Artificial intelligence (AI) data centers are packed with power-hungry GPUs that need massive amounts of electricity, cooling, and infrastructure to keep those advanced chips running. Investors now know how that this demand is creating opportunities for a new class of AI infrastructure winners. One company increasingly catching Wall Street's attention is nVent Electric (NVT), which has often been referred to as “mini” version of Vertiv (VRT).

NVT stock has climbed 68% year-to-date (YTD), compared to VRT stock's gain of 96% so far this year. Let’s take a closer look at why Wall Street rates this “Mini Vertiv” stock as a “Strong Buy” now.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Why nVent Electric Is Suddenly Being Called a “Mini Vertiv”

nVent Electric is not a pure-play AI company. But it has often drawn comparisons to one of the leading AI infrastructure providers: Vertiv. Vertiv provides liquid cooling systems, power distribution units, and thermal management solutions, among other critical products that allow data centers to run effectively.

On the other hand, nVent is a broader electrical infrastructure company that sells enclosures, connectors, grounding systems, cable management products, and increasingly liquid-cooling solutions used in data centers, industrial facilities, utilities, and commercial buildings. AI data centers are driving exceptional growth not only for Vertiv but also nVent, which provides a similar ecosystem. This is probably why Wall Street now gives nVent stock a consensus “Strong Buy” rating.

In the first quarter of fiscal 2026, nVent's revenue increased 53% year-over-year (YOY) to $1.24 billion, driven by a 34% rise in organic sales. Adjusted EPS increased 63% to $1.09, marking the first time the company achieved more than $1 in quarterly adjusted EPS. Management cited AI data centers as the primary growth engine.

CEO Beth Wozniak specified that nVent's data-center business expanded across both "gray space" and "white space" applications. The company is winning business from hyperscalers, neocloud providers, multi-tenant operators, and distribution partners. Notably, organic orders grew 40%, while backlog currently stands at $2.6 billion, fueled by orders for the AI data-center buildout. For investors, these numbers are important, as they reveal that customers are placing orders quicker than the company is currently recognizing revenue.

Importantly, infrastructure — which now accounts for 55% of total company sales — reported nearly 80% organic sales growth in Q1, fueled primarily by data-center demand. Power utility sales surged by double digits, while industrial sales and commercial/residential sales increased by mid-single digits.

nVent’s willingness to invest aggressively in growth opportunities has also made Wall Street more optimistic. The company launched 11 new products during the quarter. Management expects $130 million in capital expenditures in 2026, with much of the investment directed toward supporting development in data centers and power utilities.

For 2026, nVent now expects organic growth of 21% to 23%, with total revenue increasing by 26% to 28%. Likewise, adjusted EPS is expected to increase by 34% YOY at the midpoint.

Why Buy nVent Electric Instead of Vertiv?

Investors might wonder why anyone would want to buy the “Mini Vertiv” instead of Vertiv itself. At a market capitalization of $115 billion, Vertiv is a much larger company than nVent at $27 billion. In fact, Vertiv works directly with Nvidia (NVDA) on next-generation AI factory designs and large-scale power architectures. Vertiv is a clear AI winner, with 30% and 83% YOY growth in revenue and earnings in its most recent first quarter.

The answer lies in valuation. With Vertiv's increasing prominence in AI infrastructure, VRT stock now trades at a premium. So what if investors want exposure to AI infrastructure but do not want to pay Vertiv’s lofty premium? In that case, nVent is the clear choice. At 37 times forward earnings, nVent is cheaper compared to Vertiv's forward price-to-earnings (P/E) ratio of 49 times.

Analysts expect nVent’s earnings to increase by 36% in fiscal 2026, followed by a 22% YOY increase in fiscal 2027. Revenue is also predicted to grow by double digits over the following two years.

Wall Street Is Strongly Bullish About nVent

No doubt, Vertiv remains one of the most recognized AI infrastructure stocks on Wall Street. But if the AI infrastructure buildout continues at its current pace, this "Mini Vertiv" may not remain under-the-radar for much longer.

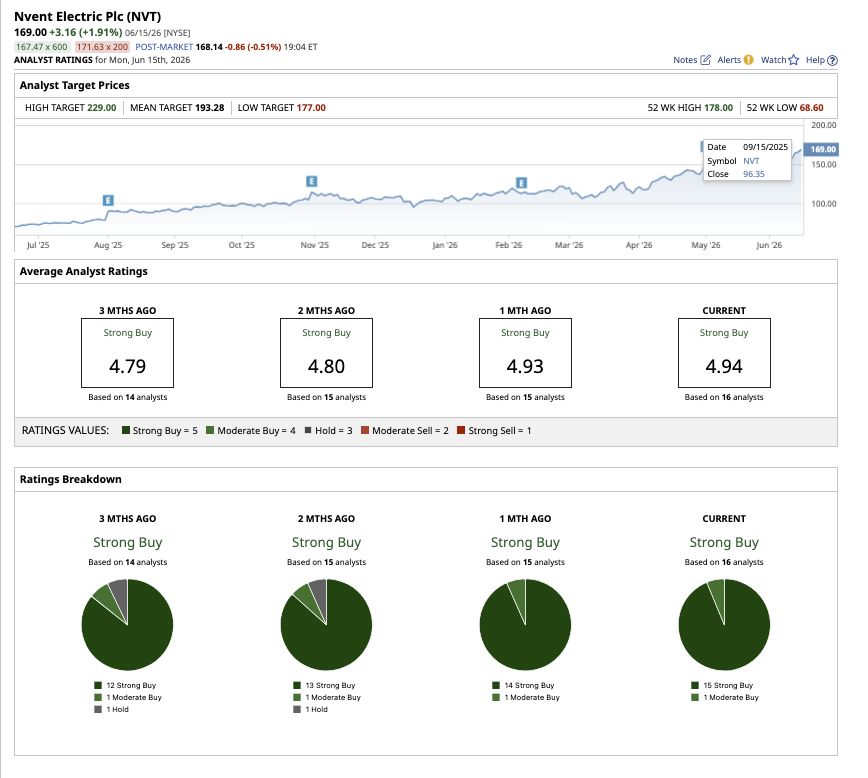

Wall Street already recognizes nVent’s growing importance and has given the stock a consensus “Strong Buy” rating. Of the 16 analysts covering the stock, 15 rate it as a "Strong Buy" while one analyst has a “Moderate Buy” rating. The average price target of $193.28 implies potential upside of 13% from current levels. Furthermore, the Street-high price estimate of $229 suggests 34% potential upside over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Shorting Out-of-the-Money Cisco Puts and Calls Provides Shareholders Extra Income Why the Roku Buyout Is a Cautionary Tale for AI Stocks Apple Is Betting That Its Next Big Product Could Be AirPods with Cameras The ‘Mini Vertiv’ AI Stock Wall Street Is Strongly Bullish About