansion with expensive borrowing or repeated share offerings. AXT avoided both problems.

Surprisingly, the stock’s rise also reflected scarcity. Investors searching for smaller AI infrastructure names found relatively few public companies directly tied to optical semiconductor materials. That pushed fresh money toward niche suppliers like AXT.

Nevertheless, risk remain. For example, AXT still depends heavily on cyclical semiconductor demand. Revenue remains tiny compared to larger suppliers like Coherent (COHR) or Lumentum Holdings (LITE). And trade tensions with China are a concern because AXT maintains manufacturing operations there.

Even so, the company no longer looks like a forgotten micro-cap drifting through the semiconductor industry.

What Analysts Think About AXTI

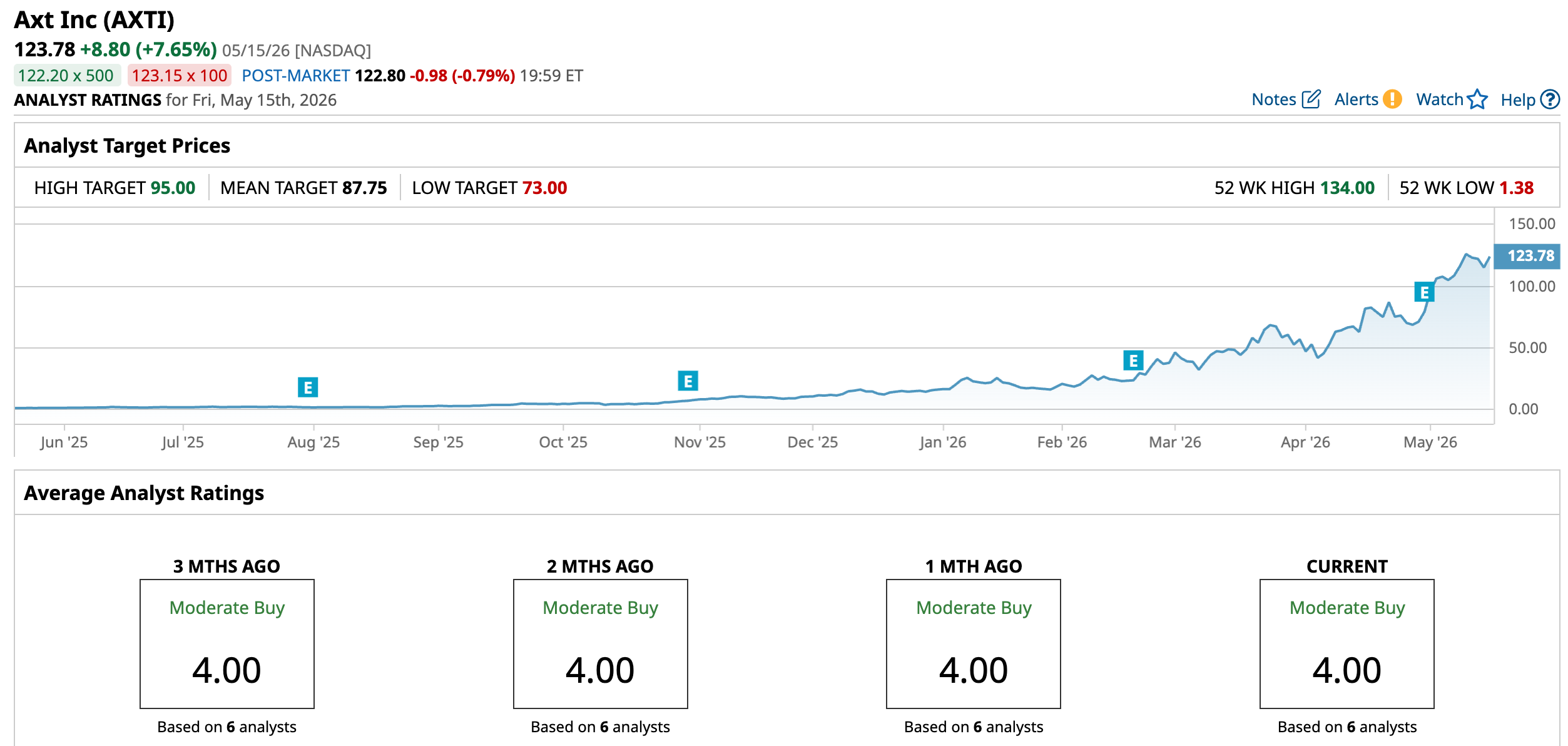

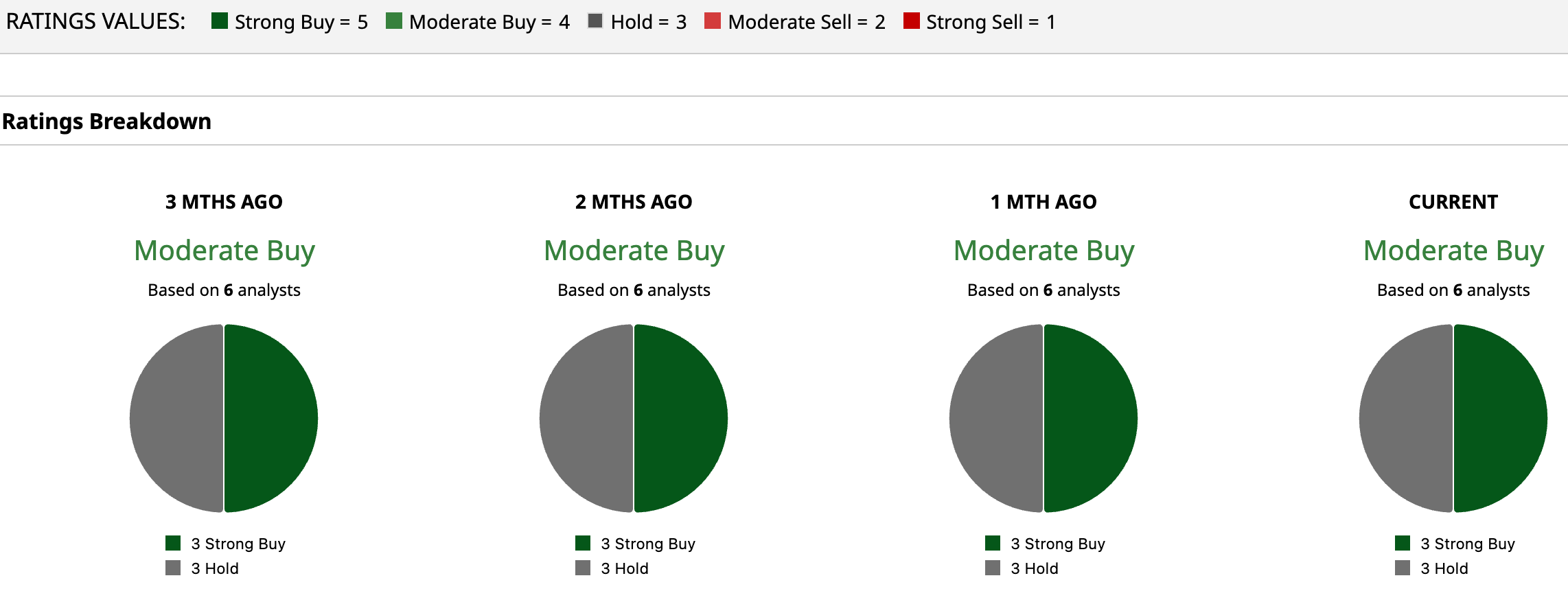

Wall Street still approaches AXT cautiously, though sentiment has improved alongside the AI infrastructure buildout.

Analysts currently maintain a consensus “Moderate Buy” rating on the stock. The mean price target sits near $87.75 per share, a solid 29% downside from its current price, and the Street-high target of $95 shows a 23.25 downside.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com That range suggests analysts believe its valuation has caught up to and is exceeding the AI-related networking demand. But that could change if it keeps accelerating. It also signals Wall Street expects volatility since small-cap semiconductor suppliers rarely move in straight lines.

In any case, analysts appear focused on one core question of can AXT translate AI enthusiasm into sustained earnings growth rather than temporary order spikes?

Bottom Line

In short, AXT became one of the market’s biggest AI winners because investors finally recognized the AI boom extends far beyond GPUs.

Data centers need connectivity. Connectivity needs advanced optical components. Those components need semiconductor substrates. That chain leads back to AXT.

Finally, the stock’s 8,436% return says more about how overlooked the company once was than how expensive it has become today. Smart investors should still approach AXTI carefully, but the company now sits in the middle of one of the largest infrastructure spending cycles the tech industry has ever seen.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

AXT Turned the AI Data Center Boom Into an 8,436% 1-Year Return Lockheed Martin Stock Looks Well-Positioned to Get a Big Lift From the Very Costly Golden Dome Initiative Cerebras Is the Biggest IPO of the Year. If You Buy CBRS Stock Now, Brace Yourself for Volatility Ahead. Ford’s EV Pivot Was Disastrous. Now It’s Trying to Compete with Tesla on Energy Storage.