DocuSign (DOCU) spent years wearing the "pandemic convenience tool" badge, but it has since grown far past that label and rebuilt itself into a full-blown enterprise software platform. Consistent year-over-year (YOY) growth, improving profitability, and tighter operational discipline gradually restored confidence in the business.

Still, the skeptics have not packed up and left. The bear case rests on two nagging worries. First, artificial intelligence (AI)-native startups are picking up speed and threatening to lap traditional incumbents. Second, the rise of AI agents could gut the economics of e-signature services entirely, undermining the seat-based licensing model that DocuSign has leaned on for years.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

But the bulls have a real argument too. Companies running DocuSign's Intelligent Agreement Management (IAM) platform are generating new documents dramatically faster and cutting agreement finalization time sharply. More than 25,000 paying customers have already adopted the platform, signaling meaningful traction beyond traditional eSignature services.

The tug of war between genuine transformation and market skepticism makes June 4 especially important. DocuSign is scheduled to release its Q1 FY2027 results on Thursday, after market close.

Investors would now be able to see whether management can sustain its revenue growth trajectory, expand adoption of its newer products, and justify the higher expectations that followed several quarters of encouraging execution.

About DocuSign Stock

Based in San Francisco, California, DocuSign delivers AI powered IAM solutions alongside electronic signature technology. Its product portfolio includes eSignature, Contract Lifecycle Management (CLM), Document Generation, identity verification, remote online notarization, and analytics capabilities designed to streamline agreement workflows from start to finish.

Carrying a market cap of approximately $10.2 billion, the company’s reach extends to more than 1.8 million customers and over one billion users spread across more than 180 countries, giving DocuSign one of the largest footprints in the digital agreement ecosystem.

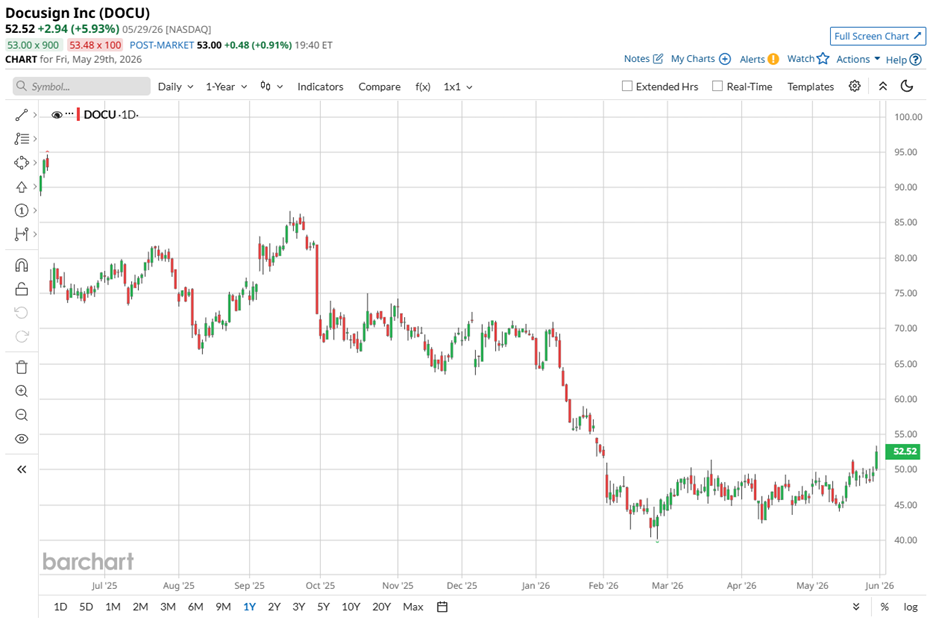

The stock's performance has reflected the market's uncertainty. Over the past 52 weeks, DocuSign’s shares fell 36.58% while, year-to-date (YTD), the stock dropped 17.84%.

However, momentum has started swinging back. Shares have climbed 24.69% during the past three months and gained 17.18% over the last month, suggesting investors have begun warming up to the company's improving fundamentals ahead of earnings.

www.barchart.com

www.barchart.com On the valuation front, DOCU stock is currently trading at 11.83 times forward adjusted earnings and 2.92 times sales. Both figures sit below industry averages as well as their own five-year historical valuation levels. The discount suggests that the market is pricing in meaningful uncertainty, creating an opportunity for investors who believe management can continue executing successfully.

DocuSign Surpasses Q4 Earnings

Investor enthusiasm received a boost on March 17 when DocuSign reported its Q4 FY2026 results. The market responded positively. Shares gained 1.54% on the day of the announcement and added another 2.86% during the following trading session.

Revenue increased 7.8% YOY to $836.9 million, comfortably ahead of analyst expectations of $828.2 million. Subscription revenue reached $819 million, reflecting an 8.1% annual increase. Professional services and other revenue totaled $17.9 million, representing a 3.4% decline from the prior year.

Coming to profitability, non-GAAP net income climbed 11.5% to $206.1 million from the year earlier period, while non-GAAP EPS grew 17.4% from the year-ago value to $1.01, surpassing Wall Street's expectation of $0.95.

Perhaps most notably, billings crossed the $1 billion mark for the first time in company history, growing 10% YOY. The company's newer growth initiatives also continued gaining ground. Just over 18 months after launch, IAM generated more than $350 million in annual recurring revenue. The contribution represented 10.8% of total company annual recurring revenue compared with only 2.3% at the end of fiscal 2025.

Such rapid expansion demonstrates that customers are increasingly embracing DocuSign's broader platform vision. Customer metrics reinforced the trend as total customers increased 9% YOY to more than 1.8 million. The company finished the quarter with 1,205 customers spending more than $300,000 annually, reflecting a 7% increase from the prior year.

Looking ahead, management expects Q1 FY2027 revenue between $822 million and $826 million, representing approximately 8% YOY growth at the midpoint. For FY2027, the company projects revenue between $3.484 billion and $3.496 billion, which also implies roughly 8% growth at the midpoint.

On the other hand, analysts currently expect Q1 FY2027 EPS to decline 5% YOY to $0.38, which represents a 5% decline from the previous year’s quarter. Longer term projections paint a brighter picture. Wall Street expects full FY2027 EPS to rise 6.1% from the previous year to $1.75 while they forecast a jump of 23.4% to $2.16 in FY2028.

What Do Analysts Expect for DocuSign Stock?

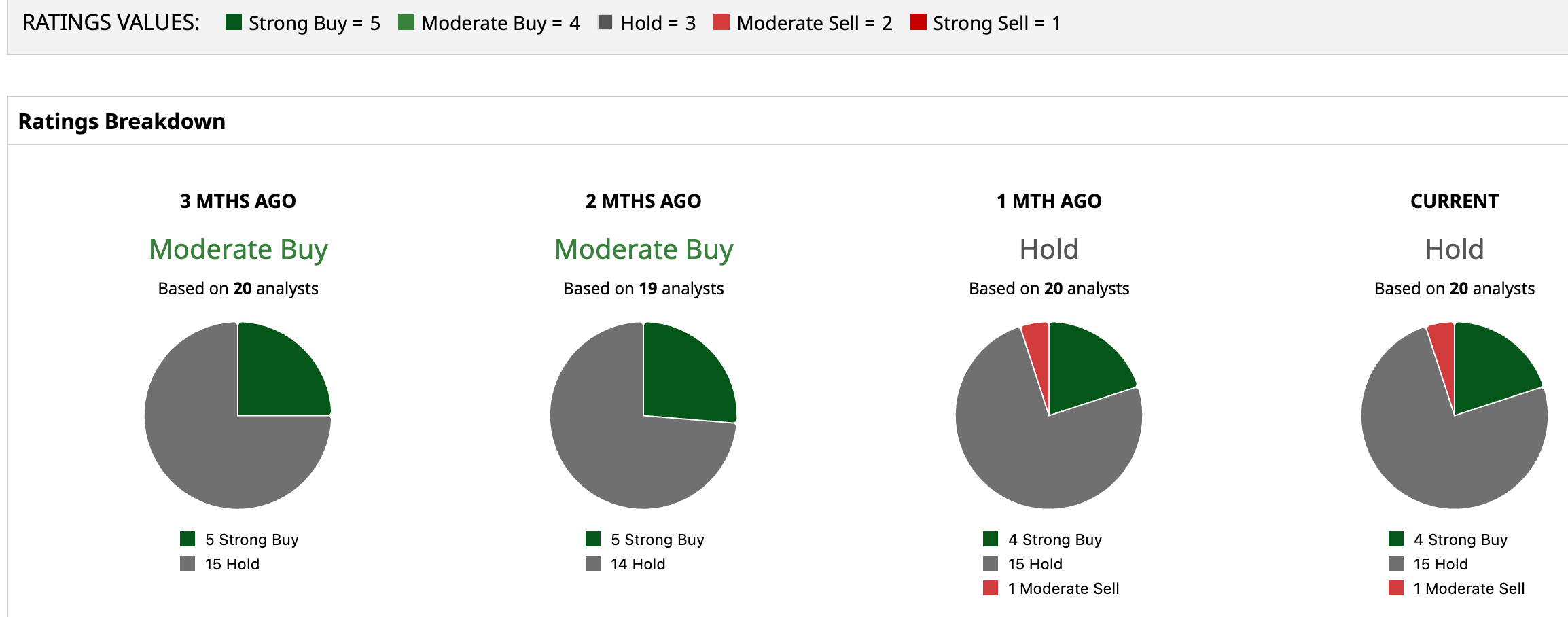

Wall Street has yet to pick a side on DOCU stock. They have currently assigned it an overall rating of “Hold.” Among 20 analysts tracking the stock, four recommend a “Strong Buy,” 15 suggest to “Hold,” while one remains cautious with a “Moderate Sell” rating.

The mixed outlook reflects the ongoing tug of war between confidence in DocuSign's platform driven evolution and concerns about future competitive pressures. Despite the cautious consensus, analysts still see room for upside.

Interestingly, the stock’s average price target of $58.81 represents potential upside of 3.87%. Meanwhile, the Street-High target of $86 suggest a gain of 52.16% from current levels, suggesting some analysts believe the market may be underestimating DocuSign's long term growth potential.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Docusign Stock Fans, Mark Your Calendars for June 4 Dear Honeywell Stock Fans, Mark Your Calendars for June 3 NXT Stock Alert: Solar Company Nextpower Is Taking on Data Centers With New Acquisition Costco Just Reported 'Record-Breaking' Gas Sales. COST Stock Is Falling Anyway.