Meta Platforms Inc (META) stock is off its recent highs after the Q1 earnings release. META could be cheap based on revenue, operating cash flow, capex, and free cash flow forecasts. Value investors are looking at shorting OTM puts.

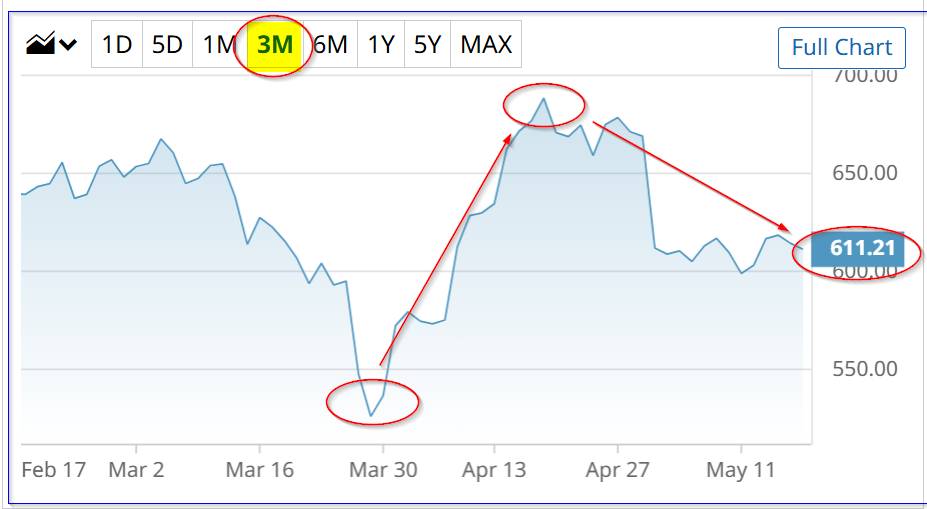

META closed at $611.21 on Monday, May 18, down slightly. However, it's well off a recent peak of $688.84 on April 17, before the April 29 earnings release. It's still up from a March 30 trough price of $536.38.

Can’t Get Enough Options?: Join the list for Barchart’s daily unusual options report, delivered free.

Meta stock - last 3 months - Barchart - May 18

Meta stock - last 3 months - Barchart - May 18 Strong FCF and Capex Outlook

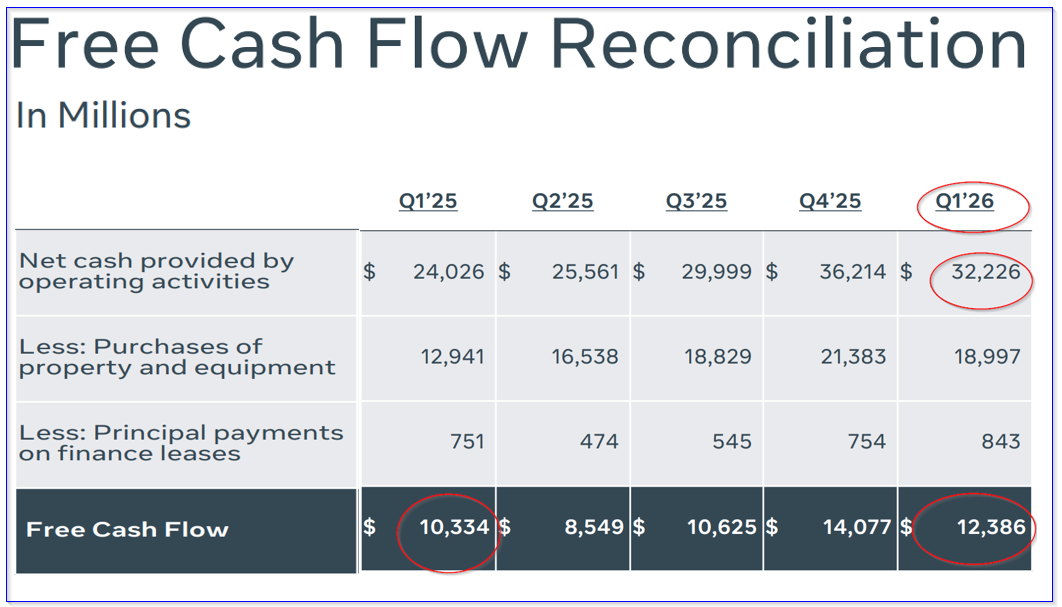

Meta delivered strong YoY free cash flow (FCF) last quarter (+19.9%), despite a 47% YoY increase in its capital expenditures (capex). This can be seen in the table provided by Meta Platforms on page 15 of its shareholder deck presentation.

Meta's quarterly FCF - deck presentation page 15 - Q1 2026

Meta's quarterly FCF - deck presentation page 15 - Q1 2026 Meta likes to include principal payments on its finance leases, as a form of capex (Meta says it's irrelevant that the company borrows money to pay for “plant”). Most other tech companies, other than Amazon, don't do this. However, even with this measure included, FCF rose significantly, though it was down last quarter.

However, more importantly, Meta projected that it intends to spend between $115 billion and $135 billion (see page 8 of the earnings transcript) on capex this year. That's +73% higher than the $72.215 billion in capex and finance lease principal payments made during 2025.

That works out to just $10.42 billion per month (i.e., $125 midpoint/12) or $31.26 billion per quarter. That is well over the $19.84 billion in Q1 capex, incl. principal payments on finance leases. It implies another +57.5% increase in quarterly capex/principal payments on finance leases compared over the next year, compared to Q1.

As a result, to project future FCF, forecast its operating cash flow, and then deduct the expected capex payments. From that, we can derive a fair value for META stock.

Projecting Meta's FCF

For example, analysts now forecast that Meta's 2027 revenue will rise to $301.63 billion. Multiplying this by its trailing 12-month (TTM) operating cash flow (OCF) margin will allow us to project its future OCF.

For example, Stock Analysts reports that its TTM OCF was $124 billion as of Q1. Since its TTM revenue was $214.62 billion, that means its TTM OCF margin was 57.77% (i.e., $124b/$214.62b).

Therefore, applying this OCF margin (rounding it up to 58%) to the analysts' 2027 revenue forecast:

$301.63 billion x 0.58 = $175 billion operating cash flow (OCF) 2027

Next, let's deduct the projected capex for 2027. Management said it expects the capex of $125 billion at the midpoint (see above). Next year, let's assume a 10% increase in 2027:

$125 billion x 1.10 = $137.5 billion 2027 capex

Therefore, free cash flow (FCF) in 2027 can be projected:

$175 billion OCF - $137.5 billion capex = $37.5 billion FCF in 2027

How will the market value this?

Setting a Price Target for META Stock

Historically, Meta Platform's stock has been valued at about a 3.0% FCF yield. For example, its Q1 TTM FCF of $48.253 billion (not incl. principal payments on finance leases) is equal to 3.1% of its market cap today of $1,552 billion (Yahoo! Finance calculation).

Just to be generous (not conservative), let's use a better FCF yield of 2.50%:

$37.5 billion FCF in 2027 / 0.0250 = $1,500 billion

That is slightly below today's market cap. Even if the company generates $40 billion in FCF, Meta's fair value would only be slightly higher:

$40b / 0.025 = $1,600 billion

$1,600b / $1,552 = 1.03 -1 = 3.0% higher fair value

That puts its price target (PT) at $629.55 per share (i.e., $611.21 x 1.03).

However, other analysts are much more optimistic. For example, Yahoo! Finance reports that the average PT is $826.69 from 63 analysts, or +35% higher. Similarly, Barchart's mean survey PT is $826.12.

AnaChart.com, which tracks recent analyst write-ups, reports that the average PT from 39 analysts is $722. So, the average of these analyst surveys is $791.60, or +29.5% higher.

One explanation why other analysts may have higher price targets is that they are able to project how much higher the operating cash flow margins will be in the future. That is based on how effectively the significantly higher capex converts into higher revenue and OCF margins. I just used the TTM OCF margin figure.

The bottom line is that META stock could be quite cheap here.

One way to play META, in case it doesn't rise further, but also doesn't drop significantly, is to sell short out-of-the-money (OTM) put options. That way, an investor can get paid while waiting to buy in at a lower strike price.

Shorting OTM META Puts

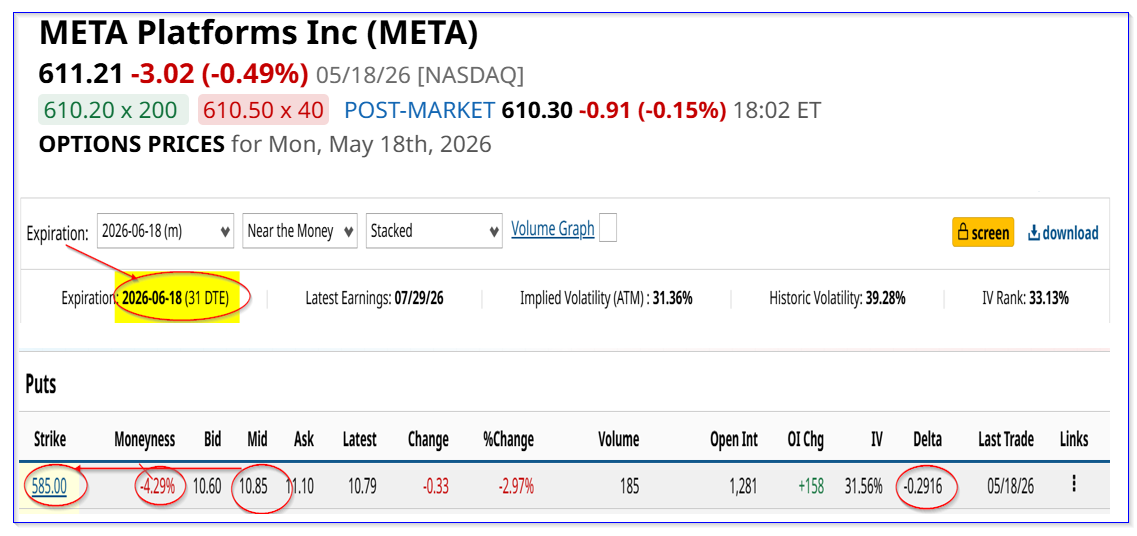

For example, the June 18 expiry put option chain shows that the $585.00 strike price put, 4% lower, has a $10.85 midpoint premium.

META puts expiring June 18 - Barchart - As of May 18, 2026

META puts expiring June 18 - Barchart - As of May 18, 2026 That means an investor can make a 1.855% income yield (i.e., $10.85/$585.00) over the next month, while waiting to buy in at a 4% lower strike price.

Moreover, even if META falls to $585.00, the investor's breakeven point is lower:

$585.00 - $10.85 = $574.15 breakeven (B/E)

$574.15 / $611.21 price today -1 = -6.0% lower

The point is that this allows an investor to set an attractive buy-in, while getting paid each month, as this play is done. For example, over three months, if repeated, the investor could make:

1.855% x 3 = 5.65%

That is the same as seeing META rise to $645.74 over the next month. In fact, over a year, the investor could theoretically make 22.26%. That is equal to a price of $747.27, or below, but not too far below the $791 average analyst price target.

Moreover, it provides some downside protection as the lower buy-in point reduces risk. The bottom line is that META looks cheap here, and one way to play it is to short out-of-the-money one-month put options.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Meta Stock Is Off Its Highs, and Could be Cheap - What's the Best META Play? NVDA Earnings Bull Put Spread has a High Probability of Success Unusual In-the-Money Put Options Trades in Amazon Stock Show Investors Bullish How Beaten-Down Tempus AI Stock Offers a Lottery Ticket for Traders Here