Artificial intelligence is emerging as one of the most important growth opportunities for Vishay Intertechnology VSH, with management highlighting strong and accelerating demand across multiple AI-related applications.

During the first quarter of 2026, the company reported continued momentum in AI-driven programs, particularly across power infrastructure, data centers and optical communications. Management also indicated that AI-related revenues in 2026 are expected to be significantly higher than in 2025.

Vishay is benefiting from the growing adoption of several key technologies used in AI systems. Management cited sustained demand for high-voltage MOSFETs used in AI power applications, while customers continue to add Vishay’s polymer capacitors, power inductors and current-sense resistors to AI power management architectures. These products are increasingly being incorporated into next-generation server power supplies, AI infrastructure equipment and high-performance networking systems.

VSH’s AI exposure is also broadening beyond servers. Vishay is actively pursuing opportunities in optical communication modules, 800-gigabit and 1.6-terabit networking switches, and next-generation power systems required to support rapidly growing AI workloads. The company noted increased collaboration with telecom customers involved in AI optical networking while continuing to advance design efforts for next-generation AI power supplies and 800-volt power-management systems targeting data-center applications.

Vishay believes its expanded manufacturing capacity under the Vishay 3.0 strategy is strengthening its competitive position. While larger semiconductor suppliers remain formidable competitors, Vishay is leveraging shorter lead times, expanded capacity and a unique combination of semiconductor and passive component offerings to gain share.

Management pointed to supply constraints affecting some competitors and said Vishay is capturing incremental AI-related business by offering reliable supply and products available for immediate delivery.

As AI infrastructure spending continues to expand, Vishay appears increasingly well positioned to convert this demand into a meaningful long-term growth driver.

Peer Updates

Diodes DIOD delivered another strong quarter, with revenues rising 22% year over year to $405.5 million, supported by accelerating momentum in automotive, industrial and AI server-related applications. Automotive and industrial together accounted for 44% of product revenues, helping gross margin expand to 31.8% as higher-margin content and utilization improved.

Growth was fueled by increasing semiconductor content in vehicles, AI-driven power infrastructure, industrial automation and data-center networking. Management also highlighted robust design wins in silicon carbide, power management and connectivity products.

Sustainability appears favorable as AI infrastructure, automotive electrification and factory automation remain secular drivers, though management expects customer qualification cycles and fab loading normalization to extend into 2027–2028, suggesting growth should remain durable but gradual rather than explosive.

Lattice Semiconductor LSCC posted a robust quarter, with revenues surging 42% year over year to $170.9 million, driven primarily by AI data center demand, compute and communications strength and industrial automation recovery. Compute and communications reached record levels, accounting for 62% of revenues, while industrial and embedded products rebounded more than 20% sequentially.

Growth is increasingly being driven by Lattice’s expanding presence in AI servers, where its low-power FPGAs support security, power sequencing and platform management functions rather than competing directly with CPUs and GPUs.

The growth outlook appears sustainable, with bookings extending into 2027, channel inventory normalizing to roughly two months and management describing the company as being in the “early innings” of a multiyear cycle driven by AI infrastructure, networking and physical AI applications. However, supply-chain constraints and rising backend costs could temper future margin expansion.

VSH’s Price Performance, Valuation and Estimates

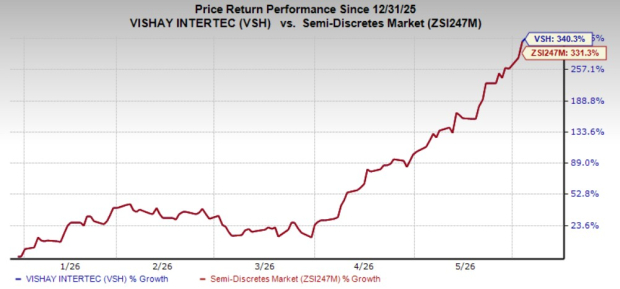

Shares of Vishay have skyrocketed 340.3% so far this year compared with the industry’s 331.3% growth.

Image Source: Zacks Investment Research

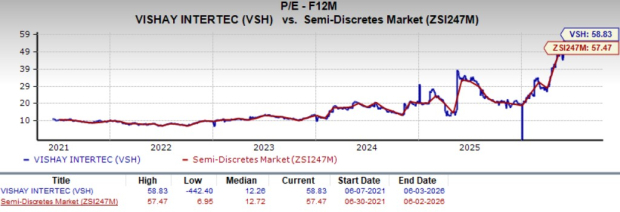

From a valuation standpoint, Vishay trades at a forward price-to-earnings ratio of 58.83, significantly above the industry average. It is also higher than its five-year median of 12.26. VSH carries a Value Score of D.

Image Source: Zacks Investment Research

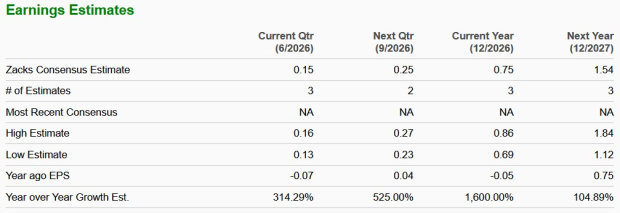

The Zacks Consensus Estimate for Vishay’s fiscal 2026 earnings implies a 1600% improvement from the year-ago period’s level.

Image Source: Zacks Investment Research

The stock currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Lattice Semiconductor Corporation (LSCC): Free Stock Analysis Report

Diodes Incorporated (DIOD): Free Stock Analysis Report

Vishay Intertechnology, Inc. (VSH): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).