Appian Corporation’s APPN first-quarter 2026 financial results delivered clear evidence that the company's growth momentum is reaccelerating. Cloud subscription revenues rose 25% year over year to $124.5 million, while total revenues increased 21% to $202.2 million. The company also reported 115% cloud net ARR expansion, up from 112% a year ago, suggesting stronger expansion within the existing customer base. Management highlighted strong demand for AI-powered automation, particularly for its DocCenter and Agentic AI offerings, which are gaining traction across regulated industries and large enterprises.

The key driver behind the improving outlook is AI. Management said AI demand is pushing Appian’s 2026 pipeline above expectations, with nearly 40% of customers now using AI-inclusive license tiers. DocCenter, in particular, is emerging as a broad enterprise use case, with customers processing more document pages during the first quarter of 2026 than in all of 2025 combined. At the same time, Appian continues to benefit from momentum in enterprise modernization initiatives and larger strategic deals tied to process automation and AI deployment.

The key question is whether this marks a return to sustainable 20%-plus cloud growth. On a constant-currency basis, cloud subscription revenues grew 20%, which management noted was Appian’s fastest pace in two years. At the same time, profitability continued to improve alongside growth. Adjusted EBITDA reached $26.6 million, comfortably above guidance, while Appian’s weighted Rule of 40 score rose to 42, its highest level since the company introduced the metric last year. The company also raised its full-year outlook, now projecting cloud subscription revenues between $515 million and $521 million, representing 18%-19% annual growth.

Overall, Appian’s first-quarter performance strengthens the case that growth is reaccelerating, especially as AI adoption, enterprise modernization and larger strategic deals gain momentum. But for now, sustainable 20%-plus growth remains a possibility rather than the base case.

Appian Faces Intensifying Competition From Pegasystems & Salesforce

Appian continues to strengthen its position in the enterprise automation and AI-driven workflow market through the rising adoption of its AI-powered process automation platform. However, the company faces intensifying competition from Pegasystems Inc. PEGA and Salesforce Inc. CRM, both of which are aggressively expanding their AI and enterprise automation capabilities.

Pegasystems is benefiting from accelerating demand for Pega Cloud, AI-driven workflow automation and enterprise modernization initiatives. The company also highlighted growing momentum from Blueprint, its AI-powered workflow design platform, which is helping expand pipeline activity and new customer acquisition. Pegasystems expects Pega Cloud ACV to continue increasing as customers migrate away from traditional on-premise and maintenance-based deployments toward cloud-native automation solutions.

Meanwhile, Salesforce is rapidly scaling its enterprise AI ecosystem through Agentforce, Data 360 and Slack-integrated automation tools. The company reported strong demand for AI-enabled enterprise workflows, with wins above $1 million rising 26% year over year in fourth-quarter fiscal 2026. Salesforce said Agentforce has become an approximately $800 million business, while combined Agentforce and Data 360 ARR exceeded $2.9 billion in fourth-quarter fiscal 2026, representing 200% year-over-year growth.

APPN’s Share Price Performance, Valuation and Estimates

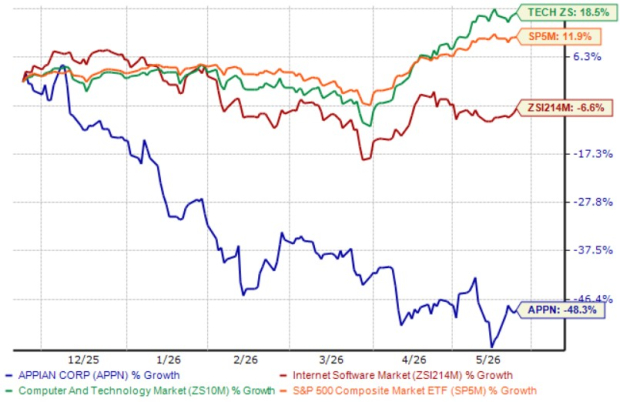

Appian’s shares have declined 48.3% in the trailing six months, underperforming the Zacks Computer & Technology sector, the broader Internet - Software industry and the S&P 500 Index.

APPN Stock Performance

Image Source: Zacks Investment Research

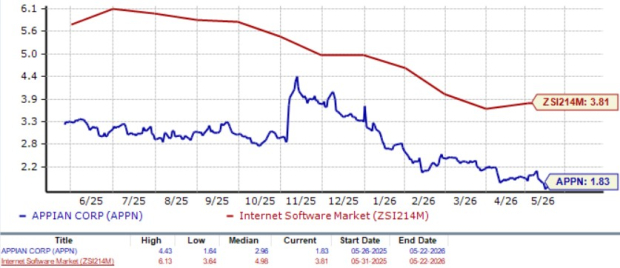

Appian’s shares are currently trading at a discount, with a forward 12-month price-to-sales (P/S) ratio of 1.83, as shown in the chart below.

APPN Valuation

Image Source: Zacks Investment Research

Estimates for Appian’s 2026 earnings have moved upward in the past 30 days to 91 cents per share. The estimated figure for 2026 earnings implies growth of 49.2% year over year on projected revenue growth of 13.3%.

Image Source: Zacks Investment Research

Appian currently carries a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Salesforce, Inc. (CRM): Free Stock Analysis Report

Pegasystems Inc. (PEGA): Free Stock Analysis Report

Appian Corporation (APPN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).