Prologis, Inc. PLD remains a scaled owner of infill logistics facilities that are central to modern distribution networks. Development, disciplined capital recycling and new strategic capital ventures extend the growth runway, while data centers and energy broaden the platform.

Last month, PLD posted first-quarter 2026 core funds from operations (FFO) per share of $1.50, up 5.6% from $1.42 a year ago. The figure beat the Zacks Consensus Estimate of $1.48 by 1.49%. Results were supported by robust leasing activity, while net earnings per share rose to $1.05 from 63 cents in the year-ago quarter.

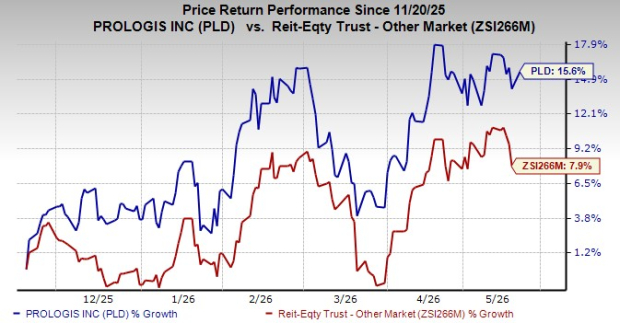

While shares of this Zacks Rank #2 (Buy) REIT have rallied 15.6% over the past six months, outperforming the industry's growth of 7.9%, there is still room for further appreciation.

Image Source: Zacks Investment Research

Factors That Make Prologis Stock a Solid Pick

Healthy Operating Performance: Prologis’ infill portfolio remains attractive to distribution users because many sites are near major airports, seaports and ground transportation corridors. In first-quarter 2026, 66.7 million square feet of leases commenced across the owned and managed operating and development portfolio, and management described logistics lease signings of about 64 million square feet as a quarterly record.

Retention was 75.8%, and both average and period-end occupancy were 95.3%. Rent capture stayed positive, with net effective rent change of 31.9% and cash rent change of 16.8% on the Prologis share portfolio in the first quarter of 2026. Cash same-store NOI grew 8.8% in the quarter, and management raised its 2026 cash same-store NOI outlook to 6.25%-7%, supporting continued rent roll-up as leases reset.

Acquisitions & Development: Prologis continues to deploy capital through a mix of acquisitions, development and recycling, allowing it to shift spending as market pricing and funding costs change. In first-quarter 2026, Prologis’ share of acquisitions was $268 million at a 4.7% stabilized cap rate, while development starts were $1.78 billion and stabilizations were $1.11 billion at a 7.6% estimated yield and 34.8% estimated margin.

For 2026, management raised its outlook for development starts to $3.50-$4.50 billion and maintained acquisitions at $1.00 to $1.50 billion. Dispositions are still expected at $1.75 to $2.25 billion, which supports funding for new projects while limiting balance sheet strain.

Data Center Diversification: Prologis is expanding beyond traditional logistics real estate by scaling digital infrastructure that can be paired with its existing land positions. In first-quarter 2026, the company started $1.3 billion of build-to-suit data center developments, and management highlighted this activity as a step forward in building the platform. Data center demand is being shaped by cloud adoption and higher computing intensity. Management’s 2026 capital deployment plan includes data centers within development activity, reinforcing its commitment to scale this business line to diversify earnings.

Balance Sheet Strength and ROE: Prologis maintains a healthy balance sheet position with ample flexibility. As of March 31, 2026, this industrial REIT had a total available liquidity of $6.7 billion. As of the same date, the company's weighted average interest rate on its share of the total debt was 3.3%, with a weighted average term of 8.1 years. Debt to adjusted EBITDA was 4.8X. The company’s credit ratings as of were A2 (Outlook Stable) from Moody’s and A (Outlook Stable) from Standard & Poor’s, enabling PLD to borrow at an advantageous rate.

This REIT’s trailing 12-month return on equity (ROE) highlights its growth potential. The company’s ROE of 6.47% compares favorably with the industry’s 2.2%, reflecting that PLD is more efficient in using shareholders’ funds than its peers. Given its balance sheet strength and prudent financial management, the company is well-poised to capitalize on growth opportunities.

Dividend: Solid dividend payouts are arguably the biggest enticements for REIT shareholders, and Prologis remains committed to that. In February 2026, the company’s board hiked its quarterly dividend by 5.9% to $1.07 per share from $1.01 paid earlier, taking the annualized dividend to $4.28 per share. In the last five years, Prologis has increased its dividend five times, and its five-year annualized dividend growth rate is 11.09%. Given the company’s solid operating platform, opportunities for growth and decent financial position compared with the industry, this dividend rate is expected to be sustainable over the near term. Check Prologis’ dividend history here.

Other Stocks to Consider

Some other top-ranked stocks from the broader REIT sector are Chatham Lodging Trust REIT CLDT and American Tower AMT, each carrying a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for CLDT’s 2026 FFO per share is pegged at $1.27, which indicates year-over-year growth of 24.5%.

The consensus estimate for AMT’s full-year FFO per share is pinned at $10.95, which calls for a 1.8% increase from the year-ago period.

Note: Anything related to earnings presented in this write-up represents funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Tower Corporation (AMT): Free Stock Analysis Report

Prologis, Inc. (PLD): Free Stock Analysis Report

Chatham Lodging Trust (REIT) (CLDT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).