Sterling Infrastructure STRL delivered one of the strongest quarters in its history, and its 120% year-over-year adjusted EPS growth is a key reason investors are paying close attention. In the first quarter of 2026, adjusted earnings per share (EPS) surged to $3.59 from $1.63 a year earlier, while revenue jumped 92% to $825.7 million. Adjusted EBITDA also climbed 107%, highlighting broad-based strength across the business.

The significance of Sterling’s EPS growth goes beyond a single quarter. It reflects the company’s ability to convert strong demand into profitable growth. The E-Infrastructure Solutions segment, which serves data centers, semiconductor facilities and other mission-critical projects, remained the primary growth engine. Segment revenue soared 174%, supported by robust data center activity, contributions from the CEC acquisition and expanding margins.

Importantly, Sterling’s earnings growth is supported by a strong pipeline of future work. Signed backlog reached a record $3.8 billion, while combined backlog rose to $5.15 billion. Including future phase opportunities, management now sees visibility into nearly $6.5 billion of potential work. The company recently secured the first phase of a large semiconductor fabrication campus and continues to benefit from accelerating AI-driven data center construction.

Management’s confidence is evident in its raised 2026 outlook. Sterling now expects adjusted EPS in the range of $18.40-$19.05, representing roughly 72% growth over 2025 levels. With expanding margins, record backlog and strong demand across mission-critical infrastructure markets, Sterling’s triple-digit EPS growth underscores the company’s growing earnings power and long-term investment appeal.

How Do Sterling's Growth Trends Compare With Its Peers?

Among infrastructure and engineering companies benefiting from the AI and mission-critical construction boom, EMCOR Group EME and Comfort Systems USA FIX are two notable peers. However, Sterling’s recent earnings momentum has been particularly impressive.

EMCOR continues to benefit from strong demand for electrical and mechanical construction services tied to data centers, manufacturing facilities and healthcare projects. EMCOR has consistently delivered solid earnings growth through strong execution and a growing backlog. Nevertheless, EMCOR's growth profile remains more diversified and mature, making its earnings expansion generally less explosive than Sterling’s recent triple-digit EPS increase. As AI infrastructure spending accelerates, EMCOR remains well-positioned, but Sterling is currently growing at a faster rate.

Comfort Systems has also emerged as a major beneficiary of data center, semiconductor and advanced manufacturing investments. Comfort Systems has posted impressive revenue and profit growth in recent quarters, supported by a robust project pipeline and expanding margins. Like Sterling, Comfort Systems is capitalizing on mission-critical infrastructure demand. However, Comfort Systems' business mix is more focused on mechanical and HVAC systems, whereas Sterling combines site development, electrical services and transportation infrastructure.

Both EMCOR and Comfort Systems remain strong long-term infrastructure plays. Yet Sterling’s 120% adjusted EPS growth, record backlog and expanding exposure to AI-driven projects suggest it is currently among the fastest-growing beneficiaries of the infrastructure investment cycle.

STRL Stock’s Price Performance & Valuation Trend

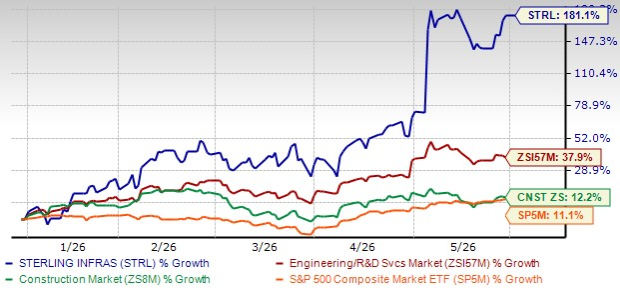

Shares of this Texas-based infrastructure services provider have gained 181.1% year to date, outperforming the Zacks Engineering - R and D Services industry, the broader Zacks Construction sector and the S&P 500 Index.

STRL Price Performance (YTD)

Image Source: Zacks Investment Research

STRL stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 43.68, as shown in the chart below.

STRL Valuation (P/E F12M)

Image Source: Zacks Investment Research

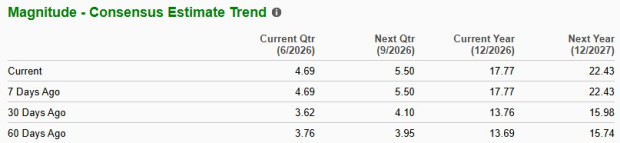

Earnings Estimate Revision of STRL

STRL’s earnings estimates for 2026 and 2027 have moved upward in the past 30 days to $17.77 and $22.43 per share, respectively. The revised estimates for 2026 and 2027 imply year-over-year growth of 63.3% and 26.2%, respectively.

Image Source: Zacks Investment Research

Sterling currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Comfort Systems USA, Inc. (FIX): Free Stock Analysis Report

Sterling Infrastructure, Inc. (STRL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).