Once again, Nvidia ( NVDA) delivered a record quarterly earnings report, with profits growing 140% year over year and revenue rising 85%, both ahead of analyst expectations. One particularly interesting development was the introduction of a new reporting segment: Edge. In classic Jensen Huang fashion, Nvidia appears to already be positioning for the next evolution of AI, recognizing that the long-term opportunity extends beyond massive data centers and into AI running directly on personal devices and at the network edge.

Nvidia stock has been on an extraordinary run, climbing roughly 1,500% since bottoming in late 2022. Yet despite that incredible performance, shares have actually lagged parts of the semiconductor industry over the last year and year-to-date, highlighting the reality that sustaining exceptional gains becomes increasingly difficult as companies reach enormous scale. Even Nvidia's newly authorized $80 billion share repurchase program, an eye-popping figure in absolute terms, represents only a modest percentage of its roughly $5.5 trillion market capitalization.

That does not diminish Nvidia's investment case. The company remains one of the highest-quality businesses in the market and continues to warrant a core position in many portfolios, supported by robust growth expectations and a still-reasonable valuation of roughly 27x forward earnings alongside projected long-term EPS growth of 41% annually. Investors who own broad index funds already likely have substantial exposure.

But for investors searching for AI stocks that may still have the potential for outsized returns, smaller companies further down the AI supply chain may offer greater upside. Three that stand out are Innodata ( INOD), Credo Technology Group ( CRDO), and Qualcomm ( QCOM).

Image Source: Zacks Investment Research

Innodata: Shares Approach Breakout Level

Innodata is a global data engineering company that has become a critical infrastructure partner for the world's largest AI labs. The company provides AI training and post-training data, model evaluation, alignment, safety testing, and deployment services, representing the human-in-the-loop layer that frontier generative AI models depend on. With over 12,000 professionals across more than 70 countries, Innodata serves multiple Big Tech clients including several members of the Magnificent Seven, and recently launched a dedicated Federal practice to pursue U.S. government AI contracts.

The company's most recent quarter was a blowout. Q1 2026 revenue surged 54% year-over-year to a record $90.1 million, beating consensus by 18%. Adjusted EBITDA nearly doubled to $25.0 million, crushing estimates by 139%, while adjusted gross margin expanded to 47%, seven points above the company's own target. Revenue from Big Tech customers outside its largest client grew 453% year-over-year. Management raised full-year revenue growth guidance to 40% or more and announced new engagements with a Big Tech customer expected to generate approximately $51 million in incremental 2026 revenue.

Following the exceptional earnings report, shares rocketed more than 100% higher in the following two trading sessions. It has since then been consolidating in an increasingly tightening bull flag, indicating a potential continuation setup. If the shares can break above the upper bound of the range, it could start the next major leg higher in the stock. At a $3 billion market cap, and clients who represent the largest and most critical businesses in the AI boom, there is plenty of upside opportunity in this stock.

Image Source: TradingView

Credo Technology Group: Major Earnings Report Approaches

Credo Technology is a semiconductor company specializing in high-speed connectivity solutions for data center infrastructure. Its products, including active electrical cables, optical DSPs, line card PHYs, and SerDes chiplets, solve the bandwidth bottleneck at the physical layer, enabling data to move faster and more efficiently across AI-driven networks operating at 400G, 800G, and the emerging 1.6T speeds. The company sells directly to hyperscalers, optical module manufacturers, and OEMs, placing it squarely in the critical path of the AI data center buildout.

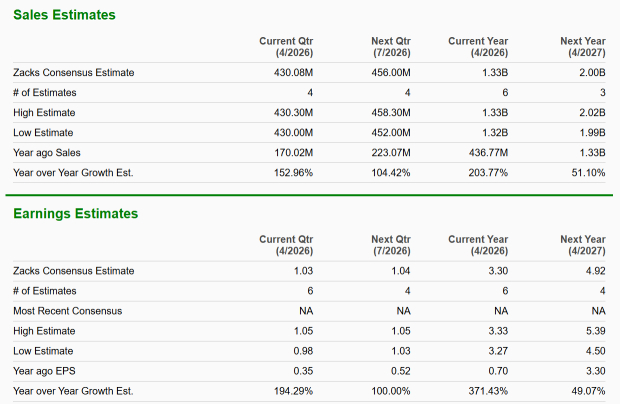

The growth trajectory here is staggering. Consensus estimates call for revenue to jump approximately 200% this fiscal year and another 51% next year, with earnings expected to follow a similar trajectory, up roughly 371% this year and 49% next year.

Credo is set to report fourth quarter and full fiscal year 2026 results on June 1, with significant expectations already baked in. Last quarter delivered record revenue of $407 million, non-GAAP gross margins of 68.6%, and a non-GAAP net margin above 51%. Management guided Q4 revenue to $425–$435 million. The bar is high, but if the company can deliver an upside surprise on top of already elevated estimates, this stock could have considerably more room to run.

At a $37 billion market cap, Credo is admittedly no longer a small company. But with growth of this magnitude, a still reasonable valuation at 37x forward earnings, and an increasingly devoted investor following, the risk-reward profile remains quite asymmetric.

Image Source: Zacks Investment Research

Qualcomm: Semiconductor Giant Quietly Gaining Steam

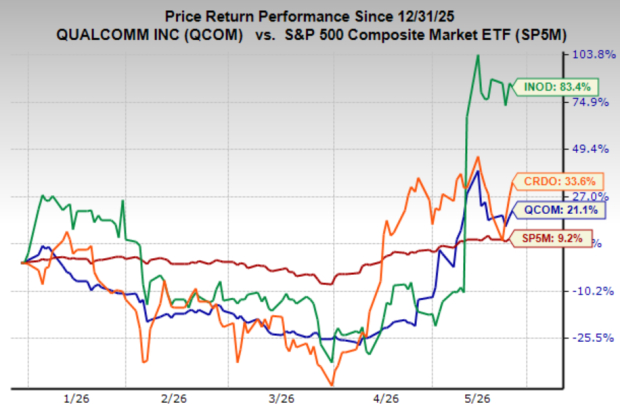

Qualcomm is the world's leading designer of mobile processors and wireless technology, powering the vast majority of premium Android smartphones and an expanding range of connected devices. But the real story is what comes next. As AI moves beyond the data center and onto devices, phones, PCs, automobiles, industrial systems, Qualcomm is uniquely positioned to capture that shift. Unlike data center chip designers who optimize for raw performance with generous power and thermal budgets, Qualcomm has spent decades engineering high-performance silicon under the tight size, power, and thermal constraints of mobile devices, expertise that translates directly to edge AI, where efficiency is everything. It is no coincidence that Nvidia just broke out a dedicated Edge reporting segment in its latest earnings report, as the opportunity at the network edge is real, and Qualcomm has been building toward it longer than almost anyone.

Despite that positioning, QCOM has been one of the most conspicuous laggards of the AI boom. That is starting to change. A confluence of catalysts has finally forced Wall Street to reprice the stock, including a landmark partnership with OpenAI, a strong earnings report, breakout growth in the automotive business, and mounting evidence that on-device AI is accelerating faster than expected. I broke down the full setup in detail here.

Shares rallied sharply following earnings as investors began to rerate QCOM as a genuine AI beneficiary. But not everything gets priced in overnight. After that initial surge, the stock built out a descending wedge over the following weeks, and just broke out of it, potentially marking the start of the next major leg higher.

Qualcomm is the largest company in this group at roughly $215 billion in market cap, which naturally limits the potential for a parabolic move. But at just 18.8x forward earnings, the stock still carries a commodity-like multiple for what is increasingly an AI platform story. With room for further multiple expansion and massive opportunities in edge AI that remain almost entirely unpriced, QCOM could still deliver outsized returns from here.

Image Source: TradingView

Should Investors Buy Shares in QCOM, CRDO and INOD?

Nvidia becoming a $5+ trillion company does not make it a poor investment. The company remains one of the strongest businesses in the market, with dominant positioning and exceptional growth prospects. But size inevitably matters, and sustaining outsized returns becomes increasingly difficult at that scale.

That creates an opportunity further down the AI supply chain. Innodata, Credo, and Qualcomm are not competing with Nvidia, they are benefiting from the same AI boom while operating from much smaller bases. For investors seeking AI exposure with greater upside potential, these three may offer compelling opportunities.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

QUALCOMM Incorporated (QCOM): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Innodata Inc (INOD): Free Stock Analysis Report

Credo Technology Group Holding Ltd. (CRDO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).