Taylor Morrison Home (TMHC) shares soared on June 1 after Berkshire Hathaway’s (BRK.A) (BRK.B) new leader, Greg Abel, announced a definitive agreement to acquire the homebuilder for about $6.8 billion.

This landmark transaction that values TMHC at $72.50 per share marks Abel’s first major takeover since taking the helm from the legendary Warren Buffett at the start of this year.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Including yesterday's surge, Taylor Morrison stock is up nearly 30% versus its year-to-date low.

www.barchart.com

www.barchart.comIs Berkshire Deal Positive for Taylor Morrison?

The take-private agreement with Berkshire Hathaway is structurally and financially constructive for Taylor Morrison.

Operating away from the intense scrutiny of quarterly earnings reports will enable the homebuilder to pivot toward long-term land acquisition strategies and multi-year construction cycles.

Plus, given Berkshire’s fortress balance sheet ($397 billion in cash and short-term investments at the end of Q1), Taylor Morrison has effectively secured a very low cost of capital.

That firepower could accelerate TMHC’s expansion into new geographies and product lines.

As CEO Sheryl Palmer put it in a statement: “Joining Berkshire Hathaway Inc is a once-in-a-lifetime opportunity to propel Taylor Morrison into its next, and most exciting chapter.”

All in all, the deal positions TMHC to scale its move-up and resort housing segments even during the cyclical real estate downturns without worrying about short-term share price volatility.

Is It Too Late to Invest in TMHC Shares Already?

For investors eyeing TMHC shares today, the math is sobering.

With the stock trading at roughly $71.60 — just under $1 shy of Berkshire’s buyout price — the deal premium is almost entirely priced in, leaving a residual spread of less than 1.3%.

This slim gap reflects the market’s confidence that the transaction will close without incident, subject to shareholder approval and standard regulatory clearances.

The remaining upside from holding Taylor Morrison stock at the current price is essentially equivalent to a short-duration, low-yield bond proxy tied to deal completion risk.

The primary scenario that would meaningfully lift TMHC above $72.50 is a competing bid from a rival suitor — possible in theory, but considered unlikely given the deal’s structure and Berkshire’s standing.

Absent that, new buyers at today’s price are taking on closure risk for minimal reward.

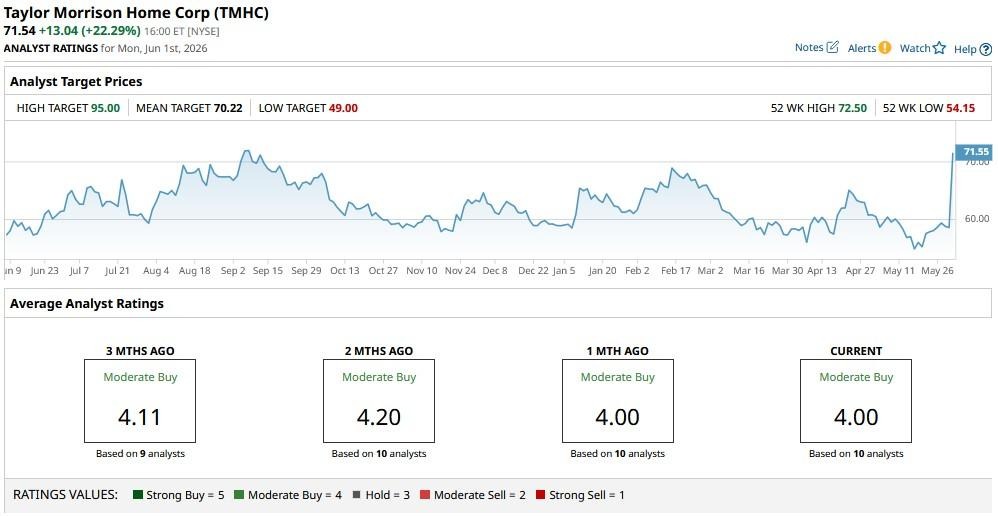

Taylor Morrison Is Trading Above Street’s Mean Target

Heading into June 1, Wall Street had a consensus “Moderate Buy” rating on Taylor Morrison shares, with a mean price target of $70.22.

This means experts didn’t expect TMHC to trade at a price higher than what it’s going for currently anyway.

www.barchart.com

www.barchart.com On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Even If Eli Lilly Stock Continues to Shine, Stay Away from This Pharmaceutical ETF Micron Stock Could Still Have Nearly 70% Upside Potential Left in Its Tank Nvidia Launches AI Chip for Laptops. Count NVDA Stock Out at Your Own Peril. Greg Abel's Big Bet: Berkshire to Buy Taylor Morrison Homes in $6.8 Billion Deal