Mama’s Creations, Inc. MAMA is scaling into a national, multi-brand deli-prepared foods platform with expanding distribution and supportive category trends.

The push comes with trade-offs. The opportunity is fast shelf expansion and operating scale. The friction points are commodity and freight volatility, promotional and club-related lumpiness, and execution complexity across an expanded manufacturing network.

MAMA’s Growth Setup and What It Depends On

The core setup is straightforward. Mama’s is benefiting from favorable deli-prepared food trends while widening national distribution and branded penetration. Product innovation and cross-selling opportunities, amplified by the Crown 1 Foods acquisition, strengthen a “one-stop-shop” deli platform strategy.

What the thesis depends on is equally clear. Growth must be paired with operational follow-through, including effective trade spending, improving Bay Shore margins, and successful integration across a three-facility manufacturing network.

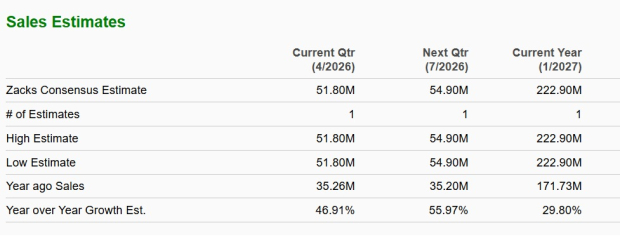

Image Source: Zacks Investment Research

Mama’s Creations Has Scale Momentum in Fiscal 2026

Fiscal 2026 net sales increased 39.2% to $171.7 million from $123.3 million in fiscal 2025. The lift was driven by volume growth, expanded distribution, new product placements, pricing actions, and the Crown 1 acquisition.

Momentum accelerated late in the year. Fourth-quarter fiscal 2026 revenue rose 60.7% to $54 million, supported by stronger sales velocity, new product launches, and acquisition contributions. Operating leverage showed up in adjusted EBITDA, which improved 77% to $5.5 million, while operating expenses improved as a percentage of revenue.

MAMA’s “Quality of Growth” Signals To Track

A practical checklist starts with retailer support. The company’s distribution momentum spans grocery, mass, club, and convenience channels, and continued placement wins are central to sustaining share gains.

Next is sell-through at new doors. New listings can compound into steadier baseline demand if replenishment normalizes and velocities hold after initial resets and marketing support.

Third is stock keeping unit growth within existing accounts. Management’s stated goal is to add a net two stock keeping units across top accounts, a cadence that can drive repeatable growth without relying only on new customer wins.

Finally, watch whether growth becomes less dependent on one-off promotions or rotations. The business can post uneven quarters from promotional timing and club activity, so improving underlying consistency is a key “quality” signal.

Mama’s Creations Margin Path: Levers and Milestones

Margin improvement is a second leg of the risk-reward. Fiscal 2026 gross margin rose to 25.1%, and fourth-quarter fiscal 2026 gross margin reached 25.9%, even with the lower-margin Bay Shore facility still ramping. Management targets a mid- to high-20% corporate gross margin profile over time.

The levers are operational and repeatable: centralized procurement, improved freight efficiency, in-house chicken trimming, better production balancing across facilities, automation, enhanced planning systems, and labor productivity improvements as overtime declines.

Milestones to watch center on Bay Shore. The improvement plan includes procurement savings, throughput gains, logistics optimization, stock keeping unit rationalization, and systems integration. Near-term quarters can still swing due to mix, promotions, and input-cost moves before pricing catches up.

MAMA’s Balance Sheet Flexibility Supports the Plan

Liquidity matters because this is a build-and-integrate story. Mama’s ended fiscal 2026 with $20 million in cash and $5.4 million of debt, providing flexibility without materially stressing the balance sheet.

That financial position supports investment in automation, shelf-life technology, productivity initiatives, network optimization, innovation, and selective acquisitions. Management has also emphasized disciplined, accretive deal-making that adds capabilities, capacity, categories, or customer access.

Mama’s Creations Customer Concentration Cuts Both Ways

Large retailers can scale volume quickly, and Mama’s is leveraging that dynamic as national distribution expands. But concentration also raises negotiating and execution risk. Two customers accounted for approximately 38% and 17% of fiscal 2026 gross revenue, so any setback can be meaningful.

Retailers also hold leverage over pricing, promotions, shelf space, and assortment decisions. If new items underperform, retailers can reduce shelf space, slow rollouts, or require higher promotional support. Private-label growth is another competitive pressure to monitor. For context, Walmart Inc. WMT and Costco Wholesale Corporation COST both carry a Zacks Rank #3 (Hold), which reinforces that these high-volume channels can be powerful growth partners but also performance-driven in how they manage space and programs. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Image Source: Zacks Investment Research

MAMA’s Club Exposure Can Make Results Lumpy

Club programs can create volatility that looks like “noise” in quarterly results. Multi-vendor mailers, rotations, and promotional events can lift revenue and plant absorption in one period, then create difficult comparisons later.

This dynamic is best framed as an expectation, not automatically a thesis-breaker. The key is whether promotions and rotations translate into steadier everyday placements and more durable baseline volume over time. Mama’s currently carries a Zacks Rank #4 (Sell).

Mama’s Creations Decision Framework

The setup fits investors who can tolerate quarterly variability in exchange for national scaling, broader retailer relevance, and a credible margin-improvement roadmap supported by procurement and operating efficiencies.

It may be a “watch” for those who need smoother predictability. Commodity and freight volatility, retailer concentration, promotional dependence, and integration execution across three facilities can all create uneven results even when demand trends are supportive.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Mama's Creations, Inc. (MAMA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).