BrightSpring Health Services, Inc. BTSG is spending 2026 absorbing policy and pricing resets while pushing harder into coordinated home-based care. The company’s integrated pharmacy and provider footprint spans all 50 states, with operations designed to keep complex patients in lower-cost settings.

The near-term setup is noisy. Reported revenue trends can look weaker even when operating performance and margins improve, which puts execution and cadence at the center of the debate in coming quarters.

BTSG’s 2026 Headwinds Are Structural, Not One-Off

Management has quantified roughly $600 million of expected 2026 revenue headwinds tied to Inflation Reduction Act-related reimbursement changes and brand-to-generic conversions. That total includes about $175 million in Home and Community Pharmacy, around $181 million in Specialty and Infusion tied to the Inflation Reduction Act, and roughly $250 million from generic conversions.

Those pressures are not confined to a single quarter, which can distort growth optics. In Home and Community Pharmacy, management guided to an Inflation Reduction Act impact of about $45 million per quarter for the remaining quarters of 2026, implying a multi-quarter drag even if underlying profitability per script improves.

BrightSpring’s Scale Positions It for Payer Demand Shifts

BrightSpring’s strategic premise aligns with payer priorities: lower-cost, coordinated solutions that shift care away from higher-acuity settings. The company positions its platform around seniors and specialty populations across Medicare, Medicaid, and commercial payors, with first-quarter 2026 mix that included Medicare Part D near 29.7%, Medicare Advantage around 16.7%, commercial nearly 26.5%, and Medicaid roughly 8.5%.

The differentiator is co-location. With pharmacy and provider operations across all 50 states, BrightSpring can support integrated care pathways and value-based models that depend on tight coordination between medication management and in-home clinical services. Management cites more than 475,000 patients served daily and approximately 12,400 clinical providers and pharmacists as evidence of national scale.

BTSG Specialty and Infusion Win Share Despite Resets

Specialty and Infusion remains the primary growth engine inside Pharmacy Solutions. In first-quarter 2026, Specialty and Infusion revenue rose 36% year over year to $2.64 billion, supported by limited-distribution access, new wins, generic utilization, and commercial execution.

Management highlighted adding four exclusive ultra-narrow limited distribution drugs in the quarter, lifting the limited distribution drug portfolio to 153. The company also expects double-digit infusion growth across acute and chronic specialty categories, with initiatives such as concierge programs aimed at increasing participation in chronic categories.

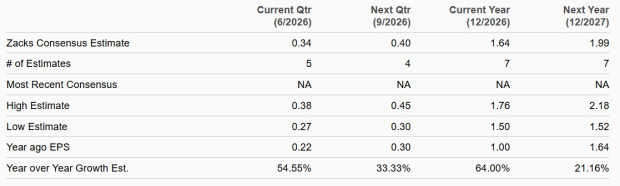

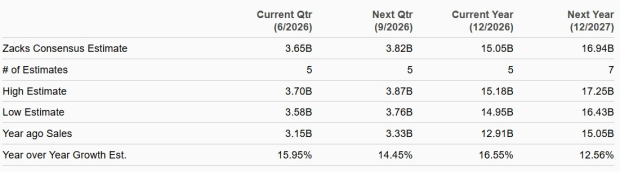

The key takeaway is that guidance moved higher even with known pricing resets. BrightSpring raised 2026 adjusted EBITDA guidance to $795 million to $825 million, which signals confidence that volume, mix, and efficiency can more than offset the policy and conversion headwinds over time.

Image Source: Zacks Investment Research

BrightSpring’s Provider Quality Metrics Fuel Referrals

Provider Services is the other pillar supporting the 2026 narrative. In first-quarter 2026, Provider Services revenue grew 28% year over year to $442 million, driven by acquired home health branches, de novo expansion, preferred Medicare Advantage contracts, and census growth. Home Health Care revenue increased 49% to $266 million.

Quality metrics are positioned as a competitive lever for referrals and payer relationships. Management cited more than 91% of home health branches rated 4 stars or higher and timely initiation of care above 99%, metrics it links to referral growth, preferred payer relationships, and margin durability as Provider Services scales.

Integration economics matter here. Acquired assets contributed about $79 million of revenue and around $9 million of adjusted EBITDA in the first quarter, with expectations for roughly $30 million of adjusted EBITDA contribution in 2026 as centralized intake, technology standardization, and operating efficiencies roll through the footprint.

Image Source: Zacks Investment Research

BTSG Home and Community Is Repositioning for Profit

Home and Community Pharmacy is being managed for profitability, not headline growth. In first-quarter 2026, segment revenue declined 9% year over year to $527 million, which management tied primarily to an approximately $50 million Inflation Reduction Act impact and exiting uneconomic customers.

The strategy centers on focusing on profitable end-markets and investing in automation across the national footprint. Management has pointed to assisted living, hospice, behavioral, Programs of All-Inclusive Care for the Elderly, and skilled nursing as focus areas while the business cycles through the reset during 2026.

Even with these initiatives, the cadence is likely to keep reported revenue pressured near term. With the quarterly Inflation Reduction Act impact expected to persist through the balance of 2026, the segment’s recovery is set to be measured more by mix and efficiency than by top-line momentum.

BrightSpring’s 2026 Narrative Investors Will Debate

The market’s central tension is straightforward: uneven revenue optics versus the case for margin expansion and integration progress. BrightSpring expects sequential improvement through 2026, with adjusted EBITDA growing faster than revenue as mix, efficiency programs, and a midyear generic launch support company-level margin expansion.

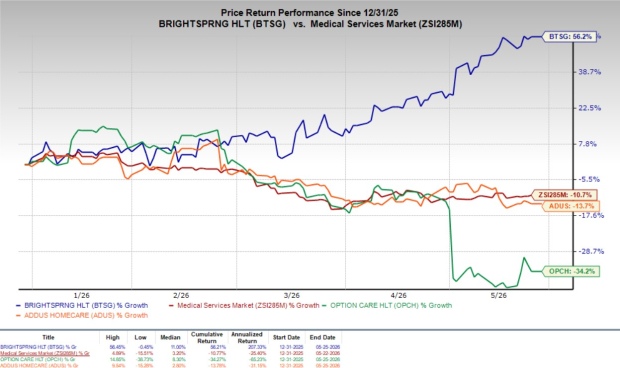

That debate is not unique to BTSG. Option Care Health, Inc. OPCH and Addus HomeCare Corporation ADUS also operate in home-based care categories where payers want lower-cost settings and consistent outcomes, and where execution can drive meaningful dispersion in results.

In the year-to-date period, shares of BrightSpring rallied 56.2% against the industry’s 10.7% decline. In the same time frame, the company’s peers, shares of Addus HomeCare Corporation and Option Care Health, Inc. have plunged 13.7% and 34.2%, respectively.

At present, BTSG sports a Zacks Rank #1 (Strong Buy) and Addus HomeCare Corporation holds a Zacks Rank #3 (Hold). On the other hand, Option Care Health carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Image Source: Zacks Investment Research

For BrightSpring, “durable earnings expansion” will be reinforced if upcoming quarters show steady Specialty and Infusion momentum, continued Provider Services integration progress toward the full-year contribution target, and visible stability in Home and Community Pharmacy as the pricing reset is absorbed.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Addus HomeCare Corporation (ADUS): Free Stock Analysis Report

Option Care Health, Inc. (OPCH): Free Stock Analysis Report

BrightSpring Health Services, Inc. (BTSG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).