Liberty Energy Inc. LBRT is a leading provider of completion services and technology solutions for the oil and gas sector. The company earns revenues by offering hydraulic fracturing, wireline and related support services that enable energy producers to optimize well productivity, lower operating costs and improve overall project economics. By leveraging innovative technologies and a modern fleet, Liberty Energy helps customers increase efficiency and enhance returns across their operations.

Over the past six months, LBRT has significantly outperformed both its peers and the broader sector. LBRT’s shares grew 60.8%, significantly higher than 36.6% growth of the Field Services Oil and Gas sub-industry and 21.8% increase in the overall Oil-Energy sector. The company’s impressive performance reflects strong business momentum and a track record of delivering superior returns relative to the sub-industry and the overall energy market.

6-Month Stock Price Performance Overview

Image Source: Zacks Investment Research

LBRT Beats Q1 2026 Earnings and Revenue Estimates

LBRT posted a first-quarter 2026 adjusted net profit of 6 cents per share, in contrast to the Zacks Consensus Estimate of a loss of 13 cents. The outperformance was driven by the company’s focus on technological innovation and strong operational execution. LBRT's revenues totaled $1 billion, which beat the Zacks Consensus Estimate of $949 million.

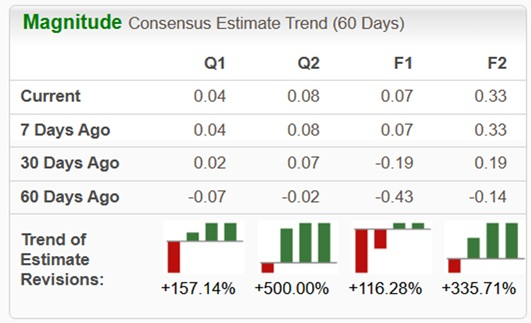

Rising analyst confidence is evident in LBRT’s earnings outlook, as the Zacks Consensus Estimate has increased 116.28% for 2026 and 335.71% for 2027 over the past 60 days.

Image Source: Zacks Investment Research

As a leading player in the industry, LBRT attracts considerable investor attention. The company demonstrates several strengths that have supported growth, yet it also faces risks that warrant careful consideration. Below, let’s dive into the key factors driving LBRT’s stock performance, as well as the challenges that could shape its future trajectory.

What’s Fueling LBRT’s Recent Rally?

Premium Completions Franchise Driving Strong Customer Demand: LBRT continues to attract outsized demand for its premium completion services despite a challenging industry backdrop. Management highlighted that strong fleet utilization, record pumping efficiencies and technology-driven execution supported revenue growth. The company’s ability to maintain customer demand while many competitors face softer activity demonstrates the strength of its service quality and customer relationships.

Industry-Leading Technology Creates Competitive Advantages: LBRT is differentiating itself through proprietary technologies such as StimCommander and Forge. These platforms automate real-time pressure and rate control while continuously learning from fleet-wide operating data. This improves stage consistency, lowers fuel consumption and enhances well economics for customers. Such digital capabilities create barriers to entry and strengthen Liberty Energy’s position compared with traditional pressure-pumping competitors.

Commercial Deployment of Advanced Natural Gas Pump Technology: The company has begun commercial deployment of its latest digiPrime technology, which management described as the industry's only 100% natural gas-powered pump with variable-speed capability. This innovation can reduce operating costs, improve efficiency and lower diesel dependency. As operators increasingly prioritize fuel savings and emissions reductions, Liberty Energy’s advanced fleet design could command stronger customer preference and pricing power.

Positioned to Benefit From Improving Frac Market Fundamentals: Management believes the North American completions market has reached a cyclical floor and is now strengthening. Higher oil prices, increased drilled-but-uncompleted well activity and tightening fleet availability are creating conditions for pricing recovery. Liberty Energy expects utilization improvements and pricing gains to emerge during the year, potentially supporting margin expansion and stronger earnings performance.

What Risks Could Constrain LBRT Stock’s Upside?

Adjusted EBITDA Declined Significantly Year Over Year: Adjusted EBITDA fell to $126 million from $168 million in the comparable prior-year period. This decline occurred despite higher revenues, indicating that pricing pressure and cost inflation continue to affect profitability. If the anticipated pricing recovery fails to materialize, Liberty Energy could face ongoing earnings pressure despite maintaining high utilization levels.

Pressure Pumping Remains a Highly Cyclical Business: Liberty Energy’s core completions business remains heavily tied to upstream oil and gas activity. Customer spending decisions are influenced by commodity prices, drilling economics and broader market sentiment. A decline in oil prices or reduced exploration and production spending could quickly reverse utilization gains and negatively affect revenues, margins and cash flow.

Power Business Requires Significant Upfront Capital: Liberty Energy’s power initiatives represent a major growth opportunity, but they also require substantial capital commitments before generating meaningful returns. Management discussed large equipment purchases, milestone payments and multiyear development cycles. Such investments may pressure near-term cash flow and carry execution risks that are difficult to predict at this stage.

Competitive Oilfield Services Market Can Limit Margins: The pressure-pumping industry remains highly competitive, with operators constantly seeking efficiency gains and cost reductions. Even with Liberty Energy’s technological advantages, customers continue to negotiate aggressively on pricing. Sustained competitive pressure could limit the company’s ability to fully capture the benefits of stronger activity and tighter capacity conditions.

Verdict for LBRT Stock

LBRT benefits from strong customer demand for its premium completions franchise, supported by high fleet utilization, operational efficiency and deep customer relationships. The company’s proprietary technologies, including StimCommander, Forge and the newly deployed digiPrime natural gas-powered pump, provide meaningful competitive advantages through improved efficiency, lower operating costs and enhanced customer economics. Additionally, management believes North American frac market fundamentals are improving, with tightening capacity and higher activity levels potentially supporting pricing recovery and margin expansion.

However, adjusted EBITDA declined significantly year over year, highlighting the ongoing impact of pricing pressure and cost inflation on profitability. The company also faces risks from the highly cyclical nature of the pressure-pumping market, substantial capital requirements for its power business expansion and intense industry competition that could limit margin improvement. Given this mix of strengths and potential challenges, investors should wait for a more opportune entry point instead of adding this Zacks Rank #3 (Hold) stock to their portfolios.

Key Picks

Investors interested in the energy sector might look at some better-ranked stocks like Chevron CVX, Imperial Oil IMO and Marathon Petroleum MPC, sporting a Zacks Rank #1 (Strong Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Chevron is valued at $363.39 billion. It is one of the world's largest integrated energy companies, engaged in oil and natural gas exploration, production, refining and marketing across multiple continents. Chevron is also investing in lower-carbon technologies, including renewable fuels, hydrogen and carbon capture, to support the global energy transition.

Imperial Oil is valued at $57.41 billion. It is a major Canadian petroleum company involved in crude oil production, refining and fuel distribution, with operations concentrated in Canada. A majority-owned subsidiary of ExxonMobil, Imperial Oil benefits from advanced technology and expertise while maintaining a strong presence in Canada's energy sector.

Marathon Petroleum is valued at $72.63 billion. It is one of the largest downstream energy companies in the United States, operating extensive refining, transportation and fuel marketing networks. Through its refining assets and retail fuel brands, Marathon Petroleum supplies gasoline, diesel and other petroleum products to consumers and businesses nationwide.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chevron Corporation (CVX): Free Stock Analysis Report

Imperial Oil Limited (IMO): Free Stock Analysis Report

Marathon Petroleum Corporation (MPC): Free Stock Analysis Report

Liberty Energy Inc. (LBRT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).