In the old tactical playbook for a top-heavy, late-cycle market regime, one of the rules is “when growth gets risky, hide out in the consumer staples sector.” Well, the 20th century stock market called. And it wants its playbook back.

The theory is that no matter how ugly the macro environment gets, people still need to eat, drink, and buy household essentials. To execute this defensive strategy, investors often flock to the Invesco Food & Beverage ETF (PBJ).

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

With its clever ticker and a basket packed with structural food giants, agricultural processors, and grocery distributors, PBJ is marketed as the ultimate recession-proof buy. However, 2026 is proving to be different.

The PBJ ETF isn’t protecting capital. It is actively destroying it.

The underlying tape tells us a story, as it always does. Inflation is not going away. In fact, it has proven to be as incredibly sticky as a giant glob of peanut butter plastered to the roof of your mouth. And while you might think inflation would help companies that sell food, the unique construction and economic reality of PBJ makes it less of a consumer staple, and more like a staple in your finger.

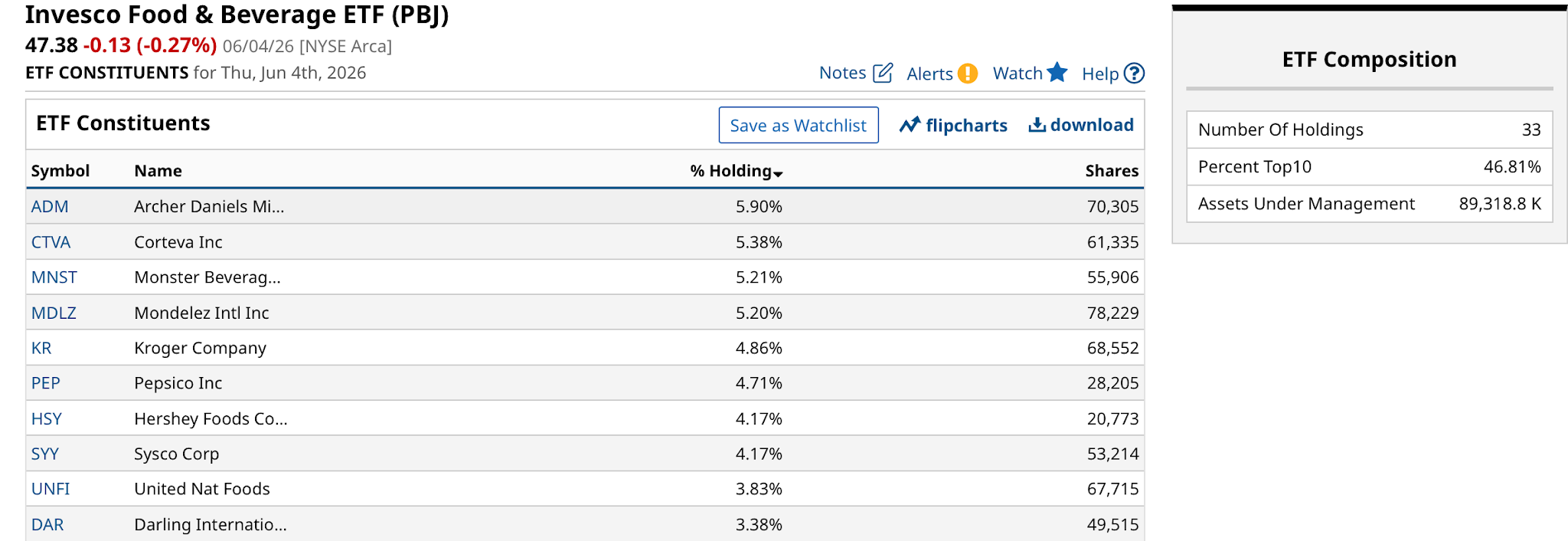

Here’s PBJ’s current lineup, or at least the top 10 holdings. That’s about half the ETF’s assets, with the rest allocated to roughly 20 more names.

www.barchart.com

www.barchart.com The core fundamental flaw with the “buy food stocks for inflation” thesis is that it completely misinterprets how pricing power works when inflation becomes more ingrained in the financial system.

In the initial stages of a pricing spike, large food conglomerates can easily pass higher costs onto the end consumer, temporarily boosting their nominal revenues. But we are now deep into a multi-year inflationary cycle. The structural inputs that drive PBJ’s components, including diesel fuel for shipping, agricultural fertilizers, industrial electricity, and labor, remain stubbornly pinned to the ceiling.

The companies inside PBJ have officially hit the upper limit of consumer elasticity. The regular, working-class consumer is completely tapped out. After years of paying grocery bills that feel like a second mortgage, consumers are aggressively trading down. That means instead of buying the premium, high-margin branded products manufactured by PBJ’s top holdings, they are migrating to private-label generic store brands.

As a result, volume growth across the food and beverage industry has flatlined or turned negative. This means forward profit margins are compressing at an accelerating rate — the exact opposite of what you want from a “defensive” investment.

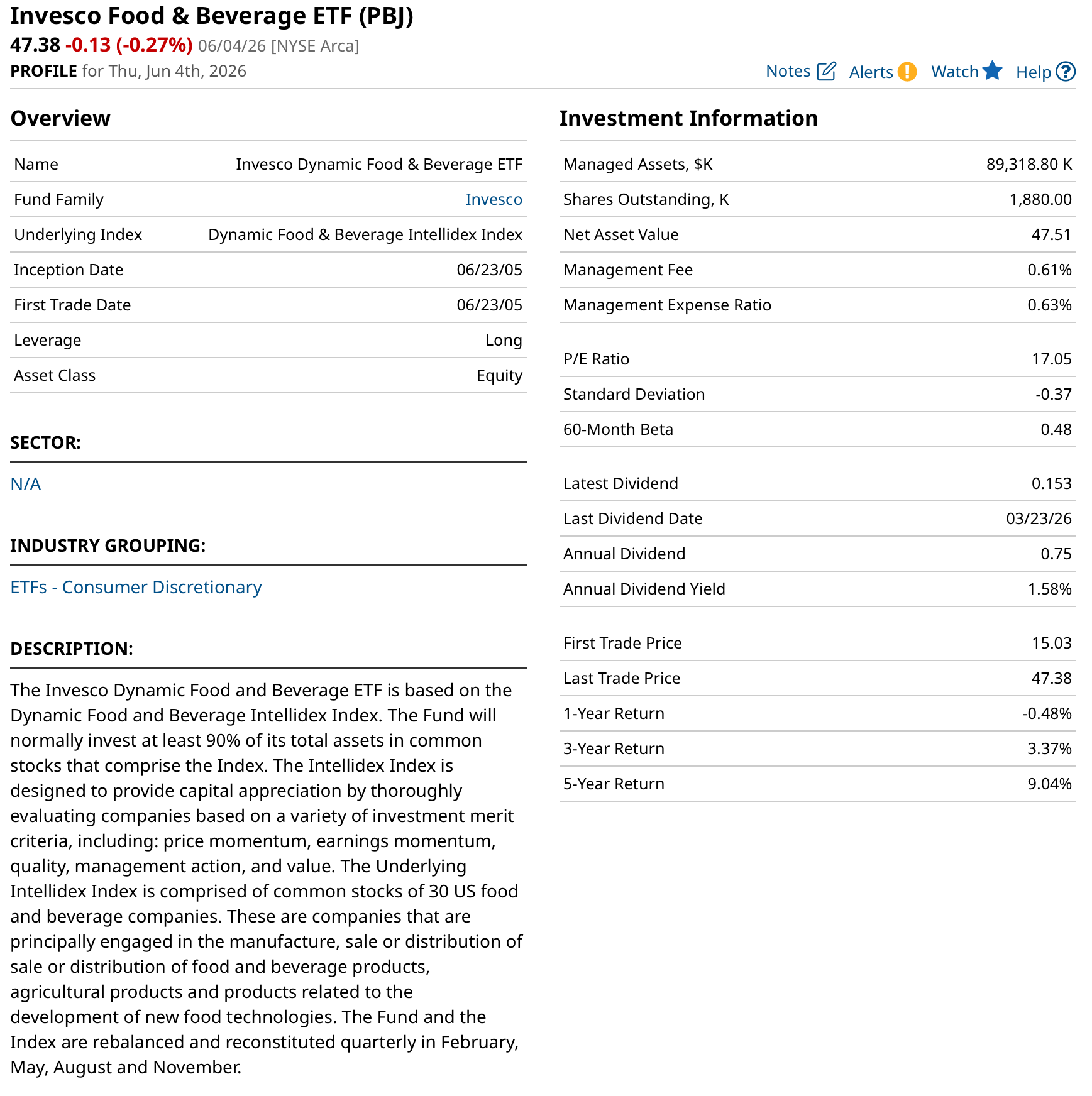

Even if you wanted to express a defensive view on the consumer, PBJ’s index construction is less fit for this predicament as opposed to the more broader Consumer Staples SPDR ETF (XLP), one of the 11 S&P Sector SPDRs.

Unlike standard cap-weighted sector funds, PBJ tracks a dynamic, multi-factor index that selects companies based on price momentum, earnings trend, and management capability. While that sounds sophisticated, it routinely results in a bizarrely constructed, concentrated portfolio that exposes you to the worst elements of the agricultural and food supply chain.

Instead of owning pure, steady, cash-flow-heavy global mega-caps with unassailable distribution moats, PBJ frequently overweights highly cyclical agricultural processors and low-margin grocery middle-men. These are asset-heavy, low-margin businesses that possess zero pricing power and are entirely at the mercy of global commodity swings. When commodity inflation remains sticky, these distributors get crushed first because they cannot instantly rewrite their multimillion-dollar institutional supply contracts.

www.barchart.com

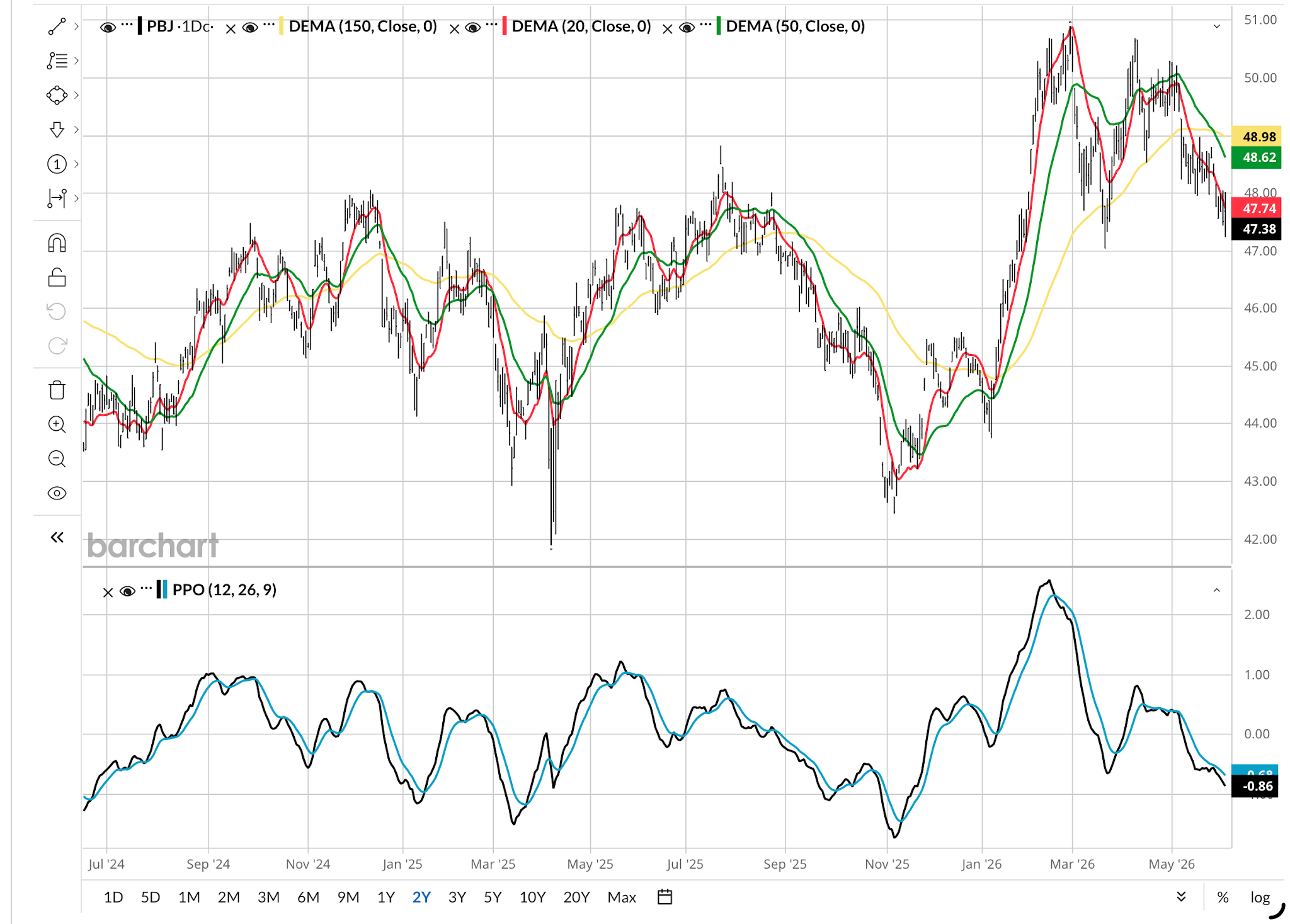

www.barchart.com How do I know I’m not the first to point this out?

See the daily price chart above. PBJ is only off about 8% from its recent high. But that drooping percentage price oscillator (PPO) at the bottom of the chart.

www.barchart.com

www.barchart.com The PBJ ETF is a broken defensive approach for a structural inflation era. The “peanut butter” inflation is sticking to the roof of the consumer’s mouth.

Trying to hide in low-growth, margin-compressed food packaging and distribution stocks is a legacy strategy that no longer works when input costs refuse to fade back down.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As IBM Unlocks a ‘Multi-Billion-Dollar Opportunity’ With Google, The Stock Is a Buy ServiceTitan Stock Surged on Better-Than-Expected Results Powered by AI. What This Means for ServiceTitan Investors. As Cash Flows Swell, The Market Will Start Loving AppLovin Stock Consumer Staples Stocks Are No Longer a Recession-Proof Haven Amid High Inflation. Just Look at the PBJ ETF.