Williams-Sonoma, Inc. WSM delivered better-than-expected results for the first quarter of fiscal 2026 (ended May 3), with earnings outpacing expectations on steady demand across its brand portfolio and growing year over year. Meanwhile, net revenues met the expectations but grew year over year.

The company’s growth was supported by positive comparable performance across its key concepts, with several banners delivering meaningful contributions to the top line.

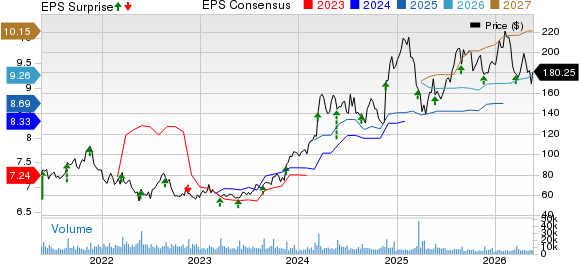

WSM’s Q1 Earnings, Revenues & Comps Discussion

WSM posted earnings of $1.93 per share, up 4.3% year over year and ahead of the Zacks Consensus Estimate of $1.80 by 7.2%.

Net revenues of $1.81 billion rose 4.4% from the year-ago quarter and came in line with the consensus mark of $1.81 billion. Comparable brand revenues increased 4.8% in the quarter.

Williams-Sonoma, Inc. Price, Consensus and EPS Surprise

Williams-Sonoma, Inc. price-consensus-eps-surprise-chart | Williams-Sonoma, Inc. Quote

WSM Posts Broad Revenue Gains Across Brands

Pottery Barn remained the largest revenue contributor, generating $708.4 million for the quarter, with Pottery Barn Kids and Teen generating revenues of $240.1 million. Pottery Barn Kids and Teen comps rose 4.5%, and Pottery Barn comps increased 1%, reflecting a more balanced demand backdrop across the portfolio.

West Elm continued to stand out in terms of momentum, producing $471.2 million of net revenues, with comps growing 8.5% year over year. The Williams Sonoma brand (including Williams Sonoma Home) posted $271.5 million and the brand’s comps increased 5% compared with a year ago.

The “Other” bucket, which includes concepts such as Rejuvenation, Mark and Graham, international franchise operations, GreenRow and Dormify, generated $114.1 million.

Williams-Sonoma Margin Mix Shifts

Gross margin was 44% for the quarter, down 30 basis points (bps) from the prior-year level. The company attributed the change primarily to lower merchandise margins, which were pressured by 100 bps year over year.

That headwind was partially offset by supply-chain efficiencies, which contributed 50 bps, and occupancy leverage, which added 20 bps.

Selling, general and administrative expenses were 27.8% of net revenues, increasing 30 bps year over year.

Williams-Sonoma Operating Profit Holds Steady

Operating income for the quarter was $291.7 million, and operating margin was 16.2%, down 60 bps year over year. While the margin declined modestly, the company still produced operating income essentially in line with the prior-year quarter’s $290.7 million, supported by revenue growth and continued cost discipline.

Net earnings totaled $231.4 million, essentially flat with $231.3 million a year ago, reflecting the interplay of margin pressure, expense trends and tax costs during the period.

WSM Cash Flow Support Capital Returns

WSM ended the first quarter with cash and cash equivalents of $651.6 million, down from $1.02 billion as of fiscal 2025.

Net cash provided by operating activities was $156.3 million for the quarter, up from $118.9 million in the year-ago quarter, supporting continued shareholder returns.

WSM repurchased $287.8 million of common stock and paid $85.6 million in dividends during the period, highlighting an ongoing emphasis on returning capital while maintaining flexibility.

Williams-Sonoma Reiterates 2026 Outlook on Tariff Assumptions

For fiscal 2026, WSM expects annual net revenues to increase in the range of 2.7-6.7%, with comparable brand revenue growth (comps) in the range of 2-6%. WSM also continues to project an operating margin between 17.5% and 18.1% for the year.

The outlook assumes oil prices remain elevated and that there is no refund of tariffs paid, with tariff impacts expected to be front-loaded in the first half of fiscal 2026 as higher costs flow through the company’s weighted-average cost of goods sold.

WSM also expects annual interest income of approximately $25 million and an effective tax rate of about 25.5% for fiscal 2026, while maintaining its long-term view for mid-to-high single-digit annual net revenue growth and an operating margin in the mid-to-high teens.

WSM Stock’s Zacks Rank & Peer Releases

Williams-Sonoma currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Home Depot, Inc. HD delivered first-quarter fiscal 2026 results that topped the Zacks Consensus Estimate on both the top and bottom lines. Adjusted earnings were $3.43 per share, down 3.7% from the year-ago quarter but came above the consensus mark of $3.40. Net sales rose 4.8% year over year to $41.77 billion and beat the consensus estimate of $41.49 billion.

The underlying business demand has been relatively similar to the trends seen throughout fiscal 2025, amid consumer uncertainty and housing affordability pressure. Comparable sales (comps) increased 0.6% in the quarter, with U.S. comps up 0.4%. Home Depot reaffirmed its fiscal 2026 framework, calling for total sales growth of approximately 2.5-4.5% and comparable sales growth of roughly flat to 2%.

Wayfair Inc. W reported its first-quarter 2026 results on April 30, driven by a revenue outperformance against consensus estimates and a return to active customer growth after multiple quarters of year-over-year decline.

Wayfair reported first-quarter 2026 earnings of 26 cents per share, which met the Zacks Consensus Estimate. Net revenues for the first quarter of 2026 rose 7.4% year over year to $2.93 billion, surpassing the Zacks Consensus Estimate of $2.88 billion by 1.72%. For the second quarter of 2026, Wayfair expects revenues to grow in the mid-single digits year over year. Adjusted EBITDA margin is guided in the 6-7% range for the second quarter.

Lowe’s Companies, Inc. LOW has reported first-quarter fiscal 2026 results, wherein both earnings and sales surpassed the Zacks Consensus Estimate. Adjusted earnings were $3.03 per share, rising 3.8% year over year and beating the Zacks Consensus Estimate of $2.96 by 2.4%. Net sales came in at $23.1 billion, rallying 10.3% from the year-ago quarter and surpassing the consensus mark of $22.9 billion by 0.6%.

Management has highlighted that Lowe’s Total Home strategy continues to resonate with both Pro and DIY customers despite a challenging housing backdrop. Lowe’s reaffirmed its fiscal 2026 guidance and expects total sales between $92 billion and $94 billion, indicating year-over-year growth of 7-9%. Comparable sales are anticipated to be flat to up 2%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lowe's Companies, Inc. (LOW): Free Stock Analysis Report

The Home Depot, Inc. (HD): Free Stock Analysis Report

Williams-Sonoma, Inc. (WSM): Free Stock Analysis Report

Wayfair Inc. (W): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).