Houlihan Lokey HLI) has long been one of the most respected names in independent investment banking, but its stock is now facing a meaningful shift in analyst sentiment.

Over the past several weeks, earnings estimates have been moving sharply lower, with the downward trend reflecting a combination of softer-than-expected financial results, weakening momentum in key business lines, and cautious management commentary.

With EPS revisions falling this broadly, Houlihan’s stock has been flagged as a potential underperformer, landing a Zacks Rank #5 (Strong Sell) and the Bear of the Day.

Image Source: Zacks Investment Research

A Double Miss That Reset Expectations

Sparking concerns was Houlihan’s most recent fiscal fourth-quarter report last month, the catalyst for what has been a wave of downward EPS revisions:

Q4 Revenue of $635.64 million missed the $687.1 million Consensus by 7% and fell 4% from the prior year quarter.Q4 EPS of $1.63 missed expectations of $1.84 by 11% and dropped from $1.96 a year ago.

Image Source: Zacks Investment Research

A miss on both the top and bottom line is usually enough to trigger estimate cuts, but what concerned analysts even more was that the weakness showed up in Houlihan’s core Financial Restructuring (FR) business, which advises companies, creditors, private equity sponsors, and other stakeholders when a company is under financial stress or needs to reorganize its balance sheet.

Restructuring Slowdown & Broad Underperformance

Best known for its leadership in financial restructuring, a segment that historically delivers some of Houlihan's highest margins, recent declines have raised eyebrows.

To that point, Q4 Restructuring revenue fell 33% YoY to $110.4 million and noticeably missed expectations of $137.2 million.

This is a notable shift because restructuring tends to boom during periods of broader economic uncertainty, which, of course, has been highlighted by elevated interest rates and higher energy prices from the War in Iran. That said, the current restructuring environment has seen fewer large-scale distress situations. With the cycle cooling, analysts are recalibrating their forward assumptions.

Furthermore, the weakness wasn’t isolated to restructuring, as revenue for Houlihan’s Corporate Finance and Valuation Advisory segments also came in below expectations:

Q4 Corporate Finance revenue: $433.8M vs. $448.8M expectedQ4 Valuation Advisory revenue: $91.5M vs. $95.5M expected

When every major business line misses estimates, analysts tend to assume the softness is macro-driven and likely to persist.

Management’s Tone Adds to the Pressure

Even though Houlihan still delivered a record fiscal year, management struck a noticeably cautious tone about the near-term environment, citing “uncertainty” as the firm enters its FY27. When leadership signals hesitation on top of recent quarterly underperformance, analysts usually trim their outlook.

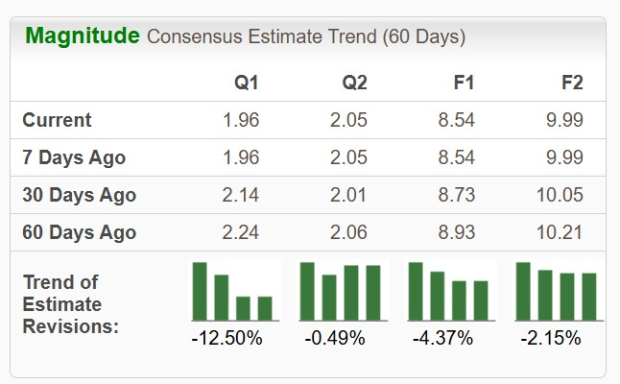

Analysts Respond With EPS Cuts

As shown below, Houlihan’s EPS revisions are starting to decline across the board, highlighted by what is now a 12% drop in Q1 earnings estimates over the last 60 days and a 4% drop in full-year FY27 earnings estimates.

Image Source: Zacks Investment Research

What investors may also want to keep in mind is that while Houlihan stock is trading at a reasonable 17X forward earnings multiple, this is a sharp premium to its Zacks Financial-Miscellaneous Services Industry average of 10X, with other noteworthy peers being American Express AXP), Coinbase COIN), and LendingClub LC).

Image Source: Zacks Investment Research

Bottom Line

Houlihan Lokey remains a high-quality financial investment bank with a strong long-term track record, but the trend of declining EPS revisions suggests short-term weakness is still ahead.

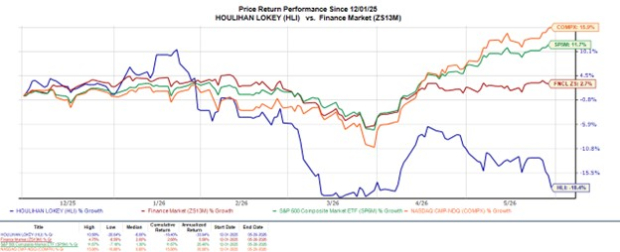

Until analysts see stabilization or a pickup in dealmaking or restructuring activity, Houlihan's stock is likely to remain under pressure after falling nearly 20% in the last six months.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Houlihan Lokey, Inc. (HLI): Free Stock Analysis Report

American Express Company (AXP): Free Stock Analysis Report

LendingClub Corporation (LC): Free Stock Analysis Report

Coinbase Global, Inc. (COIN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).