Powell Industries, Inc. POWL and EnerSys ENS are both prominent names operating in the electrical components and equipment sector. As rivals, these companies are engaged in providing highly engineered electrical equipment and energy storage solutions in the United States and internationally.

While Powell has been enjoying growth opportunities in electric utility and industrial markets, EnerSys is benefiting from growing needs for eco-friendly energy storage solutions across transportation, aerospace and defense markets. But which one has the better upside potential? Let’s take a closer look at their fundamentals, growth prospects and challenges to make an informed choice.

The Case for Powell

Powell’s results in second-quarter fiscal 2026 (ended March 2026) indicated strong year-over-year growth, with revenues growing 6% to $297 million. The results were driven by persistent strength and healthy levels of project activity across the electric utility and commercial & other industrial markets. Growing investments across power generation and electrical distribution markets have been driving demand for its products in the electric utility market.

Several positive trends across the oil and gas market, including growth in energy transition projects, such as biofuels, sustainable aviation fuel, carbon capture and hydrogen production, are likely to be favorable for the company. Although currently subdued, the company expects the petrochemical market to recover from a gradual increase in commercial activity in the quarters ahead.

Its increased participation across the electrical power value chain has enabled it to generate solid bookings from the electric utility and commercial & other industrial markets. This has led to a strong backlog level, which was $1.8 billion (up 33% year over year and 12% sequentially) while exiting the second-quarter fiscal 2026. Exiting the fiscal second quarter, new orders totaled $490 million, higher than $249 million in the previous fiscal year quarter.

POWL’s solid liquidity position with no debt also supports its shareholder-friendly activities. Exiting the fiscal second quarter, Powell had cash equivalents and short-term investments of $544.9 million compared with $475.5 million at the end of fiscal 2025.

Despite the positives, the company has been grappling with high operating costs and expenses. In the first six months of fiscal 2026, its cost of sales rose 3% year over year, while selling, general and administrative expenses increased 17.9%. In the fiscal second quarter, the company’s gross profit margin contracted 30 basis points (bps) to 29.6%, while the operating margin declined 170 bps to 19.4%.

The Case for EnerSys

EnerSys has been witnessing strength in its Specialty segment, driven by solid momentum in the aerospace and defense end markets. The segment’s revenues increased 8.1% year over year in the fourth quarter of fiscal 2026 (ended March 2026). The Energy Systems segment is benefiting from the expansion of U.S. communications networks, fueled by AI-driven data demand. Increased demand for products from industrial customers also bodes well. The segment’s revenues increased 7% in the fiscal fourth quarter.

The global megatrends, including 5G expansion, rural broadband build-outs, modernization of energy grids, electrification, automation and decarbonization, are aiding the company. Driven by strength across its businesses, EnerSys expects net sales to be in the band of $915–$955 million for fiscal 2027 (ending March 2027), indicating 5% year-over-year increase at the midpoint.

The company is making progress in new areas, including lithium battery solutions for data centers and energy storage systems for warehouses, both of which moved into customer testing and commissioning in the fiscal fourth quarter.

EnerSys announced its decision to shut down its lead-acid battery manufacturing plant in Tijuana, Mexico. The company will work on transitioning the majority of the production to its existing Thin Plate Pure Lead (TPPL) plant, based in Springfield, MO. This will help EnerSys to scale its TPPL platform, optimize its U.S. manufacturing footprint and better serve its data center customers.

EnerSys remains committed to rewarding its shareholders through dividends and buybacks. In fiscal 2026, it paid out dividends of $38.1 million and bought back its shares worth $370.7 million. Also, the company hiked its quarterly dividend by 9% to 26.25 cents per share in August 2025.

However, ENS has been witnessing weakness in its Motive Power segment. The slowdown is caused by deferred customer capital spending in logistics and warehousing. Also, tariff-related pressures and softer demand from smaller customers have weighed on the company’s higher-margin product mix and ordering patterns. The segment’s revenues declined 5.7% year over year in the fiscal fourth quarter.

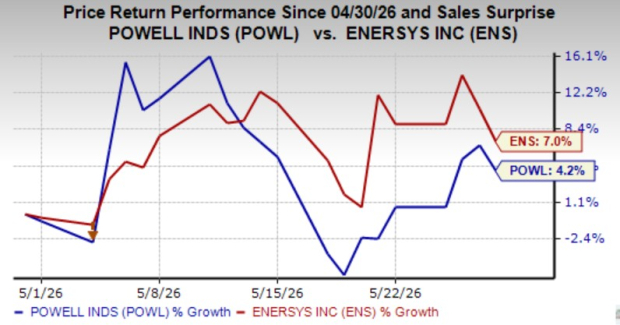

Price Performance

In the past month, Powell’s shares have increased 4.2%, while EnerSys stock has gained 7%.

Image Source: Zacks Investment Research

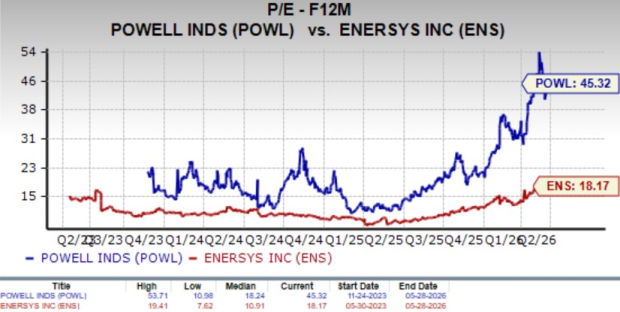

ENS’ Valuation Attractive Than POWL

Powell is trading at a forward 12-month price-to-earnings ratio of 45.32X, above its median of 18.24X over the last three years. ENS’ forward earnings multiple sits at 18.17X, higher than its median of 10.91X over the same time frame.

Image Source: Zacks Investment Research

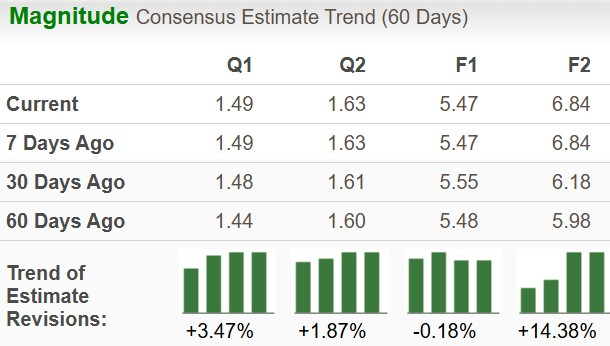

The Zacks Consensus Estimate for POWL & ENS

The Zacks Consensus Estimate for POWL’s fiscal 2026 sales and earnings per share (EPS) implies year-over-year growth of 8.7% and 10.5%, respectively. While EPS estimates for fiscal 2026 have decreased over the past 60 days, the estimate for fiscal 2027 have increased.

Image Source: Zacks Investment Research

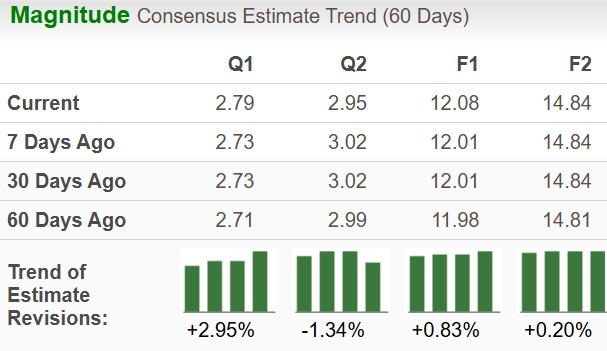

The Zacks Consensus Estimate for ENS’ fiscal 2027 sales and EPS implies year-over-year growth of 3.3% and 14.4%, respectively. The EPS estimates for both fiscal 2027 and fiscal 2028 have increased over the past 60 days.

Image Source: Zacks Investment Research

Final Take

Powell and EnerSys currently have a Zacks Rank #3 (Hold) each, which makes choosing one stock a difficult task. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Powell’s strong momentum in the electric utility, commercial and other industrial markets, driven by solid order rates and robust backlog, bodes well for growth. However, POWL's strength in the markets has been dented by rising operating expenses, which might affect its margins and profitability. Also, the stock’s expensive valuation warrants a cautious approach for existing investors.

In contrast, EnerSys’ strong momentum in aerospace, defense and industrial markets, and strategic investments bode well for growth in the quarters ahead. Additionally, ENS’ upwardly revised estimates instil confidence. Given these factors, ENS seems to be a better pick for investors than POWL currently.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Enersys (ENS): Free Stock Analysis Report

Powell Industries, Inc. (POWL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).